CRE CLO Distress Rates Drop, Issuance Soars

The commercial real estate collateralized loan obligation (CRE CLO) market offers lenders flexibility and investors exposure to diversified real estate debt. As interest rates elevated, the sector experienced notable shifts in loan performance. But are those trends now reversing?

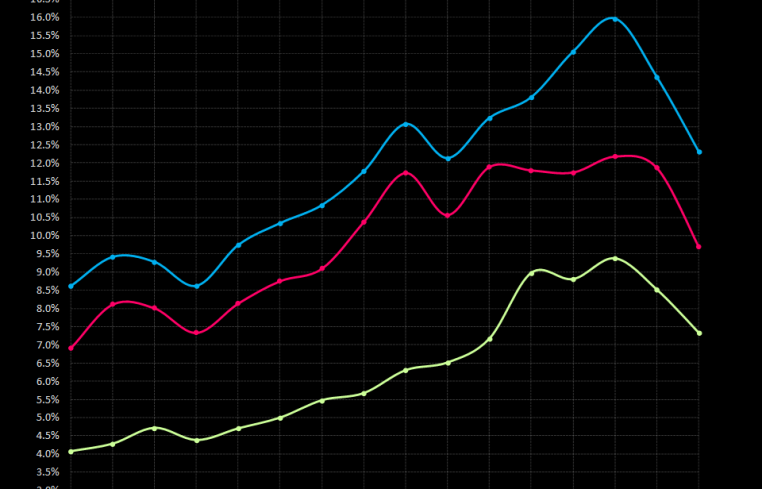

CRED iQ’s latest report on the April results reveal some encouraging trends. Our overall distress rate notched a 410-basis point (BP) decline, the largest such favorable move in over a year. The CRE CLO distress rate now stands at 10.3 percent.

Similarly, the underlying metrics saw meaningful declines as well. Our delinquency rate dropped 220 basis points to 9.7 percent and special servicing shaved 110 BPs, landing at 7.4 percent.

Total year-to-date CRE CLO issuance totals $11.4 billion, which includes Invesco’s first CLO deal that totaled $1.2 billion. Also notable this year was TPG’s $1.1 billion managed CRE CLO deal, of which $962 million was rated investment grade.

As a comparison, during the first four months in 2024, CRE CLO volume only totaled $2.2 billion, meaning CRE CLO issuance velocities have increased 400 percent compared to last year.

While these improvements are encouraging, the broader picture reveals ongoing challenges. Some, 63.1 percent of CRE CLO loans have surpassed their maturity date (down from 69.5 percent last month). Also, 36.6 percent are classified as “performing matured, down from 37.3 percent. This suggests that many borrowers are exercising extension options or negotiating month-to-month arrangements to avoid default.

The percentage of loans current in April was 16.8 percent, up from 15 percent in March.

Non-performing matured loans represent 36.6 percent of CRE CLO loans , up from 32.2 percent the previous month.

Delinquent loans (pre-maturity) accounted for 15.7 percent of CRE CLO loans, a jump up from 13.1 percent the prior month.

These figures reflect a market grappling with the aftermath of loans originated in 2021, when cap rates were compressed, valuations were elevated, and interest rates were historically low. Many of these loans, structured with floating rates and three-year terms, are now hitting maturity walls in a dramatically different economic environment.

A real-world example illustrates the pressures facing CRE CLO borrowers was the $46.3 million Haven at Bellaire loan, backed by a 384-unit multifamily property in the Houston market. Set to mature in April, the loan included two one-year extension options at origination. The loan was added to the servicer’s watchlist in November 2024 due to pending loan maturity and transitioned to performing mature status in April.

Mike Haas is the founder and CEO of CRED iQ.