Blackstone Looks to Foreclose on Art Deco Landmark the McGraw-Hill Building

By Abigail Nehring July 18, 2024 2:29 pm

reprints

The planned residential conversion of an Art Deco landmark in Hell’s Kitchen may have to hit pause until the building’s finances get straightened out.

Lenders Blackstone and Rialto Capital initiated a foreclosure against Deco Towers Associates after it defaulted on a $140 million floating-rate loan package tied to the McGraw-Hill Building at 330 West 42nd Street, according to a pair of complaints filed on Tuesday and Wednesday in Manhattan Supreme Court.

“We continue to engage with borrowers to find the best resolutions possible,” a spokesperson for Blackstone said in a statement to Commercial Observer.

The loan package’s components — a $65 million mortgage modification, a $50 million building mortgage modification and a $25 million building loan — matured a few months apart in October and May, and Deco was hit with notices of default shortly after, court records show.

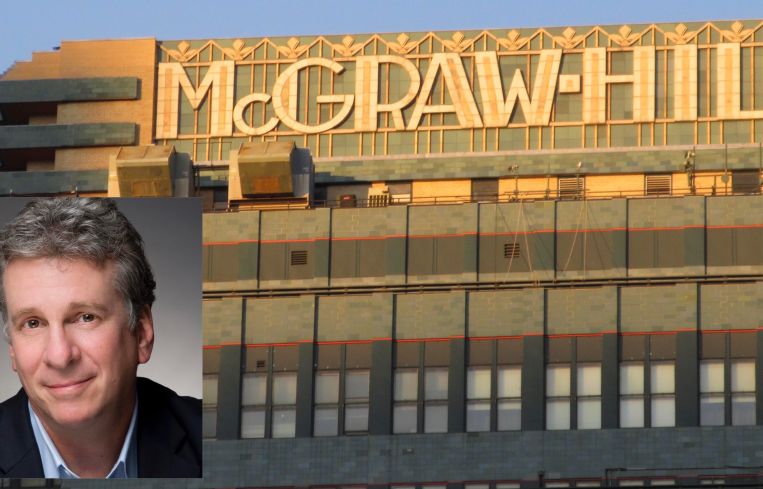

Alex Schwartz, of ASI Management, guaranteed the bulk of the loan package and was listed as the manager of Deco Towers, according to property records.

The 33-story office building was once home to the McGraw Hill publishing company but has sat largely vacant since its former longtime tenant, Service Employees International Union, departed in 2020.

Asset manager Resolution Real Estate stepped in that year to embark on a $120 million gut renovation and repositioning of the property, terminating the remaining leases to clear out the building, as CO previously reported. Resolution hired MdeAS Architects to draw up plans to convert the top half of the building to apartments.

The project, which included removing the historic “McGraw Hill” sign fixed atop the tower in the 1930s, faced close scrutiny from the city’s Landmarks Preservation Commission, but finally appeared to get underway last year, CO reported.

Signature Bank provided the loans in 2019 and began looking to sell the building’s debt in 2023, but never got the chance. Instead, Blackstone and Rialto took it over later that year when they acquired a stake in Signature’s former $16.8 billion commercial real estate loan portfolio, according to property records.

Despite the issues with Signature, Gerard Nocera, managing partner at Resolution, told CO in 2023 that everything was running smoothly at the project.

“We’ve been current on that loan, [we will] stay current on that loan,” Nocera previously said. “It’s at a very good rate in today’s world, so we’re happy with that and we plan to extend it.”

But now things have changed, and, in addition to facing foreclosure, the developer was hit with hefty fines in 2023 for failing to remedy violations issued by the New York City Department of Buildings, city records show. It’s also had a partial stop work order on the property since 2020.

Nocera and spokespeople for Rialto and Deco Towers did not immediately respond to requests for comment. Schwartz could not immediately be reached for comment.

Update: This story has been updated to include a statement from Blackstone.

Abigail Nehring can be reached at anehring@commercialobserver.com.