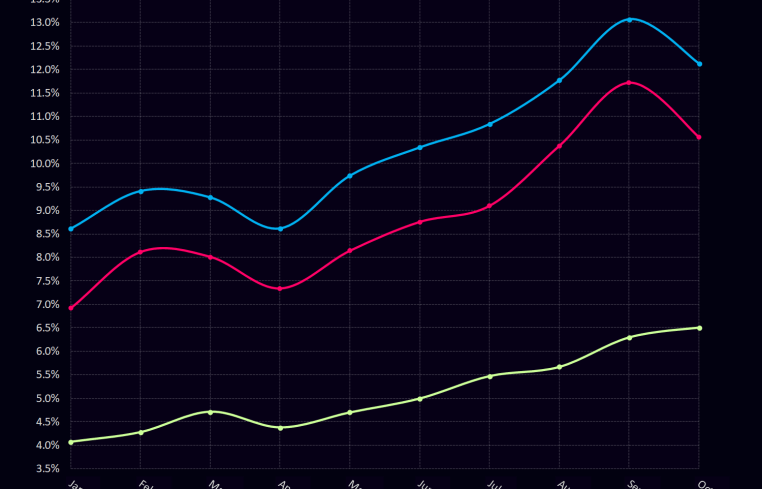

CRE CLO Distress Rate Inches Down to 12.1%

The CRED iQ team focused on commercial real estate collateralized loan obligations (CRE CLOs) to explore how this marketplace has evolved since our previous report in September.

We found that the CRED iQ distress rate fell 97 basis points (falling to 12.1 percent from 13.07 percent) on the heels of adding 277 basis points in our October print. In comparison to the CMBS distress rate of 9.6 percent, the CRE CLO sector remains higher by 250 basis points.

The CRED iQ distress rate includes any loan reported 30 days delinquent or worse, past their maturity, specially serviced, or a combination of these. We also examined the most recent property-level net operating income figures and compared them to underwritten expectations.

Given the rapid surge in interest rates, these floating-rate loans have shown significant declines in debt service coverage ratios (DSCR). Forty-seven percent of the properties within the distressed CRE CLO sector have reported a lower DSCR net cash flow compared to their underwritten DSCR. These numbers are based on the underwritten “as is” DSCRs and net operating income.

CRED iQ’s analysis uncovers that 67.1 percent of all distressed CRE CLOs are operating below a 1.0 DSCR, up from 62.3 percent last month. NOI is a key variable in calculating a loan’s DSCR, which determines the strength and creditworthiness of a given loan.

The office sector continues its leadership in distress across all property types, logging a distress rate of 18.4 percent, remaining mostly flat to last month’s print. While still high, the office segment is off its 2024 distress peak of 21.3 percent in February.

Multifamily distress increased 140 basis points to 15. percent in October, compared to 13.7 percent last month. Multifamily remains firmly entrenched as the second most distressed segment.

Retail saw its distress rate decrease significantly from 11.1 percent to 7.2 percent, dropping two slots to the fourth most distressed CRE CLO property type. The hotel segment also saw a decrease in their distress rate to 7.7 percent and landing just above retail as the third most distressed CRE CLO property type.

Industrial saw a slight uptick to 1.7 percent, representing a 60 basis point increase from last month. Self-storage continued to operate without distress in October.

Looking across payment status, 31.4 percent of loans are performing matured, with another 32.4 percent nonperforming matured, meaning 63.8 percent of the CRE CLO loans in our study are past their maturity dates — down slightly from 64.3 percent in the September report.

Analysis, scope and methodology

CRED iQ consolidated all of the loan-level performance data for every outstanding CRE CLO loan to measure the underlying risks associated with these transitional assets. Our team examined $70.8 billion in active CRE CLO loans. Many of these loans were originated in 2021 at a time when cap rates and interest rates were low and valuations high; the loans are starting to run into maturity issues given the spike in rates.

Some of the largest issuers of CRE CLO debt over the past five years include MF1, Arbor, LoanCore, Benefit Street Partners, Bridge Investment Group, FS Rialto and TPG.The vast majority of the $79.1 billion in CRE CLO loans are structured with floating rates with three-year loan terms equipped with loan extension options if certain financial hurdles are met.

Mike Haas is the founder and CEO of CRED iQ.