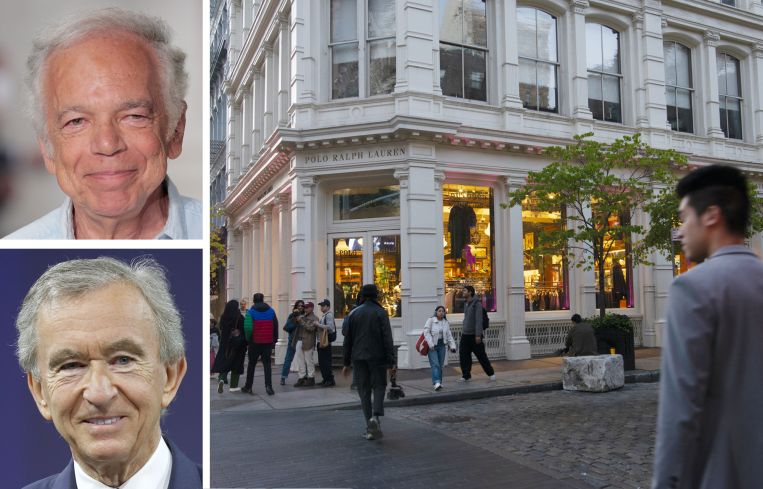

Ralph Lauren in Bidding War With LVMH for SoHo Storefront

By Lois Weiss April 4, 2025 11:01 am

reprints

A prominent SoHo corner spot at Prince and Greene streets has been at the center of a bidding war by two luxury brands, but it looks like the longtime occupant, Ralph Lauren, will pay up to keep the space, Commercial Observer has learned.

While the ground-floor storefront 109 Prince Street has been occupied by the retailer since 2010, its lease is coming due. French retail giant LVMH has been battling for the space, which LVHM wants for Tiffany & Co., now located at nearby 97 Greene Street.

Sources told CO Ralph Lauren will most likely purchase the spot, but it could also turn into a high-priced lease instead.

Most retail deals are currently trading at a 6.5 to 8 percent cap rate, according to broker Adelaide Polsinelli of Compass, who marketed the space a decade ago for $54 million with no takers. While unaware of but not involved in the current transaction, she said Ralph Lauren would now command a premium over that range, putting it at a 5 to 5.5 percent cap rate.

The Real Estate Board of New York‘s fall report found average retail asking rents along the Broadway corridor in SoHo to be $490 per square foot. Any new starting rent for Ralph Lauren would likely be higher.

LVMH has been trying to find a new home for Tiffany for some time, but keeps losing out.

Over the last year, the company has tried to lease the former Nespresso store at 92 Prince Street, which was instead leased to Ferrari, as well as the nearby Apple store at 103 Prince Street. That 30,000-square-foot former post office has been occupied by Apple since 2001 and underwent a $30 million expansion and renovation in 2011 when it was purchased by Imperium Capital.

With the aggressive LVMH nipping at the bricks, to maintain its space, one real estate source said, “Apple was forced to renew at a rent they didn’t love.”

Now it looks like LVMH has lost out on another Prince Street deal and pushed another retailer to pony up.

The primary owner of 109 Prince is the Swiss investor and art financier Jean-Pierre Lehmann, who bought the 20,000-square-foot historic cast-iron building in 1991 for $3 million. He completely renovated the French Renaissance-style edifice, first home to silk dealers and later to chemical suppliers, designed by Jarvis Morgan Slade and now part of the SoHo-Cast Iron Historic District.

In 1997, Lehmann sponsored the building as a live-work artist condominium through his company Prince Street Realty, with retail on the ground floor, second floor and lower level, plus three upper-floor residences.

In May 2010, records show Ralph Lauren signed a lease for the two retail lots, which had been a Replay store with a café in the lower level. The lease ends in 2026.

The ground-floor lot has 3,258 square feet with a retail-friendly, 16-foot-high ceiling and a lower-level cellar spanning 3,386 square feet. The second-story retail condo has 3,265 square feet, and restaurateur Jean-Georges Vongerichten leased it for storage. It could not be determined if he still leases that space.

With those leases in hand, however, Lehman reconstituted the ownership entity of the two lots and obtained a mortgage of $18 million.

After trying to sell the leased retail for $54 million through Polsinelli, enough interest was generated to up the mortgage in 2014 to $35 million with J.P. Morgan Chase, which pooled it into a commercial mortgage-backed securities loan.

In 2016, as Ralph Lauren was closing stores around the country, CO reported that loan could be at risk in 2026 if the retailer did not renew since the store occupied 74.2 percent of the space, with 25.8 percent being occupied by others — presumably Vongerichten.

But now the loan appears to be paid off.

A Securities and Exchange Commission report from February 2025 said the balance on the one New York retail loan was $29.6 million and had an interest rate of 4.65 percent. Scheduled to mature in January 2026, the loan was anticipated to be repaid in June 2024. While no loan satisfaction has been filed, the report also stated there was an “unscheduled principal” prepayment for a partial liquidation of $156,917, and that the loan was paid through March 1.

The upper floors are all residential condominiums. The third floor of the building has been owned since December 1998 by a Fortress Investment Group executive who did not respond to requests for comment. He paid $1.375 million to late art gallery owner Ileana Sonnabend, who had paid $775,000 just a year earlier. She also paid $775,000 for the fourth floor, which she sold back to Lehmann’s entity in mid-1998 for $1.589 million. His entity also still owns the fifth floor that has exclusive use of the roof.

Sources said Ralph Lauren is likely negotiating this deal in-house but its spokesperson did not return requests for comment. Lehmann’s attorney and an LVMH spokesperson also did not return requests for comment.

Naturally, this deal may still be undone.

If inked as a sale, however, it would continue what is now a long trend of retailers buying New York City real estate.

Prominent sales to retailers include Prada buying 720 and 724 Fifth Avenue, and a space in 730 Fifth Avenue, from Jeff Sutton for $835 million; Kering paying Sutton $963 million for 100,000 square feet at the base of 717 Fifth Avenue, which it is expected to renovate for Gucci; and James Dyson‘s Weybourne Group picking up 155 Mercer Street for $60 million as well as 770 Madison Avenue from Sutton and the Reuben Brothers for $135 million, where it is expected they will eventually locate Dyson stores.

Plus, as CO first reported, Chanel is now negotiating to buy 60,000 square feet of retail in the base of Gary Barnett’s upcoming 655 Madison Avenue luxury residential tower for around $450 million. Barnett has already sold 70,000 square feet at 570 Fifth Avenue to Ikea’s parent for about $400 million.