Skip to content

Leases

Industrial

Office

Retail

All Leases

Deals of the Week

Finance

Acquisition

CMBS

Construction

Distress

Refinance

All Finance

Deals of the Week

Sales

Residential

Commercial

Mixed Use

Land

Hotels

Development Rights

All Sales

Deals of the Week

Design + Construction

Architecture

Construction

Infrastructure

Policy

Urban Planning

Neighborhoods

All Design + Construction

Technology

More

Analysis

Columnists

Features

Industry

IMPACT

Legal

Partner Insights

Players

Research

Tenant Talk

Transportation

Markets

Los Angeles

New York City

Manhattan

Brooklyn

Queens

Bronx

National

Washington DC

South Florida

Videos

Power Briefing

Leasing + Sales Q&A

Design + Construction Q&A

On-Demand Events

All Videos

Weekly Issue

Events

Power Series

Log In

Sign Up

My Account

Log Out

Account Details

Email Preferences

Member FAQs

Logout

Search

Leases

Industrial

Office

Retail

All

Deals of the Week

Finance

Acquisition

Construction

CMBS

Distress

Refinance

All

Deals of the Week

Sales

Residential

Commercial

Mixed Use

Land

Hotels

Development Rights

All

Deals of the Week

Design + Construction

Architecture

Construction

Infrastructure

Policy

Urban Planning

Neighborhoods

All

Technology

More

Features

Columnists

Analysis

Research

Partner Insights

Industry

Legal

Players

Transportation

All

Markets

Los Angeles

New York City

Manhattan

Brooklyn

Queens

Bronx

National

Washington DC

South Florida

Videos

Power Briefing

Leasing + Sales Q&A

Design + Construction Q&A

On-Demand Events

All Videos

Weekly Issue

Events

IMPACT

Advertise

Contact

Reprints

Newsletters

Power Finance

Power 100

Owners Magazine

Log In

Sign Up

My Account

Log Out

Account Details

Email Preferences

Member FAQs

Logout

© 2024 Observer Media ·

Terms

·

Privacy

Richard Persichetti

Analysis

New York City

Don’t Discount Law Firms in Manhattan Leasing!

By

Richard Persichetti

Premium

Trending Stories

Design + Construction

·

Construction

New York City

L+M Plans 328-Unit Affordable Housing Development at 1225 Gerard Avenue in the Bronx

Sales

·

Residential

New York City

Reshape Properties and Starman Holdings Purchase 210 West 10th for $19M

Players

National

Jim Dillavou Talks Lincoln Property Retail Expansion at ICSC

Legal

New York City

NY’s Top Court Rejects Challenge to Howard Hughes’ 250 Water Street Development

Analysis

New York City

Investment Sales: We’re Baaaaccck!

By

Richard Persichetti

Premium

Analysis

New York City

It’s Summer! Here’s the Hottest Markets and Submarkets

By

Richard Persichetti

Premium

Analysis

New York City

Availability Rates Dropped or Were Flat During 1Q 2018

By

Richard Persichetti

Premium

Analysis

New York City

NYC Sales Posting Highest Volume in Six Quarters

By

Richard Persichetti

Premium

Trending Stories

Design + Construction

·

Construction

New York City

L+M Plans 328-Unit Affordable Housing Development at 1225 Gerard Avenue in the Bronx

Sales

·

Residential

New York City

Reshape Properties and Starman Holdings Purchase 210 West 10th for $19M

Players

National

Jim Dillavou Talks Lincoln Property Retail Expansion at ICSC

Legal

New York City

NY’s Top Court Rejects Challenge to Howard Hughes’ 250 Water Street Development

Analysis

New York City

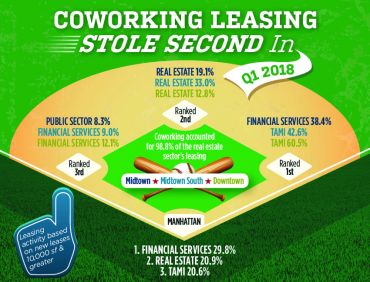

Coworking Steals the Show in the First Quarter

By

Richard Persichetti

Premium

Analysis

New York City

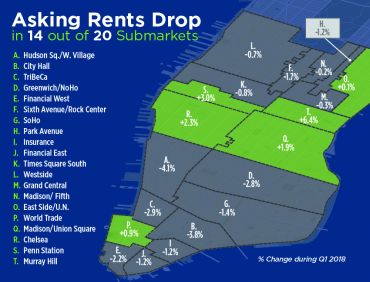

Despite Big Drop in Vacancy, Asking Rents Down

By

Richard Persichetti

Premium

Analysis

New York City

Times Square South Saw Six 100K+ Leases

By

Richard Persichetti

Premium

Analysis

New York City

The Area Around Penn Station Saw a Massive Drop in Vacancy

By

Richard Persichetti

Premium

Leases

·

Office

New York City

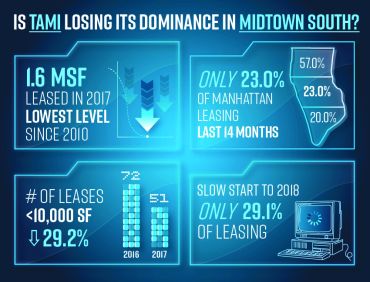

TAMI Activity Slows in Midtown South

By

Richard Persichetti

Premium

Analysis

New York City

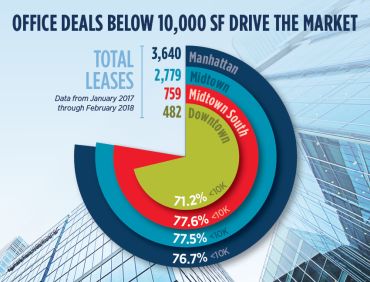

Small Is Beautiful: 77.6 Percent of Midtown South Deals Were Mini

By

Richard Persichetti

Premium

Analysis

New York City

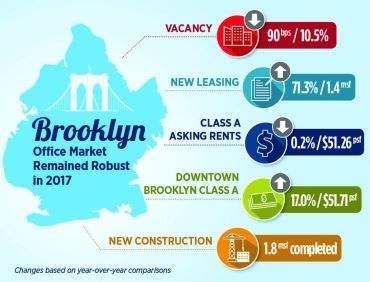

Brooklyn’s Historically High Leasing Year

By

Richard Persichetti

Premium

Analysis

New York City

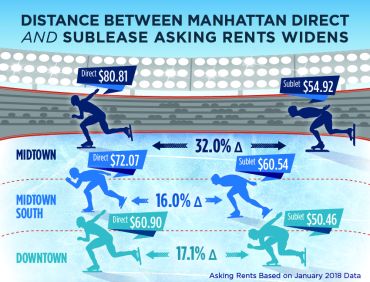

Manhattan’s Sublease Pricing Gap Widens

By

Richard Persichetti

Premium

Analysis

New York City

There Were Big Gains in the Jobs Sector; Here’s Where

By

Richard Persichetti

Premium

Analysis

New York City

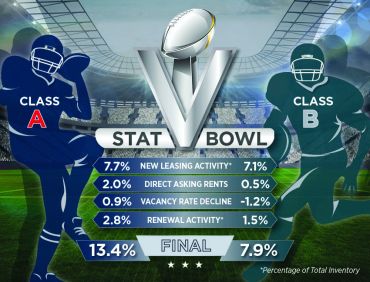

Stat of the Week: 13.4 to 7.9

By

Richard Persichetti

Premium

Analysis

New York City

Stat of the Week: 6 Out of 6

By

Richard Persichetti

Premium

Analysis

New York City

Stat of the Week: 410 BPS

By

Richard Persichetti

Premium

More