Apartment Loan Delinquencies Surge in Q4 2024

This week, the CRED iQ research team zoomed in on the latest trends shaking up the apartment sector, building on the community bank data from our 2025 almanac. The numbers tell a story of rising delinquencies, slowing growth and some eye-popping loan loss figures for 2024.

Multifamily loan delinquencies at community banks jumped 39 percent in the fourth quarter of 2024 compared to the third quarter, ballooning by $2.38 billion in newly delinquent loans. That brings the total delinquent balance in the multifamily sector with regional banks to a hefty $8.49 billion by year’s end. For context, this figure was just $6.11 billion in Q3 of 2024 and a modest $1.98 billion back in Q2 of 2023. That’s right — delinquencies have been climbing steadily since mid-2023, but 2024 turned up the heat with bigger quarter-

over-quarter spikes.

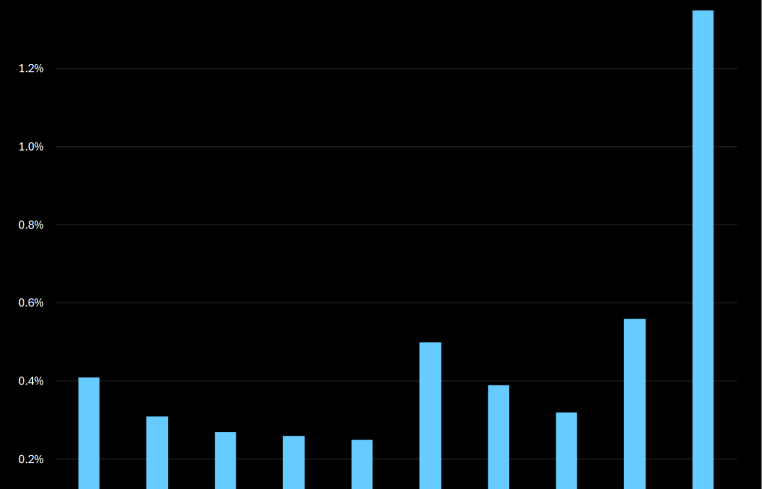

Breaking it down, 2024 started slow with a $234.8 million uptick in Q1 (compared to Q4 2023). Then things accelerated with Q2 adding $1.9 billion, Q3 tacking on $545.6 million, and then Q4 seeing a massive $2.4 billion increase. By the time the calendar flipped to 2025, the delinquency rate for multifamily loans hit 1.35 percent — a sharp rise from 0.56 percent a year earlier. The Q1 2025 data isn’t out yet, but the trend lines suggest this percentage isn’t slowing down anytime soon.

Over the past decade, multifamily loan balances held by community banks have swelled at a solid 7.9 percent average annual growth rate, from $297.4 billion in 2014 to $628.9 billion in 2024. That’s a lot of apartments! But the twist is that growth has hit the brakes since 2023, dropping to just 2.2 percent that year and ticking up slightly to 2.8 percent in 2024. So, while the total loan pie keeps expanding, it’s growing at a much slower pace than before. Meanwhile, those delinquency cracks are widening.

If rising delinquencies weren’t enough, realized loan losses are adding salt to the wound. In 2023, community banks took a $305.8 million hit, a jaw-dropping 411 percent leap over 2022. Fast forward to 2024, and losses more than doubled to $691.8 million, up 126 percent from the year prior. That’s not just a blip — it’s a signal that the multifamily sector is feeling some serious pressure.

So, what’s driving this? We dug into FDIC-insured multifamily loan data to understand how community banks — key players in this ecosystem — are exposed. The uptick in delinquencies and losses points to broader challenges: rising interest rates, softening rents, or maybe even overleveraged borrowers. Whatever the culprits, the numbers don’t lie. This is a trend worth watching.

Mike Haas is the founder and CEO of CRED iQ.