The Power 100: Commercial Real Estate’s Most Powerful Players

By The Editors April 23, 2019 9:00 am

reprints

As Marc Holliday began explaining all SL Green Realty Corp. had done in the last year, he paused.

“I don’t know where to begin.”

SL Green had a banner year. It announced plans for One Madison Avenue, it took over the leasehold for 2 Herald Square,it churned out leases at One Vanderbilt and it even dipped into affordable housing.

It would be criminal if the firm landed anything short of No. 1.

But how would we live with ourselves if we didn’t give Related Companies the No. 1 spot on the year when Hudson Yards had its big debut? The naysayers were drowned out by the crowds who liked the enormous copper beehive (or whatever the kids call it). They love the shopping, the dining—even the Shed, notwithstanding the snide comparisons to airplane hangars.

Related wasn’t our No. 1 choice, either.

Last year, Brookfield Property Partners—which has been gobbling up properties and companies like it has a tapeworm—seized the title as New York City’s biggest commercial landlord. Brookfield will soon beat out Blackstone in assets under management globally, thanks to buying Oaktree Capital Management. We didn’t even mention the millions of square feet it unveiled at Manhattan West. We felt that was worth a lot.

Last year was, in essence, an embarrassment of riches for the real estate industry. These are the top players.—Max Gross

The 2019 Power 100 Issue:

Welcome to the List

The Bezos Factor: Who Fell a Few Rungs Thanks to Amazon

Biggest Jumps

Power Landlords: The Guys Who’ve Got the Biggest Portfolios in New York

Power Designers: The Most Powerful Eyes in the Business

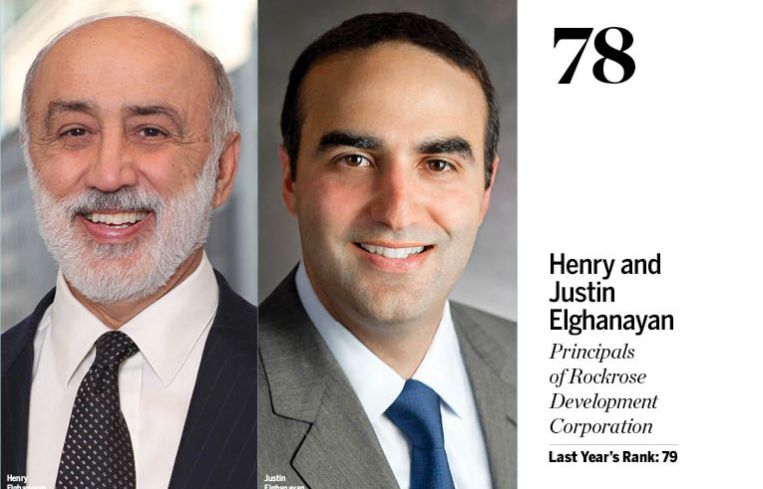

1. Ric Clark and Brian Kingston

Chairman of Brookfield Property Group and Brookfield Property Partners; CEO of Brookfield Property Group

Last Year's Rank: 1

The Far West Side is largely considered Related Companies territory. But it really shouldn’t be.

Brookfield Property Partners has Manhattan West, which, when complete, will span 7 million square feet across six buildings, including 5.5 million square feet of offices, a Pendry Hotel, residential units and retail.

In the past year, the company has completed leasing its 1.5-million-square-foot 5 Manhattan West as well as its 200,000-square-foot Lofts at Manhattan West. And at 1 Manhattan West, which is slated to open in the fall, there are only seven or eight floors left for lease in the 2-million-square-foot, 67-story office building. The company has notched high-profile tenants at Manhattan West including Skadden Arps, accounting firm EY, the National Hockey League, Amazon, J.P. Morgan Chase, a Peloton flagship, a Whole Foods market and a Danny Meyer restaurant.

But its leasing, as impressive as it is, is not the whole story.

“We are now New York City’s biggest commercial landlord,” Ric Clark said.

It’s a status Brookfield already enjoyed in Los Angeles, Houston, London, Toronto, Calgary and Perth, according to Clark.

One of the “big things that moved the needle” for the company, he said, was acquiring Forest City, a July 2018 $11.4 billion deal (including debt) which gave Brookfield an additional 11 million square feet of office space (and 18,500 apartments) in the U.S., 5 million of which (and 2,500 apartments) is in New York City. Brookfield’s worldwide portfolio spans 450 million square feet. Clark credited Brian Kingston with sealing the Forest City deal.

And don’t forget, early last year Brookfield acquired GGP in a $9.3 billion cash deal, also due to Kingston’s handiwork. (That included 125 malls, or as a Brookfield Properties spokesman indicated, “8 percent of the high-quality retail space in the country.” In Gotham alone, that deal gave Brookfield more than 2 million square feet of retail.)

Brookfield will soon beat out Blackstone in assets under management globally. When Brookfield’s purchase of a 62 percent majority stake in Los Angeles-based global asset management firm Oaktree Capital Management for $4.8 billion closes, it will bring Brookfield to $475 billion in assets under management. (Blackstone has $472 billion, as per its fourth-quarter 2018 filing.)

Brookfield’s U.S. multifamily business, which did not exist eight years ago, grew to $17 billion last year, covering 67,000 units within 225 properties. And its total real estate assets under management climbed to $188 billion worldwide in 2018, up $40 billion over the last two years. And parent company, Brookfield Asset Management, one of the world’s largest alternative investment managers, has kicked off 2019 with a bang, closing its largest global real estate fund, Brookfield Strategic Real Estate Partners III, at $15 billion.

And last August, Brookfield assumed operations of the troubled 666 Fifth Avenue via a 99-year ground lease with Kushner Companies. Part of the 2019 mission is to “launch the redevelopment plan for 666 Fifth and re-tenant it,” said Clark, who led the deal. Plus, Brookfield will pursue tenants at its 2-million-square-foot 2 Manhattan West, a spec office building on which the firm launched construction.

All this adds up to a choice spot on the Power 100. The most choice. Number one.—L.E.S.

2. Stephen Ross, Jeff Blau and Bruce Beal

Chairman and Founder; CEO; President at Related Companies

Last Year's Rank: 3

After more than a decade of construction, Related Companies unveiled its masterpiece in March: the $25 billion, 18-million-square-foot Hudson Yards.

“We spent the last 11 years designing, planning and executing, with all of the construction issues,” said Jeff Blau. “When you’re done you kind of think you got everything right, but you hope people will come.”

Those worries were unwarranted. With more than 100 shops and restaurants, a cultural center and an Equinox-branded hotel, the project has broken every goal the developer set for it already—visitor numbers, condominium sales, office rents and money spent in the shops—despite hearing for years that “New Yorkers hate malls,” Blau said.

“It doesn’t seem that way to me,” he said. “We don’t call it a mall; it’s urban vertical retail shopping. And it seems to be working.”

Opening Hudson Yards would be enough for most companies to earn a high spot on this list, but Related didn’t stop there. The developer inked one of the biggest leases of 2018 in December when Deutsche Bank signed on for 1.1 million square feet at the Time Warner Center (which will be renamed in honor of the bank).

Outside of New York City, Related secured the land entitlements to start work on a 62-acre mixed-use development in Chicago and a 240-acre project in California and started to expand its Equinox-branded hotels to other states.

Related announced plans in October 2018 to build $3 billion of luxury senior housing in San Francisco and New York and got into the fulfillment business when it bought Quiet Logistics this March for an undisclosed sum.

Blau said the idea for the Quiet Logistics acquisition came after hearing from digitally native brands in which Related was invested how difficult it was to find nearby warehouse spaces for last-mile delivery.

And Related shows no signs of slowing down this year. It will get to work on its mega-projects in Chicago and California while turning its attention to the 6.2-million-square-foot second phase of Hudson Yards which includes another 2 million square feet of office, 4 million square feet of residential, 100,000 square feet of retail and a 120,000-square-foot elementary school.

“We planted a lot of seeds this year and we’ll go back into execution mode next year,” Blau said.—N.R.

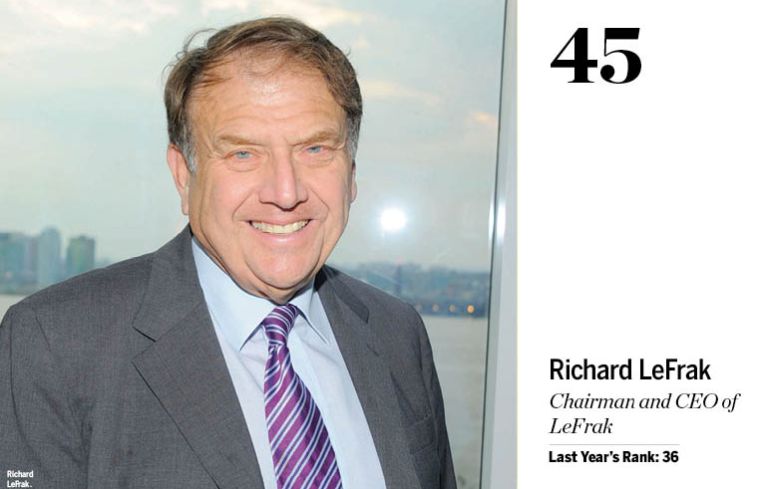

3. Marc Holliday and Andrew Mathias

CEO; President of SL Green Realty Corp.

Last Year's Rank: 2

SL Green Realty Corp. has a reputation that’s centered around its status as one of Manhattan’s largest and most prominent office landlords.

But in 2018, the developer first dipped its toe in a ground-up, partially-affordable residential project at 185 Broadway in the Financial District. The 31-story, 260,000-square-foot building will hold 209 units, 30 percent of which will rent at below-market rates. Contractors are currently digging the foundations for the building between Dey and Cortlandt Streets.

Of course, One Vanderbilt gets the most press, and in Midtown the steel superstructure for the 1.7-million-square-foot building has risen 1,100 feet in the air. The development is 54 percent leased and expected to be complete in August 2020, eight weeks ahead of schedule. TD Bank and TD Securities will move in as the first tenants this August. And SL Green’s work improving the subway platforms at Grand Central Terminal is 80 percent complete.

The real estate investment trust is also working on a 20-unit residential condominium project on top of a Giorgio Armani store at 760 Madison Avenue at the corner of East 65th Street, where it expects to break ground by the end of the year.

The major commercial landlord currently has six developments with more than 5 million square feet of construction in the pipeline, including a massive planned expansion at One Madison Avenue. The former Metropolitan Life Insurance Building—which is attached to the iconic clock tower overlooking Madison Square Park—will get an 18-story glass expansion designed by Kohn Pedersen Fox, bringing its footprint to 1.5 million rentable square feet.

“We’ll be completely transforming the podium with new window systems and replacing the limestone with a glass curtain wall system,” said Marc Holliday. “We have an excellent design that pays homage to the historical and architectural history of this site.”

The firm also plans to revamp a 600,000-square-foot former printing plant at 460 West 34th Street on 10th Avenue by Hudson Yards into high-end office space. It just nailed down a 212,000-square-foot lease with First Republic Bank at the property, which it entered contract to buy in December 2018.—R.B.R.

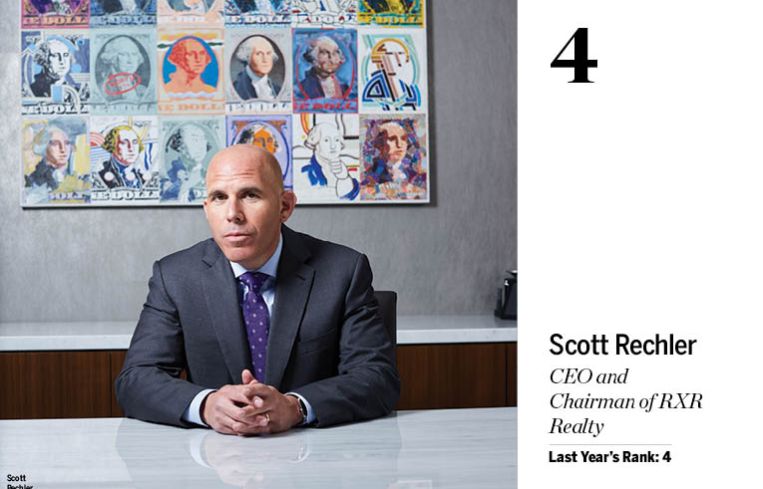

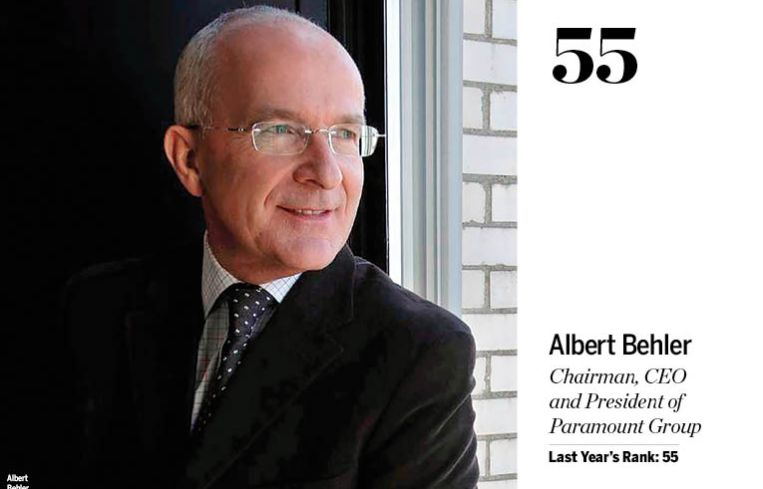

4. Scott Rechler

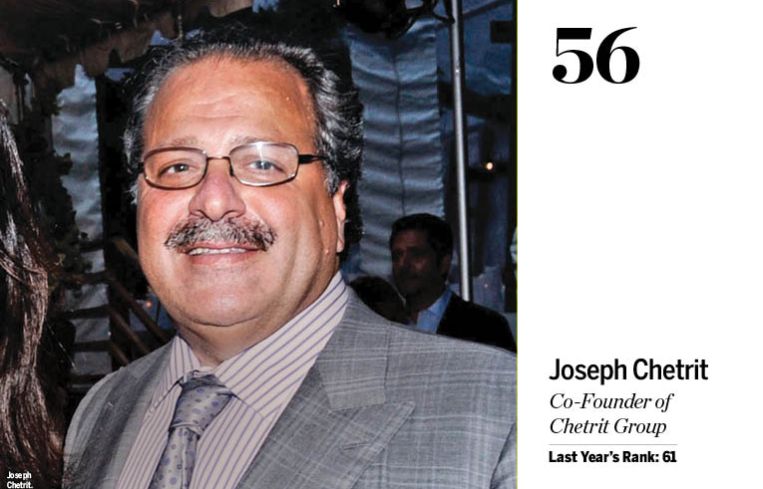

CEO and Chairman of RXR Realty

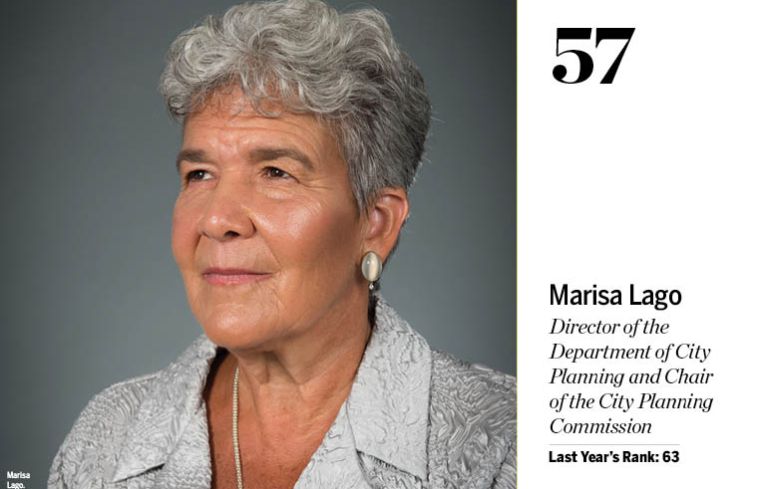

Last Year's Rank: 4

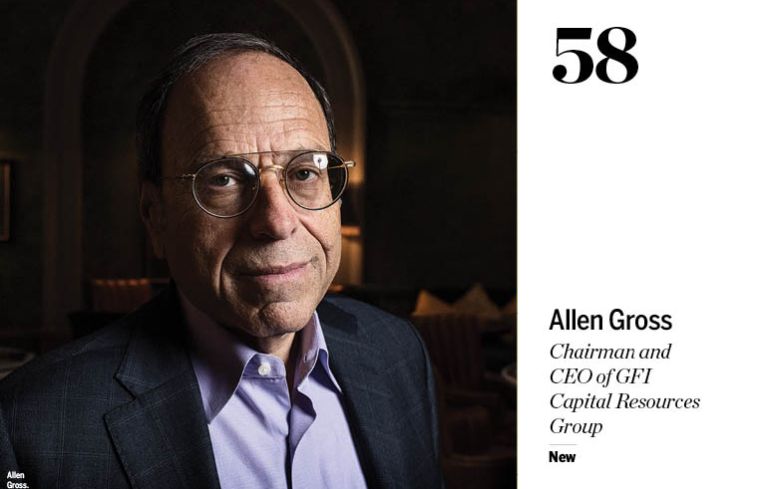

You could say that RXR Realty has been a wee bit busy over the past 12 months.

“We’re expanding our scope. It’s all about understanding New York and the customers of New York,” Scott Rechler said. “And, it’s fun—more time-consuming than just buying an office building—but fun.”

RXR’s lengthy list of projects includes joining TF Cornerstone and MSD Capital’s development team in building a $3 billion office and hotel tower next to Grand Central Terminal at 109 East 42nd Street; being selected to lead JetBlue’s $3 billion planned terminal expansion at John F. Kennedy International Airport; building a 1-million-square-foot last-mile distribution facility in Maspeth, Queens, and the $1.5 billion redevelopment of a mixed-use entertainment district around the Nassau Coliseum.

“The biggest theme of the past year is [portfolio] diversity,” Rechler said. “We’ve focused on investing anywhere we can create real estate solutions that help our customers and also help the community.”

While many have felt the heat of market competition in bids, RXR has more than held its own, from beating out traditional infrastructure funds for the JetBlue award to being the recipient of several off-market deals—thanks to the firm’s unique and varied development and investment expertise.

“We really focus on understanding our counterparty’s needs—whether it’s the customer or the community—and we try to do things that are win-win for the long term,” Rechler said. “It becomes a good calling card when others have challenging projects or developments in municipalities. They know when RXR is involved we’re going to do the right thing for the long term so that they’ll be successful, and that we’ll understand what their needs are and create something that meets their ultimate objective.”

Another big theme of the year for RXR was opportunity zones. As a master developer in many areas that fall into the designated zones in New York—such as New Rochelle, Yonkers and parts of Glen Cove—RXR is raising a $500 million opportunity zone fund.

“The strategy for us investing in these underserved, underperforming submarkets is consistent with what the opportunity zone program was put in place to do—to use investment to help revitalize and create economic vitality within these markets,” Rechler explained.

On the debt side, RXR’s been busy refinancing several of its properties, including an impressive double-header only two weeks ago. The company refinanced its Pier 57 redevelopment with a $375 million loan from Nuveen Real Estate, plus its 32 Old Slip office property with a $404 million loan from Mesa West Capital within 24 hours. Phew. The transactions were boosted by robust leasing activity from Google and law firm Cahill, Gordon & Reindel, respectively.

“Twenty-nineteen is not only about real estate and building the four walls but asking how do we activate what’s happening within those four walls—to maximize the experience for all of our customers and optimize the value of our properties. We’re continuing with our customer- and community-centric approach.”—C.C.

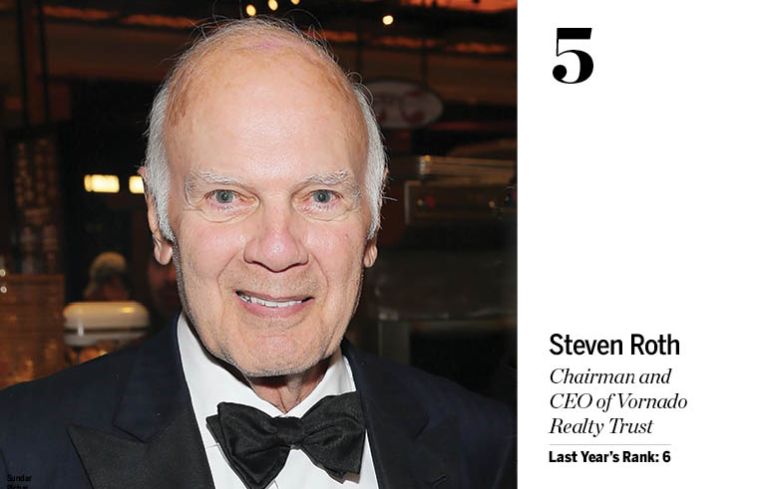

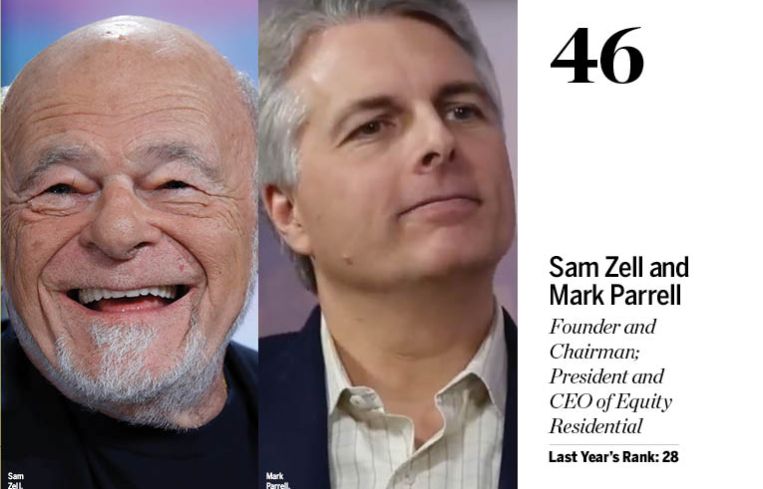

5. Steve Roth

Chairman and CEO of Vornado Realty Trust

Last Year's Rank: 6

Vornado Realty Trust is one of the real estate juggernauts that keeps on winning.

The company broke a national record last year for the most expensive home ever sold, when hedge funder Ken Griffin paid $238 million for the penthouse at 220 Central Park South. And now rumor has it that Amazon chief Jeff Bezos himself (in an ultimate trolling New York move) is scoping out a unit at the tower on Billionaire's Row.

This should be some comfort to Steve Roth. Earlier this month, in his annual letter to shareholders, Roth bemoaned New York's loss of the Amazon deal.

"Losing them was one of the stupidest damn things I've ever seen," he wrote. But not to fear, Vornado still came out a winner. A Vornado spinoff called JBG Smith is the largest property owner in Crystal City, Va. Amazon's new headquarters location, and Vornado shareholders received a 75 percent stake in that company when it was created.

"I, our senior management team and our board still retain every share that we received in the spin," Roth said.

Amazon aside, Vornado continued to move forward on several fronts in New York City, where it controls a portfolio spanning 26.8 million square feet.

According to Roth's letter, the proceeds from 220 Central Park Tower, which so far total $665 million for 23 units, will go towards the continuing work on the real estate investment trust's 9-million-square-foot portfolio along West 34th Street in the Penn Station area.

With Hudson Yards now open to the west, Vornado's Penn Plaza portfolio is well positioned to capitalize on the increased traffic and attention to the area.

In particular, Vornado is working on a plan for a two-building campus on the top of Pennsylvania Station, spanning 4.4 million square feet and rechristened Penn 1 and Penn 2. One block over, Vornado is moving forward on the Farley Post Office, where it paid $42 million to up its ownership to 95 percent from 50 percent in October 2018. Vornado anticipates delivering the office-and-retail complex in 2020.

Its plans for the Hotel Pennsylvania, for which futuristic renderings were leaked earlier this year, are on pause, the letter states. —C.G.

6. Rob Speyer

President and CEO of Tishman Speyer

Last Year's Rank: 7

It’s one thing to have your finger on the pulse of the city’s real estate market today. But leading major development deals requires you to know precisely where the market will be years down the line—a much more impressive knack. It’s precisely that ability that Tishman Speyer has cashed in on over the last year, seeing some of its boldest long-term projects pay off in a big way.

Start with The Spiral, the 65-story Bjarke Ingels-designed office tower at Hudson Yards that Tishman Speyer announced plans for in 2016. Construction only just started last year, but that didn’t stop Tishman Speyer from signing on Pfizer to lease 800,000 square feet in the tower when construction is finished in the early 2020s. Two weeks ago, the landlord also signed on AllianceBernstein as a tenant, bringing the total preleased space to 1 million square feet.

“We’re ahead of schedule,” crowed Rob Speyer. “That’s a real validation of our decision to take some architectural risk and develop a building that’s meant for the people who actually work there every day.”

If embarking on the giant tower has turned out to be a percipient venture, you can say the same for the company’s Jacx project in Long Island City, Queens, a 1.2-million-square-foot creative office complex set for completion this summer. Deals there with Macy’s, Bloomingdale’s and WeWork have enabled Tishman Speyer to fully prelease all the available space in one of the neighborhood’s first new office buildings in decades. Amazon Schmamazon.

“There were a lot of skeptics, but Long Island City has played out even more robustly than we expected,” Speyer said.

LIC is also an important residential sandbox for Tishman Speyer: The company is building Jackson Park there, a multifamily development with 1,800 rental units. All in all, Speyer said the company has 7 million square feet under development in the five boroughs.

“It’s the most activity in our history,” he boasted.

All of that raises an obvious question for such a prescient builder: Which neighborhoods is Tishman Speyer betting will be the next Hudson Yards or Long Island City?

Speyer responded the way any savvy developer would—by pleading the fifth.

“I can’t tell you that, man!” —M.Grossman

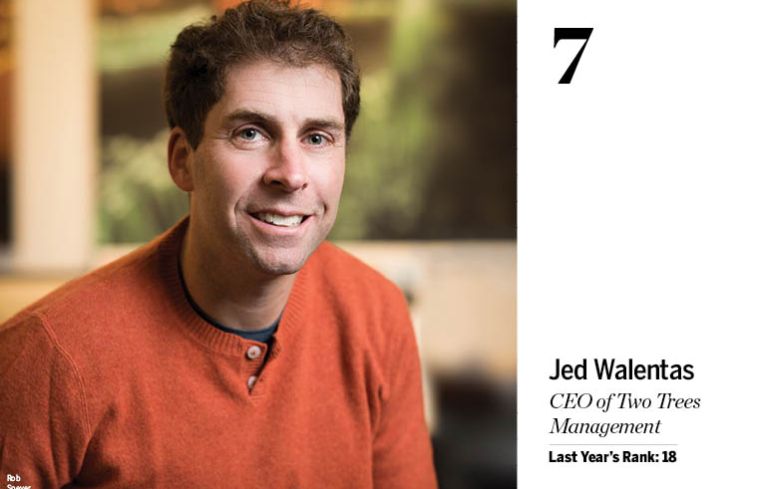

7. Jed Walentas

CEO of Two Trees Management

Last Year's Rank: 18

Jed Walentas’ vision for the Williamsburg, Brooklyn waterfront is taking shape.

Walentas’ Brooklyn-based Two Trees Management, which manages a real estate portfolio worth north of $4 billion, is making headway on its megadevelopment at the site of the former Domino Sugar Factory, which will transform a large chunk of the neighborhood.

“I think we figured out a way to create a business where our objectives and goals really align incredibly well with the communities where we work,” Walentas said. “It makes it way more fun to come to work every day when you’re not choosing between what you think is in your interest and what’s in the public’s interest.”

The new Domino Park, which stretches along the waterfront, opened in the summer of 2018, as did the first of the four buildings planned for the site, Shop Architects’ two-legged 325 Kent Avenue. The 522-unit building is fully leased, and the retail component opened with Misi, a nearly impossible-to-get-into restaurant from Michelin-starred chef Missy Robbins, sandwich shop Mekelberg and Modern Chemist, among other tenants.

Two Trees broke ground on the second building at the site, CookFox Architects’ 1 South First, and the skeleton is now fully formed, with the skin rising over it. The office and apartment building is scheduled to open at the end of 2019.

Two Trees also completed the lease-up at 300 Ashland Street, a 379-unit rental building in Downtown Brooklyn, secured 140 office leasing deals comprising over 250,000 square feet and was instrumental in bringing the Downtown Brooklyn Arts Festival to Downtown Brooklyn.

Walentas said, at the moment, his firm is primarily occupied with the design of the final two Domino buildings.

Two Trees also has holdings in Manhattan, including the 864-unit Mercedes House in Hell’s Kitchen, and the tech-friendly office building at 50 West 23rd Street in the Flatiron District.

He also said, since his company is independent, with no partners or institutional money, he’s able to answer only to himself and the public.

“It’s only me making decisions,” Walentas said, “so I get to decide,”—C.G.

8. Jonathan Gray, Ken Caplan and Kathleen McCarthy

President and COO; Global Co-Heads of Real Estate at Blackstone

Last Year's Rank: 9

New York City may have lost out on an e-commerce windfall when Amazon backed out of plans to open a new headquarters here last year, but that doesn’t mean Blackstone, one of the largest global landlords headquartered in the Big Apple, is missing out on the internet retail action.

Flexing its muscles as one of the best-capitalized real estate investment shops in the world, Blackstone, through its real estate investment trust, laid out $1.8 billion last March to buy a 22-million-square-foot industrial portfolio spread across the country—last-mile-distribution facilities that count Amazon as a key tenant.

But even that was small potatoes compared with its acquisition of Gramercy Property Trust, a $7.6 billion deal which closed in October 2018 that added 81 million square feet of industrial buildings from coast to coast.

“We’ve been very active in the logistics space,” Ken Caplan said. Quite the understatement.

A common thread that unites Blackstone’s diverse ambitions—the firm invested about $20 billion in real estate last year, as per Caplan—is to buy buildings where it’s hard to build new ones, eliminating the threat of oversupply. That’s why Blackstone also went on a shopping spree in 2018 for premier Hawaiian resorts. It spent $1 billion early last year on the Grand Wailea in Maui and finished the year by adding another luxe lodging along the island’s relatively scarce developable beachfront, the Ritz-Carlton Kapalua.

“It is hard to build hotels in certain resort markets, which has led to very limited new supply,” Caplan said. “We are buying irreplaceable hotels in some of these markets at meaningful discount to replacement costs.”

The company’s investments in New York City in 2018 couldn’t match that level of ambition, but Blackstone remains in control of heavyweight properties here as well: the massive 110-building Stuyvesant Town and Peter Cooper Village development on the Lower East Side, for one.

“We’ve really been focused on our residents and [on] enhancing the community and the whole property,” Caplan said.

One way was by adding solar panels to the complex’s roofs, a feature that helped make it the first LEED Platinum-certified apartments community in New York City.—M.Grossman

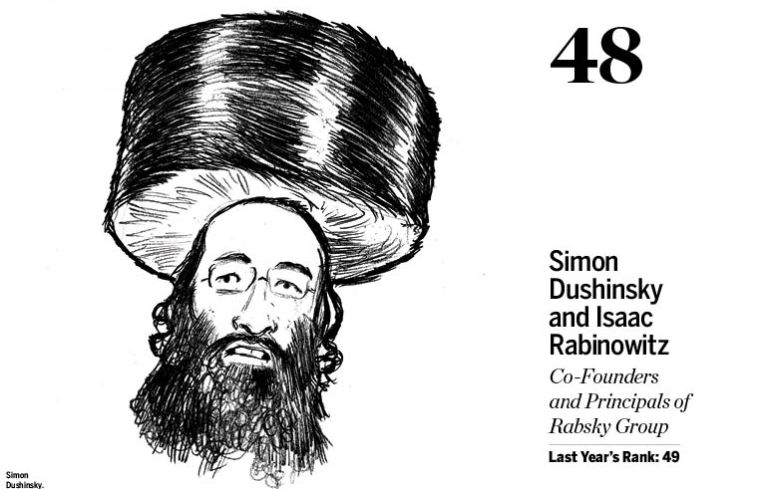

9. Douglas Durst and Jonathan "Jody" Durst

Chairman; President of the Durst Organization

Last Year's Rank: 11

The second phase of Durst Organization’s Halletts Point project in Astoria, Queens, may be stalled over a funding dispute with the city, but the family-owned development firm just opened the megaproject’s first residential building at 10 Halletts Point.

After completing just one partially affordable, 404-unit residential building, the century-old developer hopes to build four more mixed-income apartment towers at 20, 30, 40 and 50 Halletts Point, along with two entirely below-market buildings next door on New York City Housing Authority’s Astoria Houses campus.

Further south in Long Island City, Queens, Durst is also pouring the second floor on its 70-story, 958-unit residential tower at 29-37 41st Avenue, dubbed the Sven for Douglas Durst’s grandson. The development is 70 percent market-rate and 30 percent affordable housing at 130 percent area median income. Overall, Durst owns 2,500 apartments, with another 2,000 residential units under construction or in the pipeline.

On the commercial front, “It’s been an active year, and we’re pretty bullish on the market,” said Durst spokesman Jordan Barowitz. The company’s portfolio includes about 13 million square feet of commercial space. Of that, Condé Nast’s former space at 151 West 42nd Street is nearly 80 percent leased to new tenants, he said, and a separate Condé net lease for the entirety of 825 Third Avenue is set to expire this month. Durst plans to use the opportunity to reposition the 50-year-old building, which it attempted to market to investors as a ground lease last year. The firm also leased 225,000 square feet at 1 World Trade Center last year, bringing the building up to 80 percent rented.

Douglas Durst noted that the company’s 150,000 square feet of retail and office space on West 57th Street is also almost completely leased. It has successfully inked deals for 75,000 square feet of offices and 68,000 square feet of retail at the base of the buildings—VIA, Helena and Frank 57 West. He added that he was “concerned” about proposed rent-regulation reforms being mulled by the state legislature, which could negatively impact rent revenues for major owners and developers of rent-regulated housing like the Durst family.—R.B.R.

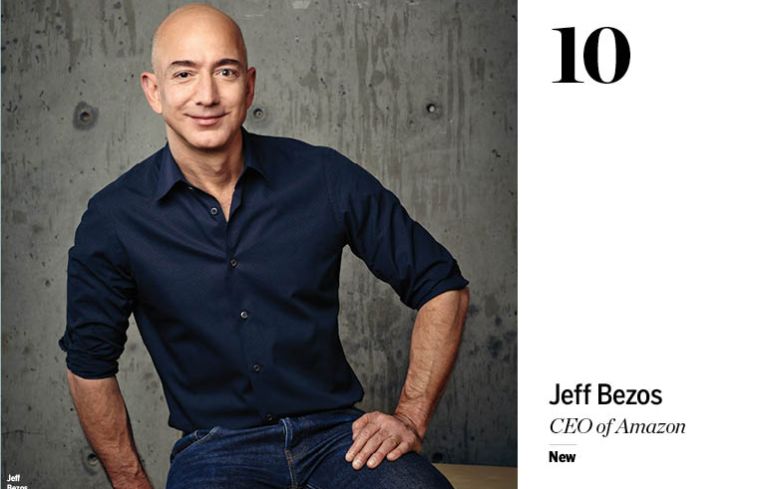

10. Jeff Bezos

CEO of Amazon

New

Not many people can throw an entire neighborhood’s real estate market into complete upheaval with just one decision, but Jeff Bezos did it—twice.

The CEO of Amazon put all eyes on Long Island City, Queens, when he announced in November 2018 that he would build an at least 4-million-square-foot campus in the waterfront neighborhood.

Amazon’s decision set off a flurry of activity in the neighborhood with brokers saying national brands were eyeing outposts in the area. The Wall Street Journal reported that people were buying residential condominium units sight unseen through text messages and that some Amazon workers closed on properties before the news was even made public.

A December 2018 StreetEasy report found that 18.8 available residential listings in Long Island City saw a price hike after the news broke, a turnaround from 2017’s declining sales and prices there.

While Gov. Andrew Cuomo, Mayor Bill de Blasio and groups like the Real Estate Board of New York heralded Amazon’s future arrival, Bezos also came up against local politicians like State Sen. Michael Gianaris and local activist groups like immigrants’ rights nonprofit Make the Road New York, who were concerned about the $2.5 billion worth of tax breaks given to Amazon from the city and state and worried that the influx of Amazon workers would displace long-term residents.

A little more than a week after Gianaris was nominated to the Public Authorities Control Board, which would have to approve Amazon’s plan, the e-commerce giant pulled out of the deal, saying, “A number of state and local politicians have made it clear that they oppose our presence and will not work with us to build the type of relationships that are required to go forward with the project.”

Real estate brokers in the neighborhood mourned the loss with reports surfacing about homebuyers trying to back out of deals made when Amazon was still coming.

Even without Amazon’s headquarters, New York City might not be done with Bezos. The company still has a distribution warehouse on Staten Island, and The New York Post reported this month that Bezos was in talks to buy a $60 million apartment at 220 Central Park South.—N.R.

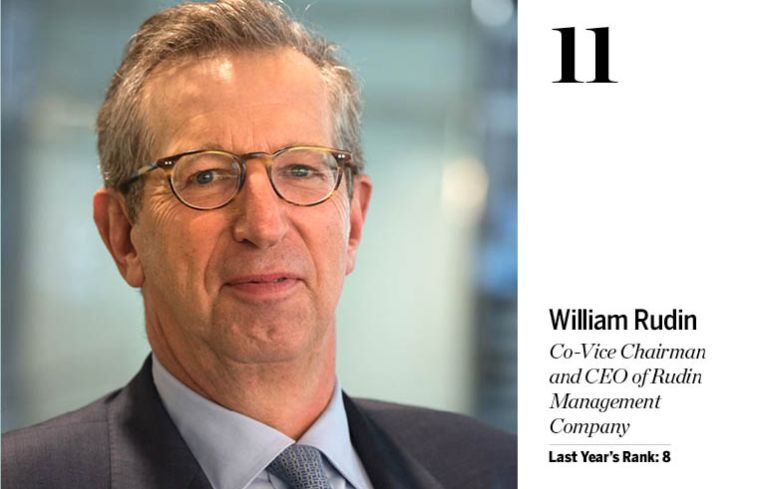

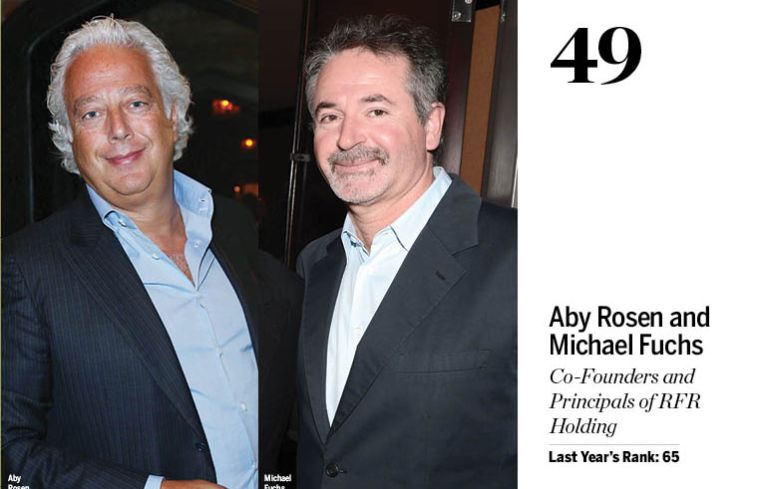

11. William Rudin

Co-Vice Chairman and CEO of Rudin Management Company

Last Year's Rank: 8

William Rudin wears two very powerful hats in the real estate business.

First, there’s the one he wears as head of Rudin Management Company, one of the blue-chip landlords of Gotham with (as per the firm’s website) some 36 properties consisting of 4.7 million square feet of residences and another 10.2 million square feet of office space.

Last year, 2018, was “pretty strong and robust,” Rudin said. He inked solid leases like Blackstone’s 148,587-square-foot expansion at 345 Park Avenue in December; Dorilton Capital’s expansion to 33,500 square feet at 32 Avenue of the Americas and the Gersh Agency’s taking of 28,000 square feet at 41 Madison Avenue.

All the while, Rudin (as well as his children Michael and Samantha, both senior vice presidents who “continue to expand their roles,” per Rudin, and his cousin, Eric, co-chairman and president) has been overseeing the tweaking and updating of the empire, from renovating properties like 211 East 70th Street, 55 Broad Street and 41 Madison Avenue; to rolling out the company’s smart building platform called Nantum and investing in tech companies like Latch; to getting the final preparations underway for the summer opening of Dock 72 in Dumbo, Brooklyn.

But there is another hat that Rudin wears as the chairman of the Real Estate Board of New York—a role that has grown more complex in the last five months.

“Last year was a major transition in terms of Albany and the change in power,” Rudin said. “We at REBNY are working very hard with the new leadership to make sure that [as issues such as] rent regulation start moving forward that there’s an understanding of the economic drive of what real estate produces for our city and state.”

Given the proclivities of the new class of state senators and city councilmembers, Rudin and REBNY President John Banks will have their work cut out for them. However, they’ve already gotten points on the board, getting firmly behind Gov. Andrew Cuomo’s congestion pricing proposal and beating down Mayor Bill de Blasio’s flirtation with a commercial vacancy tax. Plus, REBNY no doubt feels comfortable with Vicki Been as de Blasio’s choice to replace Alicia Glen as deputy mayor—a critical role as the state senate tackles affordable housing.

“Vicki Been is a great choice,” Rudin said. “She’s well versed in housing and we look forward to working with the deputy mayor designate—it’s a very strong signal in continuing…what Alicia Glen did with affordable housing.”—M.Gross

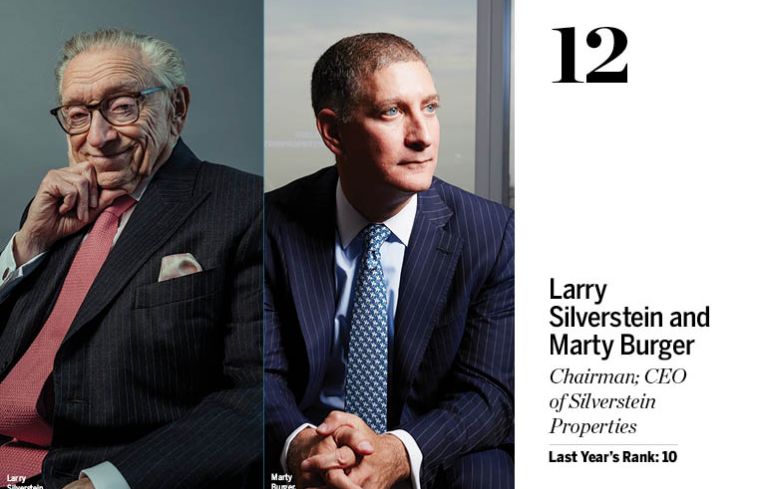

12. Larry Silverstein and Marty Burger

Chairman; CEO of Silverstein Properties

Last Year's Rank: 10

ABC, easy as 123? Silverstein Properties certainly makes it appear so. The company closed on the $1.2 billion acquisition of the Walt Disney Company-owned ABC campus on the Upper West Side in July 2018, but that was only the tip of the iceberg in terms of its activities.

“That deal was very exciting,” Marty Burger said. “It’s a very coveted site because your front door is Lincoln Center and your back door is Central Park. We were very fortunate and privileged to have won that [transaction].”

Downtown at 120 Broadway, the company has been busy marrying the old-world feel of a 1915 property with the needs of 21st-century tenants.

“We’re restoring the building to its original magnificence and making it shine all over again,” Larry Silverstein said. “It’s a historic landmark, it’s unique and special and it’s totally different from the buildings of steel and glass that we’re building at the [World] Trade Center.”

Speaking of which, the firm opened the 2.5-million-square-foot 3 World Trade Center last June with three tenants and has been racking them up ever since. Most recently, accounting firm Dixon Hughes Goodman leased 12,000 square feet at the property.

“We’re very busy. For the first time in a really long time we have nothing under construction, but all of our projects are doing great and we’re about to start the next phase of new developments,” Burger said.

The firm was also busy funding projects—its own as well as others’.

In May, Silverstein launched its first capital raise on the Tel Aviv Stock Exchange, reaching $175 million. The issue was oversubscribed, with demand doubling the amount Silverstein sought to raise. And in October, it launched its financing arm, Silverstein Capital Partners, bringing on Michael May to lead the charge. The firm financed its first deal in November—a $240 million mezzanine loan for JDS Development’s mixed-use development at 9 Dekalb Avenue in Downtown Brooklyn—and has several more in the pipeline, Burger said.

And despite Silverstein’s deep Big Apple roots, the right market isn’t always New York (gasp!). This March, it partnered with Arden Group and Migdal Insurance in a $452 million purchase of a Class A office building at 1735 Market Street in Philadelphia.—C.C.

13. Michael Turner and Dean Shapiro

President; Head of U.S. Development at Oxford Properties Group

New

“We were the inverse” of Amazon, Michael Turner said. “New York’s quiet victory with Google.”

Quiet is definitely the proper word. There were no nationwide competitions. No fawning mayors or governors slavishly singing the CEO’s praises. There were no tax controversies, no political backlash, no public rebuke and humiliation—nothing except for a dizzying real estate deal the likes of which most developers would kill for.

We’re speaking, of course, of Google’s $1 billion decision late last year to forge a 1.7-million-square-foot campus in Hudson Square—specifically at Oxford’s St. John’s Terminal at 315 and 345 Hudson Street and 550 Washington Street.

It’s the kind of deal that Turner, who became the president of Oxford last year, and Dean Shapiro would be happy to hang their hat on, but wait—did we also mention that this is the year that Hudson Yards opened? Though Related Companies gets the glory, Oxford has partnered with Related since 2010 to develop the 28-acre, 18-million-square-foot mini-city, the first phase of which had its premiere party last month.

“The world looked very different when we came on board,” Turner said. “But we believed in the project. It was a moment of pride to see that come to life.”

Call it Canadian politeness or modesty, but the quiet work has continued. With very little fanfare, Oxford—the real estate arm of the Canadian pension fund Omers, which owns some 104 million square feet of real estate and has $60 billion of assets under management—has built a mezzanine loan operation out of its New York office and has continued picking up property in Boston and Washington, D.C. and bought a $3.5 billion stake in logistics company IDI.

“On any given day, we have a $2 billion book,” Turner said, adding that “a sweet spot for us is $100 million to $300 million.”

But don’t expect the company to rest on their laurels.

“Execution matters,” Turner said. “We have to deliver beautifully at St. John’s. Our team will be laser-focused on all the elements of these large and complicated projects.”

—M.Gross

14. Jeff Sutton

Founder and President of Wharton Properties

Last Year's Rank: 19

The name “Jeff Sutton” is so deeply entwined with Fifth Avenue retail that you’d be forgiven for thinking that Wharton Properties was having a bad year given how much of a shellacking the famous strip has taken of late.

You’d be wrong.

Sutton has largely escaped the headline closings—from Henri Bendel to Versace to The Gap—that have flayed his peers. But to a certain extent, the Brooklyn-born real estate hustler has gone back to his roots; he’s been grinding out creative leases like the Tiffany & Co. sublease at 6 East 57th Street while the jeweler commences a three year renovation of its flagship (the Trump Organization owns the building, but Sutton made a deal with Niketown—the original tenant—to relocate the sports apparel company to his 650 Fifth Avenue, which included taking over the empty space), and it was the largest retail deal in the city last year.

He’s also doing the respectable office leases, like 49,000 square feet to Knotel at 530-536 Broadway, and outer-borough retail ones, like a Sephora at 429 86th Street in Bay Ridge, Brooklyn. (Wharton did 19 leases last year.) He also picked up properties in Brooklyn, Queens and the Bronx (a dozen in total) and refinanced 17 buildings. And, of the many American developers who have tried their luck on the Tel Aviv Stock Exchange, Sutton is one of the few to have emerged unscathed. After a tiny blip back in December, his bonds are trading at 4.4 percent yields (the highest all year).

But the most interesting play the developer has undertaken was buying out SL Green Realty Corp.’s stake in 724 and 720 Fifth Avenue last summer. (The exact terms of the deal were not released, but the properties were a part of an eight-parcel package SL Green and Wharton bought in 2012 from David Frankel Realty for $416 million, as The Real Deal originally reported.)

What could Sutton do with the property?

While we wouldn’t want to traffic in speculation, it should be noted that Sutton owns the air rights to produce something truly towering, and truly spectacular—and he has the means to build it. Rather than one of the supertall condos of West 57th Street for the billionaire set (which was never his modus operandi) he could conceivably do a supertall office building. A boutique, luxury office tower with a schmancy design, perhaps? Just remember, you heard it here first.—M.Gross

15. Mary Ann Tighe

CEO of the New York Tri-State Region for CBRE

Last Year's Rank: 18

After more than three decades in the commercial real estate business, Mary Ann Tighe isn’t slowing down one bit. Over the past year, the 70-year-old head of CBRE’s tri-state business has done 5.7 million square feet of office deals, including several hundred thousand square feet of leases outside the U.S. Her team has leased 98 percent of the 1.9-million-square-foot former Time & Life Building at 1271 Avenue of the Americas. Law firms Blank Rome and Latham & Watkins collectively took 550,000 square feet in the property last year, and wealth manager Bessemer Trust took another 239,000 square feet. At the newly opened 3 World Trade Center, Tighe and her crew from CBRE nailed down big leases with McKinsey, Hudson River Trading, Casper and Diageo, just as media conglomerate GroupM moved into its 700,000-square-foot offices in the 2.5-million-square-foot tower.

On the Far West Side, Tighe helped seal a 99,337-square-foot lease for Regus’ trendy Spaces coworking brand at Georgetown Company’s redeveloped 787 11th Avenue.

The one-time art historian also leased various foreign office spaces for GroupM parent company WPP, including a 14,500-square-foot outpost in Bogota and a 258,300-square-foot one in Toronto, along with a 45,513-square-foot location in Mexico City for WPP subsidiary Young & Rubicam.

Her forecast for the office market is surprisingly upbeat.

“Normally the first quarter is the quietest period in the market,” she said. “But this has been the most explosive start to the year, coming off a record-breaking leasing year of 32 million square feet in New York City.”

However, she predicted that landlords had overbuilt amenities like exercise rooms in new office developments and would eventually have to find new uses for some of that space.

“I think we’re all gonna have a laugh [about the excess of amenities] in a few years.”—R.B.R.

16. Adam Neumann and Miguel McKelvey

Co-Founder and CEO; Co-Founder and Chief Creative Officer, The We Company

Last Year's Rank: 14

Founded by Adam Neumann and Miguel McKelvey in New York City, the privately held WeWork has become an amoeba, dividing and colonizing real estate and companies at breakneck speed, in between launching new business lines like last year’s WeWork Labs, a program dedicated to helping early stage startups grow, and WeMrkt, a market stand featuring member products.

Working hard to distance itself from its 2010 coworking roots, the company this year rebranded as the We Company. And it boasts that large companies—those with 1,000-plus employees, like IBM, Microsoft, Standard Chartered, GE, NASDAQ, HSBC, Salesforce, Liberty Mutual and UBS—now represent 32 percent of WeWork’s membership.

And that’s a membership that exceeds 400,000 across 425 locations in 100 cities and 27 countries globally.

WeWork started off the year with a $2 billion investment from SoftBank Group, and while $14 million less than anticipated, it was still a sizable sum. (The $2 billion brought the Japanese bank’s total investment in the company to more than $10 billion.) In February, WeWork and partner Rhône Capital announced that they closed their $850 million purchase of the iconic former Lord & Taylor flagship location at 424 Fifth Avenue, more than a year after announcing the acquisition.

The same month WeWork picked up data platform Euclid for an undisclosed amount, TechCrunch reported, and this month WeWork acquired five-year-old office management startup Managed by Q, as Commercial Observer reported.

Two 2018 acquisitions that point to WeWork’s diversification include office management startup Teem in September for $100 million in cash and marketing company Conductor.

And all of that is on top of the fact that WeWork offers fully furnished apartments via WeLive, owns Flatiron School (a coding bootcamp it purchased in a mostly stock deal worth more than $40 million at the time in October 2017), and Meetup (the online group organizer that it bought in November 2017 for a reported $30 million).—L.E.S.

17. MaryAnne Gilmartin, Robert Lapidus and David Levinson

Co-Founder and CEO of L&L MAG; Co-Founder of L&L MAG, President and CIO of L&L Holding Company; Co-Founder of L&L MAG, Chairman and CEO of L&L Holding Company

Last Year's Rank: 26

A little more than a year after MaryAnne Gilmartin joined L&L Holding’s Robert Lapidus and David Levinson to form L&L MAG, it’s all systems go.

The development company announced its first project in December 2018, a 460-unit residential building at 241 West 28th Street in Chelsea, and this March was tapped to develop a long-vacant waterfront parcel in Long Island City, Queens, into a mixed-use development.

“The honeymoon period may be over, but the marriage is strong,” Gilmartin said. “We feel really good about the partnership.”

It wasn’t just the recently formed L&L MAG side of the business making moves. L&L Holding closed its $880 million acquisition of the 1.3-million-square-foot Terminal Stores with Normandy Real Estate Partners in last fall. The company plans to redevelop the 128-year-old warehouse building into an office and retail destination, all while maintaining its historic character.

“It’s really the ultimate counterpoint to the glass and steel that we build,” said Levinson, adding Terminal Stores has columns made with trees older than the United States. “This is an authentic building with brick and wood.”

L&L Holding also topped out its 897-foot-tall 425 Park Avenue office development, announced plans for a $2.5 billion redevelopment of the Times Square hotel-and-retail development TSX Broadway with a 17,000-square-foot LED billboard, and opened the redeveloped 32-story 390 Madison Avenue—leasing 436,905 square feet to J.P. Morgan Chase in March 2018.

“We’re not in the commodity real estate business,” Lapidus said. “The specialty space does really well, the commodity stuff suffers.”

In the past three years, both L&Ls had nearly 100 new people join—with 75 percent of L&L MAG made up of women—along with five weddings and eight new babies, Gilmartin said.

For next year, the companies plan to focus on finishing their millions of square feet under development and building up their multifamily portfolio.—N.R.

18. Darcy Stacom and William Shanahan

Chairman and Head of New York City Capital Markets; Chairman of New York City Capital Markets, CBRE

Last Year's Rank: 24

“No matter how anyone writes the story, we grossly exceeded our clients’ price expectations in a very creative auction,” Darcy Stacom said about the Chrysler Building deal.

The story, however, is very interesting. RFR Realty and Signa Holding GmbH acquired the leasehold for the Chrysler Building for $151 million in equity from Tishman Speyer and Abu Dhabi Investment Council (ADIC). While the sum seems paltry compared with the $800 million Tishman Speyer cleared when it sold a 90 percent stake in the iconic skyscraper at 405 Lexington Avenue to ADIC at the height of the market in 2008, it’s not a bad number considering the ground lease is owned by the Cooper Union school (with an annual rent of $32 million, which should reset to $55 million in 2049) and the building requires about $200 million in renovations.

Stacom previously told Commercial Observer that, with Chrysler closing, as well as other properties like 0 Bond Street signed and closed this year (Paramount sold it to Cara Investment GMBH for $130.5 million), Savanna acquiring 521 Fifth Avenue from SL Green for $381 million, and J.P. Morgan buying Bank of China’s 410 Madison Avenue for $100 million—all deals she and partner William Shanahan negotiated—“The market feels very alive and well right now.”

The pair is involved in many of the city’s biggest deals. Last year’s included Google’s $2.4 billion purchase of the Chelsea Market building and the $800 million sale of Terminal Markets.

“I spent nine months negotiating directly with Jamestown for Chelsea Market,” Stacom said. “That was the one that took the most time.”

Stacom said her most exciting transaction of the $6.6 billion in deals the team closed last year was Terminal Markets.

“Everyone had tried to buy it for 30 years and we managed very quietly to pick a limited number of people to go to. We sold it for $880 million, less than a 2-cap, to L&L [Holding Company] and Normandy [Real Estate Partners] basically in the cover of darkness. It’s the largest asset I’ve every sold without being able to do investor tours. It was the largest single-asset outright investor sale last year.”

To boost the strength of their team—now at 14 professionals and six support staff—the power duo hired “three senior people from three major organizations to really create the future of the team,” as Stacom said. Those were David Fowler from HFF and Sheryl Waldorf from what was TH Real Estate last year and Doug Middleton from Eastdil this year.—L.E.S.

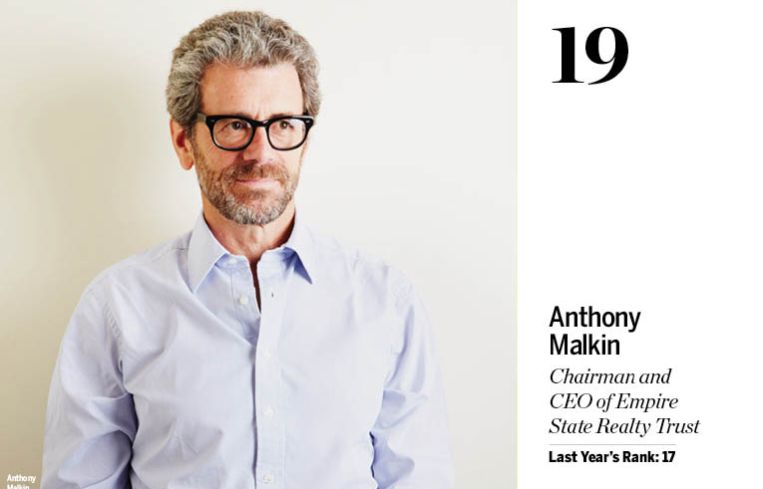

19. Anthony Malkin

Chairman and CEO of Empire State Realty Trust

Last Year's Rank: 17

Empire State Realty Trust had a bit of a viral moment last year.

Rapper Eminem performed his song “Venom” at the top of the company’s trophy asset, the Empire State Building, in October 2018 for Jimmy Kimmel Live! and the video got more than 9 million hits on YouTube alone.

“That’s a huge thing for our brand,” said Anthony Malkin. “And [the video] continues to build on the brand of our Empire State Building.”

But viral fame wasn’t the only accomplishment for ESRT. The company, which celebrated its fifth year since going public in October 2018, signed more than 1 million square feet of leases last year and had its cash rent spread for new deals climb to 27 percent.

Large deals included Signature Bank taking 111,872 square feet at 1400 Broadway, Uber grabbing 34,600 square feet in the same building and Nespresso’s 41,800-square-foot lease at 111 West 33rd Street. At the Empire State Building, LinkedIn took another 30,165 square feet, bringing its total footprint in the property to 312,947 square feet.

“The whole portfolio is really cranking,” Malkin said.

ESRT also opened up the first phase of its $150 million makeover to the Empire State Building, which included moving the visitor entrance from Fifth Avenue to West 34th Street.

“It’s a tremendous improvement of efficiency and flow for our tourist visitors,” Malkin said. “It returns the Fifth Avenue lobby to the tenants.”

ESRT unveiled a new, larger lobby at 20 West 34th Street and renovated the observation deck. The makeover encompasses a VIP guest room, restoring the granite flooring and adding digital ticket kiosks.

Malkin is currently focused on finishing the Empire State Building’s observation project by October and getting to work on “a lot of leasing to do” in the building. But still, don’t expect ESRT to announce deals with WeWork anytime soon.

“We’re not suffering by not leasing to the coworking and enterprise space providers,” said Malkin, who has been known to publicly share his disdain for WeWork. “We provide our tenants with a better experience by giving them the sort of services, security and quality that they don’t get in buildings that had coworking.”—N.R.

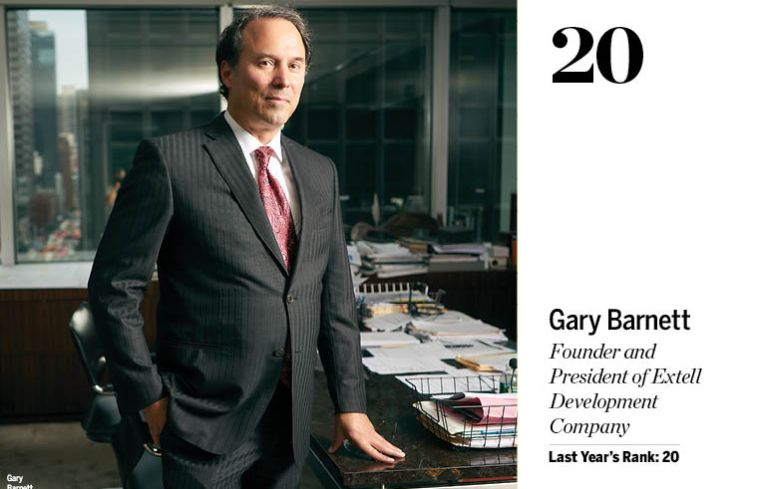

20. Gary Barnett

Founder and CEO of Extell Development Company

Last Year's Rank: 20

Gary Barnett’s Extell Development Company has amassed a tremendous footprint in Manhattan with a slew of visible and daring luxury condominium developments throughout the city. Barnett is only satisfied with being number one—his developments include Manhattan’s most expensive residential tower, Brooklyn’s tallest residential tower, and the Lower East Side’s largest housing complex.

In 2018, Barnett successfully financed his ongoing developments, and leasing launched at three of Extell’s projects including the Central Park Tower, Brooklyn Point and The Lofts at Pier Village in New Jersey. But the real trick will be selling the hundreds of units in the company’s pipeline in an ever-more precarious luxury condominium market.

That process will be overseen by Extell’s new CEO, 42-year-old Sush Torgalkar, formerly the COO of Westbrook Partners.

Central Park Tower, the 98-story super-luxury supertall on Billionaire’s Row, is nearing completion and Extell is projecting total revenue of $4.5 billion from its 179 apartments—the largest sell-out ever in the city—which works out to an aggressive $7,450 per square foot, according to financial documents filed by the company.

At Brooklyn Point, Extell’s first development in Brooklyn and the tallest residential building in the borough, Barnett secured the $530 million he needed to complete the 68-story project, which topped out earlier this month. Amenities at the building will include a 35-foot rock climbing wall, and a rooftop infinity pool—the highest in the Western Hemisphere.

Meanwhile, at One57, Extell’s other tower on Billionaire’s Row, which opened its doors in 2014, 13 units sold for a total of $135 million in 2018 and the first quarter of 2019, with 28 still to go.

Extell is also moving forward on its Upper West Side project at 36 West 66th Street, where it’s waiting on approvals for its 150-foot mechanical voids, on what will be, unsurprisingly, the neighborhood’s tallest residential tower, rising 775 feet.—C.G.

21. Douglas Harmon and Adam Spies

Co-Chairmen of Capital Markets at Cushman & Wakefield

Last Year's Rank: 29

If salespeople sell things, then what’s the word for people who sell really, really big things? Ginormasalespeople? Salespeople, Mega Division?

Whatever the term, Douglas Harmon and Adam Spies, Cushman & Wakefield’s investment sales super-brokers, are it. If a deal is going to run into the nine (or even 10) figures, then chances are great that Harmon and Spies are on it. For 2018, that meant representing Jamestown, the seller of the Chelsea Market building to Google, for $2.4 billion.

It also meant representing the sale of Starrett City—officially called Spring Creek Towers—to Brooksville Company and Rockpoint Group for $905 million. That sale included 46 buildings that sit on 145 acres adjoining Jamaica Bay in East New York, Brooklyn. With more than 5,000 apartments, Starrett City is so big that it has its own strip mall; it has its own power plant. Unsurprisingly, the transaction was the largest individual multifamily property sale in the U.S. last year.

The two brokers of Really Big Things have complementary backgrounds; Harmon was a rock star early on, selling the Helmsley portfolio in the 1990s when he was just 35. His partner Spies, meanwhile, is known as a numbers nerd, having started his career as an accountant at one of the then-Big Six firms.

Years of homework and pattern recognition got the two to where they are now.

“Insight is a much more effective weapon if it’s loaded with a wealth of experience,” Harmon said.

The Starrett City transaction, for example, was a deal that took a decade to unfold; the attempted 2007 sale of the same complex had been twice rejected by the U.S. Department of Housing and Urban Development. Perhaps as a reaction, Harmon noted that his 2018 sale of Starrett City was carefully solved for all stakeholders.

The team’s experience in brokering the sale of Stuyvesant Town and Peter Cooper Village, and advising servicer CWCapital Asset Management, for $5.4 billion in 2015, helped too.

“These days we can more often see potential deal obstacles hiding in plain sight,” Harmon noted, “If you can spot a problem that could derail a deal, or slow down a deal ahead of time, it’s easier to solve or navigate around it.”—A.R.

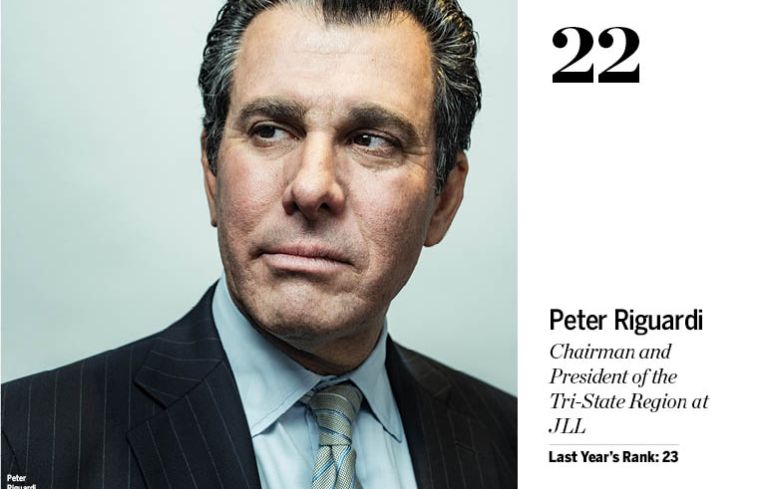

22. Peter Riguardi

Chairman and President of the Tri-State Region at JLL

Last Year's Rank: 23

Peter Riguardi closed out 2018 by inking the second-largest office deal of the year—Deutsche Bank’s 1.1-million-square-foot headquarters at Related Companies’ Time Warner Center.

After five years of working with the German bank, Riguardi and his team were able in December 2018 to sign a 25-year lease with Related for the majority of the office portion of the building—except for the 20th floor—along with the naming rights.

“It was an amazing choice for branding,” Riguardi said. “It was a great choice to retain and recruit top talent.”

The president of JLL’s New York region has been on a winning streak the past several years and netted more than 5 million square feet of leases around the city in 2018, a 15 percent increase from the year before.

Aside from the monster Deutsche Bank lease, Riguardi and his team negotiated the buyout of J.Crew’s $35 million, 370,000-square-foot space at 770 Broadway by Facebook and J.Crew’s relocation to 350,000 square feet at Brookfield Place. He also saw a flurry of leasing activity at Fosun International’s 28 Liberty Street, including information services company Wolters Kluwer’s 130,000-square-foot lease and the London Stock Exchange’s 75,000-square-foot deal.

“The largest occupiers and landlords, before they make a decision on what they want to do, are talking to us,” Riguardi said. “Our batting average is getting better and we’re winning those businesses.”

Riguardi said he is finalizing some big leases from “household names” in the coming months. And while he doesn’t foresee inking a deal as large as Deutsche Bank’s this year, he expects he’ll be able to match the amount of square footage leased in 2018. But it’s not just the brokerage side where Riguardi is doing well.

JLL’s tri-state office had its business grow by 20 percent in 2018, with the addition of 100 people including Robert Knakal’s 53-person investment sales team, Riguardi said. The brokerage plans to add at least another 75 brokers this year and continue to increase its market share.

“We’re ambitious,” he said. “We’ve got a great team. Most of our top people are in the prime of their career and we got a great rising group.”—N.R.

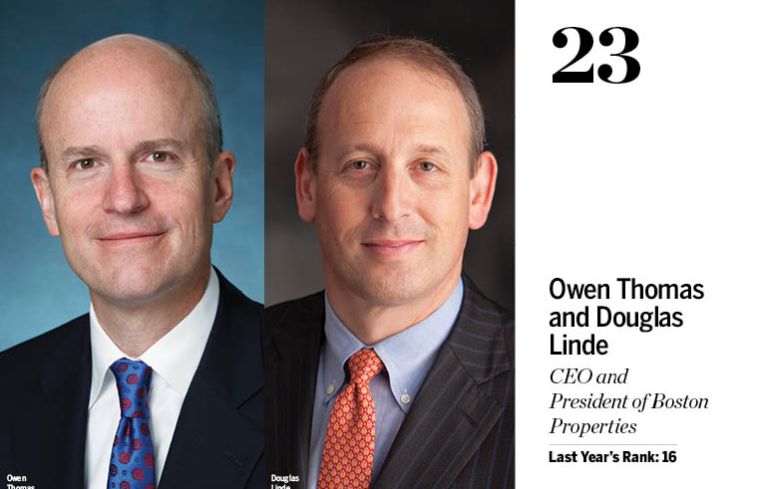

23. Owen Thomas and Douglas Linde

CEO and Preisdent of Boston Properties

Last Year's Rank: 16

Last May’s early completion and stabilization of Salesforce Tower in San Francisco, a new, 61-story, 1.4-million-square-foot development—already 100 percent leased—is part of what made 2018 such a great year for Owen Thomas and Douglas Linde of Boston Properties.

“Salesforce Tower is a prime example of what BXP does best: develop, deliver and manage complex, marquee, Class-A properties in markets with strong underlying economic driver,” said Thomas, who has been partners with Linde since joining the firm six years ago.

On our side of the world, as lender and developer, the team entered into a joint venture with the Moinian Group, providing $80 million of mortgage financing in debt to refinance a loan to acquire a development site at 3 Hudson Boulevard that can accommodate up to 2 million square feet of future development.

Said Linde, a 22-year veteran of the firm, “We continue to grow our presence in New York as we believe the market has strong underlying demand and offers attractive, long-term growth opportunities, even as new supply comes online.”

The team, which achieved 93 percent leasing at the 1.7-million-square-foot 399 Park Avenue, expects demand for New York City properties and new developments to continue this year, including at Boston Properties’ Hudson Yards site (the square block between 11th Avenue and Hudson Boulevard Park from West 34th to West 35th Streets) with the anchor tenant to begin development.

—S.P.

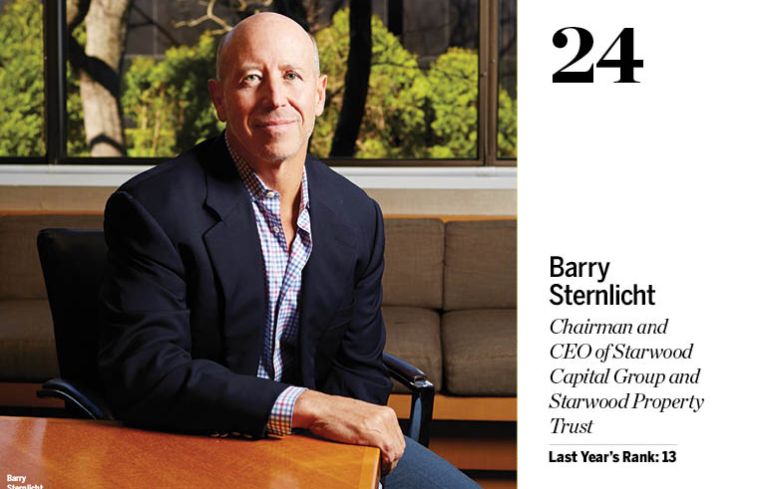

24. Barry Sternlicht

Chairman and CEO of Starwood Capital Group and Starwood Property Trust

Last Year's Rank: 13

With $56 billion in assets under management, Barry Sternlicht’s Starwood Capital Group bends the space-time of the real estate industry like few other American property owners. Even fewer source global opportunities with as much persistence—a reputation Starwood lived up to again in 2018. Add in Starwood Property Trust, a mortgage-focused real estate investment trust that Sternlich also controls and that lent a record $9 billion last year—and you have a veritable powerhouse on your hands.

“It was one of our biggest years ever buying and selling,” Sternlicht said. “Last year, we did $4 billion in acquisitions and $8 billion in sales.”

Underscoring the firm’s deep roots in the hospitality industry—after all, this is the company that launched W Hotels and, more recently, 1 Hotels—Starwood shelled out $225 million late last year to buy the St. Regis Princeville Resort on the Hawaiian island of Kauai, which it will rebrand under the 1 Hotels flag (a project slated to cost another $100 million).

And as always, there’s been a steady stream of more buttoned-down, but just as big, domestic acquisitions. This month, Sternlicht’s firm laid out more than $500 million to buy a pair of big city office towers. First, it picked up Minneapolis’ Wells Fargo Center, a 1.2-million-square-foot building in the city’s downtown, for $314 million, in an acquisition from Hines and Blackstone. Then, just last week, Starwood plunked down $227.5 million to buy a 711,000-square-foot office complex in Atlanta from Columbia Property Trust. The company is also at work on a giant office complex in Miami, and reports have suggested it aims to move its headquarters there from Greenwich, Conn.

But Starwood hasn’t limited its appetite just to American shores. In March, Starwood announced it would expand its 1 Hotels brand—a vertical that blends sustainability and luxury—with a new outpost in Melbourne, Australia, that will open in 2022.

Starwood has also turned its attention to opportunity zones, the federally designated neglected areas where, under 2017’s tax reform, developers will get tax incentives for major investments.

“It’s no secret that we’re aggressively looking at opportunities [in that space]. It’s sort of additive to what we do already,” Sternlicht said. In January, the company hired Anthony Balestrieri, formerly of MetLife Real Estate Investors, to guide its opportunity zone investments.

Though it didn’t notch any big acquisitions in New York City last year, Sternlicht’s hometown is still very much on his radar screen. After all, the company announced it would open its first-ever office here just last month: a 14,000-square-foot space at 40 10th Avenue.—M.Grossman

25. Jimmy Kuhn, Barry Gosin and David Falk

President; CEO; President of New York Tri-State Region at Newmark Knight Frank

Last Year's Rank: 30

As soon as Jimmy Kuhn picks up the phone, he knows where he wants the conversation to go.

“I want to talk about the significant capital markets business last year,” he said. “Our debt team knocked it out of the park—probably did $13 billion in debt in 2018. This goes to what we’ve done over the last five years in capital markets since we bought ARA [Apartment Realty Advisors] in 2014.”

But Newmark, which integrated ARA and its Berkeley Point Capital business into the Newmark brand last October, has a lot to discuss for 2018, the biggest being the $1.5 billion portfolio sale, which included over 2,000 apartments in New York City, from the Jack Parker Corporation.

The year’s biggest deal for NKF was the sale of the $1.5 billion Parker Portfolio, including over 2,000 apartments in New York City, to various buyers from the Jack Parker Corporation. NKF also represented both sides in the sale of 7 Hanover Square from Guardian Life to GFP Real Estate for $310 million in January; worked on behalf of NYU Langone in the sale of Shore Hill Housing, a two-building, 558-unit senior housing complex in Bay Ridge, Brooklyn, for $150 million in November; and represented Jack Resnick in the lease of 279,000 square feet of office space at 315 Hudson Street to Google in December.

“The summary,” said Kuhn, “is that we sold about $3 billion worth of product in the marketplace in New York City last year.”

On the leasing front, the company took on the final stage of leasing for 1 World Trade Center, representing NYC Health and Hospitals for its 25-year lease for over 525,000 square feet at 50 Water Street and represented Jack Resnick in his leasing of 279,000 square feet at 315 Hudson Street to Google.

The company looks to growth in the year ahead in several areas. It acquired RKF Retail Holdings in September, bolstering its national retail business with the addition of 70 brokers. Big things are also expected of the company’s new hospitality team after it hired Adam Etra, Mark Schoenholtz, Lawrence Wolfe and Miles Spencer away from Eastdil. Newmark is also developing an internally crowd-sourced database that will connect all of the company’s service lines and business units. And it also expects to see growth in the life sciences department.

“With the growing business in technology, data centers and life science, we are building up our global practice groups in these three areas,” Kuhn said. “After San Francisco and Palo Alto, New York is fast becoming the [next] hub for technology. The [New York Economic Development Corporation] has had a huge initiative to bring life sciences here. What’s really important is that Newmark continues to be an entrepreneurial firm cloaked in a corporate structure. We think about businesses, we think about where trends are going, and then we give our brokers the tools to build businesses and practice groups that are relevant to what’s going on in the economy.”—L.G.

26. Ron Moelis, Lisa Gomez and David Dishy

CEO; COO; President of Development and Acquisitions at L+M Development Partners

Last Year's Rank: 31

Powerhouse affordable development firm L+M Development Partners is so busy that its COO, Lisa Gomez, can barely keep track of all the projects she oversees. With 15 developments and 2,000 new apartments under construction across the five boroughs, the firm has its fingers in nearly every low-income swath of New York City.

Among its new construction projects are two buildings with 219 affordable apartments and 95 supportive units for the formerly homeless in the Belmont section of the Bronx. The complex, which is being built on land owned by nearby St. Barnabas Hospital, will include an ambulatory care center, primary care offices and a wellness center, along with a day care, café and rooftop farm. Gomez called it a “model project” that will show “how housing can help chronically sick people and emergency users.”

The company is also working on large affordable developments in the Kingsbridge Heights and Soundview sections of the Bronx, as well in East Harlem.

In addition, L+M is building a 446-unit affordable complex on Surf Avenue and West 19th Street in Coney Island, Brooklyn, as well as a below-market-rate, 127-unit building designed to passive-house standards in Rockaway, Queens. The developer is also revamping roughly 3,000 units of subsidized housing in New York City and San Jose, Calif. That includes 700 public housing apartments at Baychester and Murphy Houses in the Bronx being renovated under the federal Rental Assistance Demonstration program, which converts a development’s source of subsidy from public housing to Section 8.

But its most well-known development is Essex Crossing, a 1.7-million-square-foot megaproject on the Lower East Side that’s expected to be complete by 2022. So far, much of the first phase is complete: A 99-unit affordable senior rental building, a 211-unit, half-affordable rental building, and a 55-unit condominium building are all finished. Another mixed-income, 195-unit rental that includes a Regal Cinemas, an urban farm and a new Essex Street Market space is nearing the finish line, too. The 150,000-square-foot food and art market known as the Market Line is also expected to open its first phase this spring, with two more subterranean sections of the market to be built over the next few years.—R.B.R.

27. Paul Darrah

Director of Real Estate in New York City at Google

New

Meet Google’s Paul Darrah, the man who rushed in where Amazon feared to tread. In December 2018, Google, the California-based search, advertising and technology firm, announced an expansion of its New York City presence down to Hudson Square, heralding a “$1 billion” investment (for you math nerds, that’s 10 to the 91st power part of a Google). The Hudson Square campus includes leases at 315 Hudson Street and 345 Hudson Street, both buildings it plans to move into next year, and a letter of intent at St. John’s Terminal at 550 Washington, occupancy that is planned for 2022. That hub will be in addition to the firm’s Chelsea campus, where its purchase of the 1.2-million-square-foot Chelsea Market building for $2.4 billion in March 2018 was one of the top transactions of that year.

Overseeing all of these deals is Darrah, an architect-turned-facilities guy who cut his teeth at Bloomberg, leading the development of the media firm’s Park Avenue headquarters. At a Real Estate Board of New York members luncheon last month, he mentioned the “war for talent” that Google and other tech employers are engaged in. Though by old-school standards, we’re not talking about that many employees—Google plans to double its current New York City workforce of 7,000 over the next decade—apparently welcoming, primary-colored space is a major weapon in that skirmish.

Bells and whistles include multiple cafés that serve juice, gourmet food and even have Glatt Kosher offerings, and on-site wellness that includes gym facilities and massage therapists. However, community engagement may be Google’s secret weapon. Darrah said at the REBNY luncheon that “we’ve contributed in significant ways to the local community—that’s really how we’ve grown and matured.”

On that front, Google just debuted a tech training center offering free classes for small businesses in its Chelsea hub. Meanwhile, an expansion at RXR Realty and Youngwoo & Associates’ Pier 57 at West 15th Street in West Chelsea includes a large elevated park and plans for possible ferry service.—A.R.

28. Bruce White, John Santora and Bruce Mosler

CEO and Chairman; Vice Chairman and Tri-State Region President; Chairman of Global Brokerage, Cushman & Wakefield

Last Year's Rank: 33

“We’re in a great position to jump on 2019,” said John Santora. Cushman & Wakefield’s stock, the result of last summer’s initial public offering, has rebounded since its last December trough of $13.45 per share, and is now hovering around $18 per share, slightly above its IPO price of $17. The firm’s big presences (Brett White has been CEO since 2015, and Bruce Mosler, a legendary leasing broker and former CEO, has been with the firm for decades) are guiding a ship that in 2018 did such large deals as Pfizer (both selling the Midtown East headquarters and representing the tenant in leasing new space at Hudson Yards); selling the Chelsea Market building to Google on behalf of Jamestown for $2.4 billion and representing McDonald’s in its 7,000-square-foot retail lease at the Bow Tie Building at 1530 Broadway.

“We had dominance in capital markets, continued growth, continued strength in leasing, and repositioned our middle-market team with Kevin Smith [a veteran of TIAA],” Santora said.

“We continue to be involved in game-changing relationships,” noted Mosler, citing Brookfield Property Partners’ Manhattan West development—a now-burgeoning $4.5 billion development that runs from West 31st to West 33rd Streets, but one whose office leasing had been a tougher sell four years ago, when Mosler represented Brookfield in bringing law giant Skadden, Arps to the development.

Throw in a (hopefully) continued quiet-interest rate environment and continued strong employment, and what’s not to like?

Added Santora, “There was this concern, with Hudson Yards coming on board—will that leave big holes? Well, some tenants and occupiers have moved all out, but there’s activity right behind them.”—A.R.

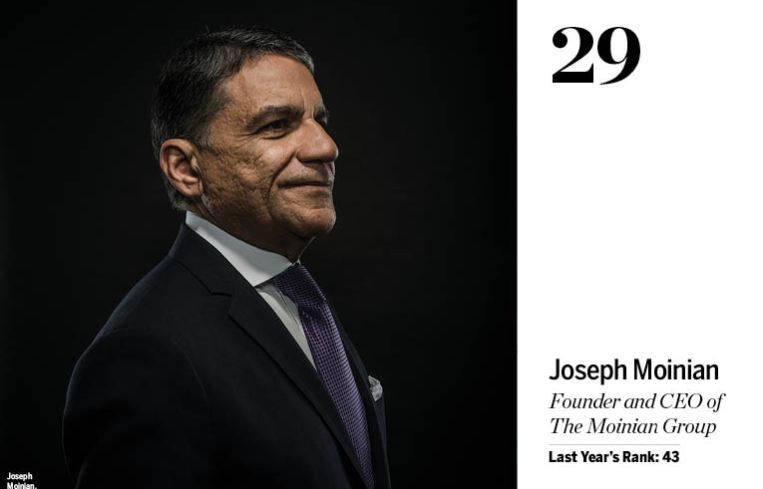

29. Joseph Moinian

Founder and CEO of the Moinian Group

Last Year's Rank: 43

For last year’s Power 100, Joseph Moinian described his 2017 as a “banner year,” and it’s hard to argue against a similar run in 2018.

Most notably, in July the firm brought in Boston Properties as a minority investor and managing partner in developing its planned 2-million-square-foot office tower, 3 Hudson Boulevard, the $2 billion “crown jewel” of Moinian’s portfolio, as he told GlobeSt following the deal’s close.

Last February, Moinian unveiled Oskar, a new 14-story, 118-unit luxury rental project at 572 11th Avenue on the Far West Side, just around the corner from the firm’s massive 60-story rental, Sky. Tenants in Oskar—which was named after Moinian executive Oskar Brecher, who died in 2016—will have exclusive access to Sky’s Life Time Athletic club. Leasing at Oskar launched in April 2018.

Later in the year, Moinian locked down $595 million from J.P. Morgan Chase and Deutsche Bank to fully acquire 3 Columbus Circle—the location of Moinian’s headquarters—paying $233 million for SL Green Realty Corp.’s roughly 49 percent stake in the asset; the deal closed in November. Earlier that month, it announced that it secured a $140 million, Freddie Mac-backed refinance from Berkadia Commercial Mortgage for Ocean at One West Street, its 31-story Lower Manhattan residential tower.

Elsewhere in the business, Moinian’s financing arm Moinian Capital Partners provided $125 million in debt to refinance one of Marx Development’s Hudson Yards hotels, the 29-story Courtyard by Marriott, at the corner of West 34th Street and 10th Avenue. The firm also participated in the $70 million Knotel Series B funding round in April 2018.—M.B.

30. Tommy Craig

Senior Managing Director at Hines

Last Year's Rank: 40

One of the neighborhoods that really had a moment in 2018 was Hudson Square.

“The combination of Google’s commitment” to more than 1 million square feet at St. John’s Terminal “and Disney’s commitment [to 4 Hudson Square] is really quite extraordinary given the scale of those two users,” said Tommy Craig. “It’s really a strong counterpoint to Hudson Yards.”

Hines has been riding that wave; those deals weren’t Hines’ deals, but the company leased more than 200,000 square feet to Google at 345 Hudson Street, part of Trinity Church and Norges Bank Real Estate’s Hudson Square Portfolio, for which Hines has been the operating partner since 2016.

Of course, Hines, which is based in Houston, has real estate concerns all over New York (and the world for that matter), and it isn’t by any means limited to Hudson Square.

“I think we’re off to a very strong start with a lot of active leasing,” Craig said. “We’ve got a 2 percent vacancy rate right now and…the majority of [our] major tenants want to expand or renew or extend.” (Its portfolio in New York is roughly 6 million square feet.)

Development-wise, Hines is one of the partners in SL Green Realty Corp.’s One Vanderbilt, which is now about 52 percent leased; it’s also partnering with Welltower on two senior living developments, Sunrise at East 56th Street and 2330 Broadway. It has also gotten the temporary certificate of occupancy on the first few floors of the MoMA Tower that it’s building at 53 West 53rd Street.

“It’s a large body of work we’ve completed in the cycle,” Craig said, “and what’s interesting to me is that New York—notwithstanding the Amazon situation—continues to stand out as a destination for both capital and talent in a global economy, [and] seems to continue to expand notwithstanding the lack of political normalcy. In a positive way.”—M.Gross

32. Christoph Kahl, Matt Bronfman and Michael Phillips

Chairman; CEO; President of Jamestown

Last Year's Rank: 22

Jamestown just suffered a major political setback in New York City, but its overall business is going quite well, according to the company’s president, Michael Phillips. The company wanted a rezoning to dramatically expand its 6-million-square-foot Industry City campus in Sunset Park, Brooklyn. However, the local city councilman, Carlos Menchaca, came out against the plan to add new construction to the World War I-era industrial complex. So did the local state senators and congressional representatives. Jamestown hopes to build up to 3.3 million square feet of hotels, retail, academic and light industrial space as part of the rezoning.

Despite the opposition, Phillips is optimistic.

“I wouldn’t say [the rezoning] is toast. Like many zoning initiatives, there’s a path that they need to follow to get all the stakeholders to buy-in. Industry City is following that path.”

Overall, Jamestown owns 11 million square feet of property in New York City and 24 million square feet nationwide. It sold $2.7 billion worth of assets last year: the Chelsea Market building traded for $2.4 billion, and 28 mixed-use buildings on Newbury Street in Boston changed hands for $300 million. The 36-year-old real estate investment outfit also acquired $483 million nationwide last year. In 2019, the firm plans to “work with Google on its plans for the overbuild and management of Chelsea Market,” said Phillips, referring to Google’s tentative plans to expand the 1.2-million-square-foot property using 300,000 square feet of development rights that came with it. Jamestown will continue to manage the market on Eighth Avenue and has kept rights to the brand, with plans to build Chelsea Market locations in Europe and other parts of the U.S.

The Atlanta- and Cologne, Germany-based firm also recently opened an office in Amsterdam to work on office and industrial repositioning projects throughout Europe.—R.B.R.

32. Josh Kuriloff

Executive Vice Chairman at Cushman & Wakefield

New

It’s unjust to face space limitations when talking about Josh Kuriloff’s year; in 2018 he was the No. 1 office broker for Cushman & Wakefield in the Americas. In office leasing, where he works both sides of the table, the super-broker did two noteworthy deals, either of which alone might have landed him in the Power 100. As a topper, he did them in different cities, with clients in different industries, of course.

In New York, he represented Pfizer in the firm’s taking 825,000 square feet in The Spiral, the Tishman Speyer building under construction at 66 Hudson Boulevard in Hudson Yards. Executives at the pharma giant, which was selling its headquarters in Midtown East, had expressed a desire to stay in the Grand Central Terminal corridor for ease of commute.

“We requested from them, respectfully,” said Kuriloff, “to show them Hudson Yards and Downtown, because that’s where new construction is.”

The master-planned community, with 1.5 million square feet of retail and a $2 billion subway stop, wowed Pfizer management, Kuriloff said. But the company had been an owner for 55 years and had to be eased into a multi-tenant environment.

The solution was “a building within a building,” with its own lobby and elevator bank.

If, in New York, Kuriloff had walked the client away from its target neighborhood, in Boston he did what few brokers would do: he walked the client away from its target building. “Verizon called me in,” he said. “They had a strategy that they wanted to consolidate their suburban sites into the city, to attract talent. And they had a target site in the Seaport district, which is a hot district.”

However, Kuriloff and John Boyle, a C&W vice chairman in Boston, had some concerns about the site.

“The elevation was just above sea level, and we had some concerns about flooding. The [target] building was an architectural masterpiece, but extremely expensive.”

Therefore—stepping away from a deal with a strong possibility of commission-generating closing—Kuriloff and his team identified a better, more inexpensive solution. They guided Verizon to The Hub on Causeway, a Delaware North and Boston Properties building being planned for the site of the former Boston Garden.

“It had a better location and better access to the university,” Kuriloff said, “and it was cheaper.”

The resultant lease of 440,000 square feet was “creative fun and a major pivot,” Kuriloff said. He praised the client and the developer for being collaborative.

“It will be one of the coolest workplaces anywhere in the country when it’s finished at the end of 2020.”—A.R.

33. David Simone

Chairman and CEO of Simon Property Group

Last Year's Rank: 37

When Grace Kelly appears in Rear Window, she’s bringing dinner from the restaurant 21 Club to a wheelchair-bound Jimmy Stewart. At this point in retail, running malls requires something of the same ingenuity: How do you connect the customer to the brand when the customer is increasingly unwilling or unable to hit the bricks?

For David Simon, who helms mall real estate investment trust Simon Property Group, the answer is “omnichannel,” a buzzword for supplying the customer with a seamless retail experience whether the customer is on his or her computer or in the store. Simon Property is taking its role as the mediator between brands and buyers quite seriously. Set to launch this spring is “Shop Premium Outlets,” an online platform that will offer special customer discounts to drive buyers into Simon’s 69 premium outlet malls.

The Indianapolis-based company has also embraced mixed-use as malls have widely faced climbing vacancies. At Northgate—a Seattle-based shopping center that opened in 1950, making it one of the first malls in the U.S.—old-school department store J.C. Penney has closed, with Macy’s set to follow, in keeping with the shrinking of traditional retailers playing out all over the country. But office space, hotel rooms and even a light-rail stop are coming, according to an article in the Puget Sound Business Journal.