The 50 Most Important Figures of Commercial Real Estate Finance

By The Editors April 4, 2018 11:30 am

reprints

With even the industry’s top lenders battling it out for every deal—bank against debt fund, CMBS shop against life insurer—never has there been a more competitive year in American commercial real estate finance than 2017

“We were doing head-to-head combat every day,” as UBS’ Chris LaBianca, this year’s No. 31 honoree, put it. That made it trickier than ever before for our survey of the battlefield to rank the most exemplary victors—especially given our desire to take a broader nationwide perspective this time around.

This fresh outlook widened the field like never before. As a result, a painstaking dive into the companies behind the big-number deals—as well as due consideration to fearsome feats of entrepreneurship among some of the field’s newest entrants—went into crowning our champions of real estate deal-making. Volumes were up nearly across the board, creating a dog-eat-dog environment where firms had to sprint ahead merely to stay in place among our ranks.

In that context, the performance of some of our dynamic newbies rings all the more impressive. Lotus Capital, Faisal Ashraf’s year-old startup, expanded its debt-advisory reach to three continents and launched a new loan sale distribution platform, landing with a splash for its first year on the list in the No. 41 spot.

KKR’s debt business is off to the races, already going blow for blow with stalwarts like Blackstone and TPG. And CBRE’s Tom Traynor and James Millon turned in a stellar debut performance we couldn’t ignore, arranging $5.1 billion in debt in just their first eight months on the job.

In the world of securitized mortgages, the era of risk retention opened more space between the haves and the have-nots, pushing the most aggressive CMBS shops into some of our top spots. Fueled by eye-popping single-asset deals, those firms claimed 2017’s most exciting trophy asset financings all to themselves.

And the formidable Freddie Mac and Fannie Mae each surpassed their own high-water marks, producing record volumes that affirmed their places at the forefront of America’s multifamily market. Their wake propelled some of our honorees’ impressive leaps this year, like Walker & Dunlop’s jump to the No. 19 slot, vaulting 30 places from last year.

Finally, we made sure to tip our hats to the market’s envelope-pushers, outfits like Bank of the Ozarks (No. 17), who has charged boldly but astutely into the forbidding territory of construction lending, and Starwood (No.4) whose multicylinder approach continues to impress.

It’s that brand of dynamism—shared in different ways by all our honorees—that writes the stories that fill our pages all year long.

1. Doug Mazer and Kara McShane

Head of Real Estate Capital Markets; Head of Commercial Real Estate Capital Markets and Finance at Wells Fargo

Last Year’s Rank: 11

Wells Fargo’s Doug Mazer and Kara McShane battled their way to the top of our most competitive list in recent memory on the sheer strength of the eye-watering numbers that tell the story of their record-setting 2017.

Ninety-six transactions that added up to $71 billion—a 23 percent increase over 2016. Lead or co-lead lender on 71 transactions totaling $52.7 billion—good for a 71 percent yearly increase. The top bookrunner in the ascendant market for collateralized loan obligations. First-ranking issuer of Freddie Mac commercial mortgage-backed securities for the fourth straight year by volume, and the sixth straight year by deal count. Upsizings and modifications worth another $13 billion. All of which rolled in to support revenue growth nearly 25 percent higher than last year’s rake.

“We were hitting on all cylinders,” McShane said, remembering that she’d never expected a year of this magnitude as the calendar turned. “I certainly didn’t anticipate the volume we achieved, the growth that we experienced in our securitizations. If you asked me to predict it, I would not have predicted that.”

Mazer, whose team saw remarkable 88 percent year-over-year growth in commercial mortgage-backed securities, tips his hat to a brisk trade in interest-rate-protected loans destined for securitization that supported a roaring trade for the San Francisco-based international bank. “Clearly the big needle-mover was in the CMBS floating-rate space,” Mazer said. “You have to start there. Conduit issuance and fixed-rate issuance were pretty flat.”

On his team’s way to snagging the top spot among CMBS lenders by loan count for the sixth straight year, a handful of bicoastal landmark deals propelled the effort, including a $500 million loan on Vornado Realty Trust’s 330 Madison Avenue, a $300 million loan on Macerich’s Santa Monica Place in the Los Angeles area, and a co-originated $2.3 billion financing on the General Motors Building in Midtown.

Granted, not all news was good news for Wells Fargo last year. Fallout from the bank’s account-fraud scandal continued to haunt the institution’s reputation among consumer banking clients, and this February, a regulatory order from the Federal Reserve barred the bank from any overall growth until further notice.

But in a missive to investors, the bank opined that by curtailing its activities in areas like short-term trading and bank deposits, customer-facing areas like commercial real estate shouldn’t notice any effects.

That flexibility could give McShane and Mazer’s group the runway it needs to go all in on collateralized loans, a sector that rocketed up significantly last year.

“I think you’ll see a really active CLO pipeline,” McShane said. “Our goals are to continue to grow our business, and from where I sit, it’s shaping up.”—Matt Grossman

2. Michael Nash, Stephen Plavin, Jonathan Pollack and Tim Johnson

Co-Founder and Chairman of Blackstone Real Estate Debt Strategies; CEO of Blackstone Mortgage Trust; Global Head of Blackstone Real Estate Debt Strategies; Senior Managing Director at Blackstone Real Estate Debt Strategies

Last Year’s Rank: 4

“2017 was a busier year for us,” said Jonathan Pollack, the global head of Blackstone Real Estate Debt Strategies. “The advantage we have as a platform is that we have scale of capital, we have $4-plus billion private equity fund and we also have a $3.5 billion market cap REIT that has $11 billion of balance sheet assets. At that kind of scale we can look at pretty much any deal that comes to market.”

But if you have a big boat, why fish for minnows when you can catch some marlins.

“We tend to try to focus on larger deals because there's less competition at that scale, more than anything that's what drove how busy we were last year,” Pollack said.

Across BXMT and BREDS the private equity giant lent $9.1 billion, a significant increase from $6.7 billion in 2016l. BXMT’s $4.8 billion total was a 37 percent increase on 2016.

“It was not only the size and scale of deals, but we were also relatively diverse from a geography standpoint,” Tim Johnson, a senior managing director at Blackstone Real Estate Debt Strategies said. “We did deals inside the U.S., up and down the Eastern seaboard, we did a lot in Hawaii and also some big transactions on the West Coast.”

Highlights for the dynamo team include a $900 million loan on a Northern Virginia office portfolio. Blackstone teamed up with Goldman Sachs to securitize the $500 million senior portion of the loan in the Rosslyn Portfolio Trust 2017-TRUST commercial mortgage-backed securities transaction. The deal is collateralized by three Class-A office buildings and four class-B office buildings in the Rosslyn district of Arlington, Va.

“The themes for us were accessing capital markets and doing larger scale transactions,” Pollack said. “After being in business for eight years we have many repeat clients, and Tim and the team do an amazing job.”—Cathy Cunningham

3. Al Brooks

Head of J.P. Morgan Chase Commercial Real Estate

New

Previous incarnations of Commercial Observer’s Power 50 list have included J.P. Morgan Chase’s Chad Tredway and Greg Reimers—a pair of real estate finance power players who lead commercial lending and real estate banking on the East Coast. But taking a broader national view this year (and to coincide with the launch of our weekly newsletter covering real estate in Los Angeles), we thought it was high time to recognize Southern California-based Al Brooks, the firm’s top executive for commercial real estate from coast to coast.

Given that he’s responsible for a $100 billion portfolio and annual originations that consistently track double-digits billions, the industry veteran has a rightful place in our top 10. His group was responsible for about $28 billion in commercial real estate originations last year with a total of $102 billion in outstanding loans—a figure that climbed 9 percent from 2016.

Brooks explained that 2017 was a year that exemplified that no loan was too large—or small—for his team to tackle.

“We’re most proud of [the fact that] we bank everything from an individual investor all the way up to the largest real estate companies in the country,” Brooks said, adding that a renewed focus on technology infrastructure was a personal theme for the year. “We’ve been fully committed to being as digital as possible, and we want to do that more. It’s driven costs down, and we can pass that on to our clients.”

Of course, that just goes toward supporting the bread-and-butter work for J.P. Morgan: executing on behemoth deals. Highlight ledger entries last year included the financings of Pioneer Natural Resources’ new 1.1-million-square-foot headquarters in Irving, Texas; Trammel Crow’s construction of Amazon distribution facilities in Denver, Portland, Ore., and Troutdale, Ore.; and funding for real estate mogul Jay Paul’s development of a pair of office towers in Sunnyvale, Calif., totaling 701,000 square feet.

That geographic diversity is nothing new for the global bank.

“From our perspective, we follow our clients,” Brooks said. “As their business needs evolve, so do our solutions and services.”

And although originations dipped a bit last year from 2016 levels, Brooks reported that things are back on track thus far in 2018. “It’s a good year,” he reported. “Our pipelines are up a bit from where they were. But it’s still a highly competitive environment.”—M.G.

4. Jeff DiModica and Dennis Schuh

President; Chief Originations Officer at Starwood Property Trust

Last Year's Rank: 14

Starwood Property Trust’s multicylinder approach is, well, firing on all cylinders.

“We’re transforming the way people should be thinking about this business,” Jeff DiModica said. “We’re building a better mousetrap, and that’s the only way to compete.”

Starwood’s debt originations increased to $7.5 billion last year, up from $6.4 billion in 2016.

But, pushing capital out the door isn’t Starwood’s primary goal. It’s playing the long game, carefully selecting transactions and focusing on its credit profile—a game it evidently plays pretty artfully, given that it hasn’t taken a loss in nine years.

“We do about 4 percent of the loans we spend time on, and only by saying no to 96 do we know that we’re getting four we really like,” DiModica said. “Some [lenders] may lower their credit thresholds in order to get volume up. We’d rather sit on cash if we don’t see great opportunities.”

Some of the opportunities it did like include a $250 million redevelopment loan for 700 K Street in Washington, D.C., and a $280 million ground-up construction loan to Hudson Companies for 280 Cadman Plaza in Brooklyn Heights (Starwood provided $200 million and Related Companies put in $80 million).

Construction loans made up one-third of Starwood’s debt activity in 2017, with the lender finding opportunities with solid sponsors in good markets, Dennis Schuh said. Further diversifying its book, the lender also widened its lens to make loans below the $100 million mark.

One key way that Starwood differentiated itself from the herd last year was in its issuance of unsecured bonds ($1.7 billion over the past 15 months). Its bond issuance in January has the tightest spread since the financial crisis and the second-tightest spread in the history of the high-yield market. “This gives us great flexibility to do things that other firms can’t,” DiModica said. “There are no assets or product types that we can’t finance.”

DiModica added, “The right side of our balance sheet is what really differentiates us and why we’ve been able to increase our lending today. It’s a financing advantage on a global scale.”

“If you look at what we do across our large-loan lending business, our fixed-rate conduit lending business, our investor and servicing segment business where we’re investing in CMBS, what we’re doing in residential non-Qualified Mortgage loans, we have a very dynamic real estate investment vehicle,” Schuh said. “There’s nobody who puts that all under one roof the way that we do.”—C.C.

5. Brian Baker

Global Head of Commercial Mortgages at J.P. Morgan Securities

Last Year's Rank: 9

“J.P. Morgan continued to grow as a firm and expand its real estate activities in 2017, transacting with a diverse group of clients,” said Brian Baker, whose team originated a whopping $18 billion in loans last year, a $2 billion increase from the year prior.

“The business here is very broad,” he added. “We’ll do the smaller fixed-rate loans that we usually exit in the CMBS market through securitization, but run the gamut through to the larger, more complicated loans—for example, development loans. We have the balance sheet capability and the talent to work through very complex situations.”

Baker runs a multifaceted business. Although his group issued $12 billion in CMBS across 48 deals—and was the No. 2 issuer last year—it also lends in whole loan form, meeting clients’ varying needs along the way.

Notable transactions the lender participated in include a $1.67 billion financing of American Dream, a 2.8-million-square-foot experiential mall and entertainment development in Meadowlands, N.J.; the $500 million financing of the old main post office in Chicago, a 2.4-million-square-foot office renovation; a $1.074 billion financing of the Stonemont office portfolio—a portfolio of 95 office, industrial and retail properties totaling 6.8 million square feet across 20 states—and a $650 million financing of 1568 Broadway, a 468-key hotel slated for redevelopment to a mixed-use property in Midtown.

Another much-talked-about deal was the bank’s $900 million construction loan for Extell Development Company’s 1.2-million-square-foot Central Park Tower on West 57th Street. “It falls into the ‘big and complicated’ category,” Baker said. “It’s a super tower, and we’re working with a client who is an expert in the space. The complexity of a deal like this one is intellectually challenging. We were able to show the client a solution, and the property required a lender who could work through the complexity of the deal.”

Of the heightened deal competition in the market, Baker said, “We’re happy to compete and have plenty of advantages that make us a formidable competitor.”—C.C.

6. James Flaum

Global Head of Commercial Real Estate Lending at Morgan Stanley

Last Year's Rank: 13

Last year may have been a high-water mark for competition in commercial real estate lending, but for big banks like Morgan Stanley, a spot at the top of the food chain helped them stay decidedly above the fray.

“Our business is less impacted by private equity lenders and [the deals] they tend to do,” James Flaum said. “We don’t run into them as much.”

That measure of insulation from middle-markets trench warfare helped Morgan Stanley on its way to a healthy bump in origination volumes last year as its total loans in the United States rose by about 14 percent to $16 billion from $14 billion in 2016. Its securitization business surged as well by 60 percent to $9 billion in CMBS activity from $5.6 billion the year prior.

Part of that success flowed from Morgan Stanley’s readiness to do business in a red-hot loan product type that had been dormant in recent years.

“I think the biggest theme for 2017 was the comeback in the floating-rate securitization market,” Flaum said. “Most of the single-asset, single-borrower [deals] were really floating rate. This was driven by investor demand, and the expectation that interest rates are going up.”

One single-asset, single-borrower deal—although a loan that closed with a fixed rate—was the source of the biggest headline of the year for Flaum’s team: a $2.3 billion refinance of the GM Building in Midtown with a 10-year term at 3.43 percent. Other eye-catching transactions for Morgan Stanley’s CRE team in 2017 included a $2.6 billion CMBS financing on a pair of Blackstone hotel portfolios as well as the bank’s $850 million refinancing of Lower Manhattan’s One Liberty Plaza in August.

As the first quarter of 2018 winds down, Flaum said he expects continued strength for the year with the caveat that the industry could always be roiled by a monetary policy surprise.

“Will growth in net operating income keep up with any cap rate expansion that may occur because of higher interest rates?” Flaum said he is asking himself. “If growth keeps up with cap rate expansion, prices will stay flat. That’s what everyone’s focused on for the year. It feels like it will be pretty steady for 2018.”—M.G.

7. Paul Vanderslice, David Bouton and Joseph Dyckman

Co-Heads of U.S. CMBS at Citigroup

Last Year's Rank: 12

Citigroup completed 45 CMBS deals in 2017, up from 26 deals in 2016. While market volume was up 17 percent from the previous year ($89 billion from $76 billion), Citi’s increased 33 percent to $8 billion from $6 billion. The bank also increased its activity in conduit deals ($4.1 billion) and single-seller deals ($3.9 billion).

The bank was the canary in the coal mine in leading the first conduit risk retention deal of 2017—the $1.4 billion CGCMT 2017-CD3 transaction. “It was kind of fun,” Paul Vanderslice said of being the industry pioneer in this particular kind of transaction. The deal was the biggest deal of the year and done as an “L” structure with KKR holding the risk. “Nobody had ever done an L structure, so we didn’t have any documents to copy and had to negotiate the first documents.”

Vanderslice said he expected the overall market volume increase, given the wall of maturities coupled with low interest rates. And when it came to the individual CMBS shops’ activity, size mattered.

“I’d say we benefited in being a big bank,” Vanderslice said. “Between risk retention and investors requiring a couple of major dealers on shelves, the bigger you are, you tend to get more business. Anyone who holds their own should grow with the market, and we grew with the market.”

In addition to being part of the $1.2 billion CMBS loan on 280 Park Avenue, transaction, highlights include a $955 million acquisition loan for Blackstone’s purchase of International Market Centers from Bain Capital Private Equity and Oaktree Capital and a $1.8 billion financing package for Blackstone on the Cosmopolitan of Las Vegas hotel and casino.

“Size favored the CMBS market,” Vanderslice said. “The GM Building, The Cosmopolitan Las Vegas, the Caesars Las Vegas refinancing...who else could have done those deals except the CMBS market?”—C.C.

8. Matt Borstein and Ed Adler

Head of Global Commercial Real Estate; Head of U.S. Origination at Deutsche Bank

Last Year's Rank: 3

Deutsche Bank saw a slight uptick in transaction volume last year, issuing $9.95 billion in CMBS across 29 deals, compared with $9.74 billion via 25 deals in 2016. Its market share, however, declined to 10.4 percent from 12.8 percent.

Officials at the bank weren’t able to chat with Commercial Observer for the list, but Deutsche Bank certainly made its fair share of headlines.

In August 2017, Deutsche teamed up with Goldman Sachs, Citi Real Estate Funding and Barclays Bank to provide $1.075 billion to Vornado Realty Trust and SL Green Realty Corp. for the refinancing of the roughly 1.3-million-square-foot office building at 280 Park Avenue. In November, the bank, along with HSBC, provided an $800 million, six-year, floating-rate loan to Fosun International for the refinancing of the 2.1-million-square-foot office tower at 28 Liberty Street.

The company also joined with Goldman Sachs and Morgan Stanley last May to provide $760 million to Crown Acquisitions to refinance the commercial properties that make up the Olympic Tower at 645 Fifth Avenue plus three nearby properties. The loan consolidates a previous $250 million Deutsche loan from 2012 and a new $510 million mortgage the trio provided. Deutsche also helped shaped a significant aspect of what will be New York City’s future with a $271 million loan package in July to Vornado and Related Companies to fund an early portion of the Moynihan Train Hall project, which will include 700,000 square feet of office and retail space, and is expected to be completed by 2022.

Deutsche Bank is off to the races this year, with several major loans announced in January. Those deals include a $176 million loan to Savanna for the development of Vandewater—a 32-story, 170-unit condominium at 525 West 122nd Street in Morningside Heights—and a $308 loan million to the El-Ad Group and Silverstein Properties to refinance the condominium at One West End, part of the seven-building Riverside Center complex.—Larry Getlen

9. Warren de Haan, Boyd Fellows, Chris Tokarski and Stew Ward

Managing Partners at ACORE Capital

Last Year's Rank: 10

“We launched the business three years ago and had a plan to be one of the true leaders in the unregulated private lending space in commercial real estate,” Boyd Fellows said. “That was really the goal.”

Goal accomplished. The young private lender’s originations topped $5 billion last year, matching 2016’s figure.

“In 2016 we got off to the races then in 2017 the world changed—there was a lot more competition and countless new entrants—but it actually ended up being very similar to 2016,” Fellows said. “We were able to validate our leadership position with another very big execution in an even more competitive environment.”

Warren de Haan added, “The hallmark of the year was proving to the market that we are a dominant player in terms of total transaction volume. The suite of products that ACORE has transcends every single part of the capital stack and every need of our borrowers. We really are a full-service lender and that puts us in a position to continue to grow.”

ACORE’s 72 deals last year include a $150 million loan on 10 Jay Street in Brooklyn—a 10-story office conversion project along the Dumbo waterfront—for Glacier Global Partners and Triangle Assets; a $131.7 million loan for the ground-up construction of AMCAL Swensen’s The Graduate—a 19-story student housing building in San Jose, Calif.; and a $121.24 million first mortgage and mezzanine loan for the purchase and renovation of 311 West Monroe, an office building in Chicago’s West Loop area.

ACORE has originated over $10 billion in debt in just over two years, and 37 percent of those loans have been repeat borrower transactions. “We can provide full service, from origination through seamless underwriting, through asset management,” de Haan said. “The culture of ACORE permeates all the way through the organization, so clients know they can borrower very well-priced capital with flexible terms as well as great customer service. That provides a great experience for a borrower up and down the curve.”

ACORE ended 2017 with its busiest quarter to date, originating $2.1 billion across 30 loans. A hard act to follow but maybe not for ACORE. So far, 2018’s deal pipeline is surpassing last year’s on all metrics, de Haan said. Stay tuned!—C.C.

10. Ralph Herzka and Aaron Birnbaum

Chairman and CEO; Executive Vice President at Meridian Capital Group

Last Year's Rank: 6

For last year’s list, Ralph Herzka told Commercial Observer that 2016 was a “frenetic year of fast-paced finance.”

It would be difficult to characterize any given Meridian Capital-style year any differently, being that the company can be expected to trump any competitor with its deal count, which reached $32.4 billion across 3,072 transactions in 2017, although down just a tick from the $35 billion volume reported in 2016. It also closed $1 billion in investment sales.

“The environment was fast paced and highly competitive,” Herzka said via email. “New York City saw a decline in overall sales activity, which impacted acquisition financing volume as well. Toward year-end and into early 2018, we have observed a material pickup in volume which is always great to see.”

Meridian’s Abe Hirsch and Zev Karpel arranged $1.4 billion in acquisition financing for the Beacon Portfolio, a 25-property multifamily portfolio—totaling a combined 9,677 residential units—throughout the Washington, D.C., metro area, Pennsylvania, Maryland, Illinois, Massachusetts and New Jersey. The financing was comprised of a combination of Freddie Mac fixed- and floating-rate debt—sourced through Berkadia—as well as five-year, fixed-rate, balance sheet financing provided by New York Community Bank.

In December, the firm secured a $500 million construction loan from J.P. Morgan Chase to finance New York-based 601W Co.’s planned redevelopment of the Old Chicago Main Post Office—a location the city of Chicago offered up as a potential location for Amazon’s second offices—into an office property. The construction loan was one of the largest loans secured in the history of the city’s real estate industry, the Chicago Tribune reported at the time of the financing.

That month, Meridian also arranged a $360 million package for the Wolfson Group to refinance the 35-story, 835,651-square-foot office building at One State Street Plaza in the Financial District. The refinance also included the leasehold interest in air rights associated with RFR Holding’s 17 State Street, also in Lower Manhattan.—Mack Burke

11. Alan Wiener

Group Head of Wells Fargo Multifamily Multifamily

Last Year's Rank: 2

It’s hard to think about Wells Fargo and not think Alan Wiener.

The bank’s multifamily production remained relatively flat at $14.4 billion from approximately $14.5 billion in 2016 as it weathered a storm caused by an increase in competition from debt funds and alternative lenders, an unpredictable interest rate environment and a challenging tax landscape.

Wiener’s group was involved in high-profile multifamily deals in New York City at a time when its multifamily lending volume dipped as low as 24 percent year-on-year in the third quarter of 2017, according to a third-quarter multifamily report from Ariel Property Advisors.

The team was very active in the affordable housing space, making 16 affordable housing loans in New York and aggregating $760 million for 2,726 combined units. They also scooped up $400 million in tax credits on 11 different properties, totaling 2,076 units. “I think we did some fascinating deals,” Wiener said.

The largest deal produced by the San Francisco-based lending giant was in June 2017 when it dished out a combined $714 million to finance Brookfield’s Urban America Pool, which includes five Upper Manhattan properties—3333 Broadway; River Crossing at 1940 First Avenue; The Heritage at 1309 Fifth Avenue; The Miles at 1990 Lexington Avenue; and The Parker at 1894 Lexington Avenue—and 2,959 apartment units.

For 2018, “we’re pulling back on construction—we have to,” Wiener said. “And that’s on the Class A properties. On the affordable side, its not limited because there’s no market risk. There’s huge demand, and that’s where [New York City] puts in a lot of subsidy, and the city and state have robust programs for it.

“I’m anticipating rate rises until market absorption heats up on the rental side,” he added. “We’re going to be careful in what we do. We’re not going to buy land that’s too expensive, and with us pulling back and developers pulling back, you’re going to see less in the short term [within the next year] but not on the affordable side.“—M.B.

12. Grant Frankel, Philip McKnight and Ken Ziebelman

Managing Directors at Eastdil Secured

New

With $57.1 billion in originations in 2017—up from $41.1 billion in 2016—Eastdil Secured undoubtedly left its mark with several high-profile transactions.

With such a large footprint and offices across the globe and in every major U.S. market, these three senior Eastdil officials stress the importance of teamwork and how it translates to a seamless execution.

“We generally follow our clients, and then we’ll work with our local experts,” Grant Frankel said. “For example, if we’re doing a deal in Boston, my colleagues [in New York City] are a part of the team. We make sure our clients have a seamless process, and it’s important that we know how they work.”

With around 50 debt professionals at the ready, the firm is producing close to $1 billion per professional. The firm’s average deal size is $150 million.

The firm’s pedigree, coupled with its process and execution, had it involved in some of 2017’s most notable transactions. One such deal was the firm’s arrangement of $2.3 billion to refinance Boston Properties’ General Motors Building, the renowned 50-story, 1.8-million-square-foot office tower at 767 Fifth Avenue, which houses the iconic Apple store below grade.

The 10-year, 3.4 percent fixed-rate loan replaced a roughly $1.6 billion package of senior and mezzanine debt—which carried a 6 percent interest rate—that was set to expire in October 2017. It marked one of the largest loans ever dispersed on a single asset. “That was a deal that we rate-locked and committed in the CMBS market, so to have a commitment to a rate on a loan of that size was pretty good from our perspective,” Frankel said.

Eastdil also arranged $250 million in floating-rate financing to refinance Midtown Equities, Rockwood Capital and HK Organization’s Empire Stores—a 443,000-square-foot, mixed-use development at 55 Water Street, along Brooklyn’s East River waterfront in Dumbo. The loan has a term of five years, including extension options.

With the markets overflowing with lenders and participants, Eastdil is seeing endless opportunity for growth and advancement. “The competition on the lending side is great,” Philip McKnight said. “Every day there are new entrants in the markets, whether foreign or domestic, who are there to finance a variety of projects—from the construction space to the mezzanine space…We’re one of the first places capital stops. We really pride ourselves on bringing new lenders to clients. We can talk to our colleagues in L.A. or San Francisco or Washington, D.C., and discuss new capital sources.

“Our job is to fully vet and hunt for capital,” he added. “We also have a team in Asia, and we work hand-in-hand with them to discuss some of the market entrants and have a behind-the-scenes view as well.”—M.B.

13. David Brickman, John Cannon, Stephen Johnson and David Leopold

Head of Multifamily Business; Senior Vice President of Production and Sales; Vice President of Small Balance Loan Business; Vice President of Targeted Affordable Sales and Investments at Freddie Mac

Last Year's Rank: 24

Freddie Mac logged a blockbuster campaign in 2017 with its multifamily group financing a record-setting $73.2 billion in loan purchases and guarantees, good for nearly a 30 percent increase over 2016, when it turned over $56.8 billion.

But that wasn’t a sure bet last January, David Brickman recalled.

“At the beginning of the year, we were a little concerned,” he admitted. “After the election, interest rates ran up 100 basis points, and there was some uncertainty. The first quarter…was actually very slow.”

But after investors and developers collected their wits and examined the economy’s fundamentals, business turned around in a hurry.

“We’re proud to have done some of the biggest deals in the market,” Brickman explained, noting that the agency twice executed deals larger than $2 billion: Greystar Real Estate’s acquisition of Monogram Residential Trust and Starwood Capital’s purchase of Milestone Apartments.

“On all fronts, we’re trying to push our ability to serve every part of the market and how we can raise capital,” Brickman said. “We were the largest ‘securitizer’ in terms of multifamily, and [we use that position] to better serve the needs of affordable and workplace housing.”

Success in that area came after a concerted effort to leverage government housing programs even in an uncertain political landscape, David Leopold said.

“With the specter of tax reform looming, the market [for low-income housing tax credit deals] was dramatically off,” Leopold recounted. “So we made a concerted effort to overcome the decline in the tax-equity subsidy space. We executed more portfolio trades, and we also focused specifically on mixed-income transactions.”

The bank also recorded an impressive showing in small-balance financings—deals that sit between $1 million and $7.5 million.

“That really is core workforce housing,” Stephen Johnson said. Last year, the bank’s small-balance business grew to $7.8 billion from $4.6 billion the year before—a 70 percent improvement.

“The most important thing to us and our business is squarely workforce housing,” Johnson said. “[Otherwise], I don’t think we would have invested in the space.”—M.G.

14. Jeffery Hayward and Michele Evans

Executive Vice President of Multifamily; Senior Vice President and COO of Multifamily at Fannie Mae

Last Year's Rank: 25

It was the second straight record-setting year for Fannie Mae Multifamily, which finished 2017 with more than $67 billion in financings under its belt. Those deals—including debt that supported more than three-quarters of a million apartments—provided the firepower for the agency to issue $65.4 billion in mortgage-backed securities. And as if that wasn’t enough good news for Fannie’s residential team to toast during its designated underwriting and servicing program’s 30th anniversary, the group topped the $12 billion mark in its guaranteed multifamily structures product.

Talk about a parade of big numbers.

Still, if those headlines left Jeffery Hayward giddy, he managed to play it cool, emphasizing that the agency hadn’t gone dumpster-diving for new material.

“The size of the market did not surprise us,” said Hayward, who marked his own 30th anniversary at the firm last year. “Lenders like doing a lot of quality business with us, and [what] we did in 2017 [was] as good as what we did in 2016.”

And all that’s not to mention how Fannie’s green financing program—which backs eco-friendly upgrades developers make to multifamily properties—grew by 800 percent. The agency’s success in green financing gave Michele Evans the most pride out of all her team’s 2017 accomplishments because the renovations it funded at apartment complexes around the country helped the environment as well as landlords and tenants’ bottom lines.

“When we look at the numbers, we saved enough water to fill 42 billion glasses,” Evans said. Other projects conserved enough electricity to power as many as 80 million cellphones for a year.

The good work doesn’t stop there, as Fannie Mae also notched its best-ever results in the affordable-housing space. That represents work that defines the government-sponsored entity’s spirit best, Hayward said.

“The people who come to work at Fannie Mae are really into affordable housing,” Hayward said. “If you talk to a person about why they work here, affordable housing will be their answer.”—M.G.

15. Raymond Qiao

Chief Lending Officer at Bank of China

Last Year's Rank: 1

Other Chinese investment institutions have seen their overseas activities handcuffed by political considerations in recent months, but the Bank of China still had the firepower to generate plenty of headline-worthy lending in 2017.

Start with the $518 million mortgage loan that the bank sealed in December on Industry City, the 5.7-million-square-foot mixed-use project on Brooklyn’s waterfront. (The bank joined with SL Green Realty Corp. on the deal.) That behemoth financing was preceded by two no-less-noteworthy Manhattan transactions: a pair of $300 million loans supporting 50 Hudson Yards and 5 Times Square—each part of separate multilender megadeals with combined values of more than $2.25 billion.

But the bank’s achievements weren’t limited to New York City, as it took the lead on two high-profile deals on the left coast, too. A short-term $389 million financing from Bank of China provided pre-stabilization financing for a luxury rental project in the Century City section of Los Angeles, and the bank was also the lead construction lender, to the tune of $375 million, on Uber’s new headquarters at the site of the Golden State Warriors’ new arena in San Francisco’s Mission Bay neighborhood.

Though the bank thrived, Raymond Qiao admitted being somewhat taken aback at just how competitive real estate financing grew last year. “Commercial real estate is no longer an alternative asset class,” he said. “As a result, what surprised us about 2017 was the amount of capital available to be deployed for debt investments throughout the entire debt stack—not just the senior tranches.”

Government moves that seemed to rebuke Chinese firms that were overextended abroad—and fears of an escalating trade war over new U.S. tariffs—have many observers bearish on Chinese lenders’ role in U.S. commercial real estate. But Qiao said Bank of China watchers shouldn’t expect the institution to flee the New York City scene anytime soon.

“Our commitment to the U.S. is evidenced by the New York branch’s flagship 475,000-square-foot headquarters near Bryant Park and our Chicago and Los Angeles branches’ recent office expansion,” Qiao said, noting that 90 percent of its U.S.-based employees are local hires. “Bank of China is very much committed to the U.S. for the long term, supporting U.S. jobs and corporate responsibility.”—M.G.

16. David Lehman

Global Head of Real Estate at Goldman Sachs

Last Year's Rank: 22

The past 12 months have been replete with big changes for Goldman Sachs, from David Solomon’s rise to become the sole presumptive candidate to succeed Lloyd Blankfein’s chairmanship to the launch of Marcus, the bank’s new platform for low-balance consumer lending and savings.

But it was business as usual on the real estate front, where David Lehman continues to control the global bank’s real estate finance business. The New York-based executive’s team turned in an especially strong year on the CMBS front, snagging the top spot on the league tables with $12.4 billion in CMBS issuance over 32 deals. That’s good for a remarkable 60 percent year-over-year increase from last year, according to Commercial Mortgage Alert.

At the same time, however, Goldman’s origination business dried up significantly, shrinking to $4.1 billion from $6.8 billion in 2016. Lehman, a 1999 graduate of Washington and Lee University, presided over some supersized loans last year. The bank led a $1.2 billion refinancing on One Worldwide Plaza in September, playing a key role in a 10-year loan on the mixed-use tower at 825 Eighth Avenue in Midtown. Earlier in the year, Goldman was part of a troika of lenders who combined to loan $760 million on another Midtown office refinancing secured by Olympic Tower, at 641 Fifth Avenue.

And in November, the bank provided $262.2 million to Lightstone Group to back its refresh of the Marriott Moxy Hotel at 485 Seventh Avenue in the Garment District.—M.G.

17. Brannon Hamblen, Greg Newman, Tucker Hughes and Richard Smith

COO of Real Estate Specialties Group; Managing Director of Originations in Southeast U.S.; Managing Director of Originations in Central and Western U.S.; Managing Director of Originations in Northeast U.S. at Bank of the Ozarks

Last Year's Rank: 31

It’s one thing to chance a debt investment on the refinancing of a fully occupied, Class-A Manhattan skyscraper—or even to originate a mortgage on a value-add multifamily play in a suburban workforce housing market.

Staking your money in a transaction where the cash-flow-ready property-to-be is no more than a gleam in the eyes of an architect and a developer: That’s a different order of business entirely.

Boldly stepping where so many well-established lenders fear to tread, Bank of the Ozarks didn’t miss a step this year in the high-risk, high-reward realm of construction lending, churning through $10.5 billion in loans, compared with $8.24 billion in 2016 and $5.63 billion in 2015. Not too shabby, eh?

Although shares in the bank tumbled 11 percent on the July 2017 day when Chief Lending Officer Dan Thomas abruptly announced his resignation, Rich Smith Brannon Hamblen, Greg Newman and Tucker Hughes finished the year strong.

The bank transacted across the country, closing construction loans right, left and center.

In May, Rescore Property Corp. scored a cool $100 million from the bank to proceed with construction of its 386-unit Hollywood apartment building known as the Rise; also in May, the lender took us to church, lending $90 million in financing for Extell Development’s condominium development on the former site of the Park Avenue Christian Church’s rectory at 1010 Park Avenue; in July it lent $218 million for the construction of the 516-key, 4.5-star JW Marriott Bonnet Creek hotel; and in September, it provided a $170 million mortgage (along with Arbor Commercial Mortgage and Melody Capital Partners) for The Chetrit Group’s mixed-use hotel and retail development at 255 West 34th Street.—C.C and M.G.

18. Jeff Fastov

Senior Managing Director at Square Mile Capital Management

Last Year's Rank: 23

Hey, man, don’t be such a square! Unless you want to rack up a cool $3.5 billion in originations in one year, that is.

Once again, Jeff Fastov and his team at Square Mile Capital Management outdid themselves, increasing their lending activity in 2017 compared with the previous year (when they originated $3.3 billion).

“I would say that things are going according to plan,” Fastov said of the firm’s continued success. “The alternative lender universe is responding to a real need for capital that not only responds to advance rates beyond where banks go but also provides the service and creativity that the market so desperately wants.”

The past year was quite the year for the nonbank lender as it flexed its significant muscle across the U.S. Deal highlights include a $133 million acquisition and redevelopment loan to Invesco Real Estate and SteelWave for The Press—the 420,000-square-foot creative office property redevelopment of a former Los Angeles Times printing facility in Costa Mesa, Calif.; a $150 million construction loan to Tavros Development Partners and Charney Construction for The Dime mixed-use development in Williamsburg, Brooklyn; and a $118 million loan for Moinian Group’s Renaissance Tower, a 1.7-million-square-foot office building in Downtown Dallas.

“Because we are an owner-developer of properties that are changing use,” Fastov said of The Press deal, “it gave us the confidence to be a lender on the same property type. I think the L.A. Times building is a similar story in that change of use.”

He added, “It’s an example where the execution of the business plan is the key. You have SteelWave and Invesco in that deal and we have high confidence that they’ll execute at a very high level. Interestingly, they are just as focused on who their lender is and that lender being able to appreciate a business plan that will maximize the property’s value. So, it kind of helps that we’re in the business as well.”

As this list goes to press, Square Mile is in the midst of closing a $250 million construction loan for the Essex Crossing mixed-use project on the Lower East Side on behalf of sponsors Goldman Sachs, Taconic Investment Partners, BFC Partners and L +M Development Partners.

“It’s a very exciting project with a who’s who of sponsorship,” Fastov said. “It’s also a project that’s going to completely transform its neighborhood. It’s of such a scale that it will become a place in and of itself.”

When it comes to the trench warfare for each deal, Fastov isn’t losing any beauty sleep.

“That’s where our relationships and history with borrowers really makes a difference, because they’ll come back to the people they trust. If you perform you see repeat business, and that’s the best business. So we’re starting to enjoy the benefits of our franchise in that way.”—C.C.

19. Willy Walker

Chairman and CEO of Walker & Dunlop

Last Year's Rank: 48

What hasn’t Willy Walker done with this company in the commercial real estate arena since he gripped the reins and took it public in December 2010?

For the ninth consecutive year, Walker & Dunlop eclipsed its prior-year transaction volume, hitting $27.9 billion in 2017, up from $19.3 billion in 2016—a 45 percent climb on the year. The company’s mortgage servicing portfolio reached a colossal $75 billion, up from $50 billion just two years earlier, while its investment sales practice also climbed to $3 billion in 2017 from $1.52 billion in its 2015 inception year. And, Walker saw revenues climb 24 percent year-over-year to $711.9 million.

On Sept. 20, W&D announced its largest batch of financing in company history—$1.9 billion in fixed- and floating-rate Freddie Mac loans delivered to Greystar for the acquisition of multifamily properties in major metropolitan centers throughout the country.

“You don’t get invited to that party unless you’ve created a brand that people associate with success and as one of the best commercial real estate firms in the U.S.,” Walker said.

Walker also mentioned that his firm worked with other industry groups in December to help carve out a provision in the Senate’s Tax Cuts and Jobs Act and exempt mortgage servicers from being hit with upfront taxes on anticipated servicing income; under the original law, it would’ve changed the treatment of this deferred income and servicers would have been taxed once the servicing right was created.

“I think we overpunch our weight on general policy with our work with GSEs [government-sponsored enterprises] and with our mortgage banking practice and having our hands in regulatory issues that many other firms cannot access because of our D.C. location,” Walker said.

W&D has lived on making moves where other firms choose not to play. The Bethesda, Md.-based firm had just one office when Walker joined the company in 2003 and now with over 25 offices across the country and a $1.83 billion market cap, the company’s stock reached its highest level since it hit the market when it touched $55.81 per share on Oct. 18, 2017.

“We’ve seen opportunities to continue to grow with and through cycles,” Walker said. “There are no reasons to stop our recruiting and acquisition efforts. Competition in 2016 was standing still, while we were aggressively expanding, and because we didn’t get caught as a deer in the headlights, we kept investing. As a result, that paid off brilliantly in 2017.”

By 2020, the company wants to have reached $1 billion in annual revenues, $30 billion to $35 billion in annual loan originations and $8 billion to $10 billion in investment sales volume; it wants to expand its servicing portfolio to $100 billion and grow its asset management platform to $10 billion.

Just another day at the office.—M.B.

20. Robert Merck and Gary Otten

Head of Real Estate and Agricultural Finance; Head of Real Estate Debt Strategies at MetLife

Last Year's Rank: 16

Although MetLife’s commercial real estate loan origination volume dipped slightly to $14 billion last year from a record high $15 billion in 2016—and from a then-record $14.3 billion in 2015—it executed $16 billion in commercial real estate transactions globally. That cements the insurance behemoth as our lists most powerful life company.

The company attributed the slight drop to its shift in strategy to offer smaller, more frequent debt investment opportunities to its growing list of third-party clients.

“The business is robust,” Gary Otten said. “We basically executed in accordance with our plan. In expanding our third-party asset management platform, we actually did a record number of transactions. We expanded our capital sources, which requires more transactions, but in slightly smaller dollar volumes—still in the $90 [million] to $100 million range.”

In November, MetLife shelled out large sums of capital on numerous properties throughout the country, including when it paired with TH Real Estate to lend $200 million of a $400 million mortgage loan on the 1.6-million-square-foot Freehold Raceway Mall in Freehold, N.J.

“It was a very strong year again for us,” Robert Merck said. “We did a significant number of deals and were able to supply mortgage opportunities for our general account and for the third-party institutional clients in our mortgage program. The broader real estate market here in the U.S. continues to see a decent amount of supply, and the demand was well matched.”

A month later, the life company followed up the Freehold loan with $143.5 million in debt on the Orlando CBD Collection, a portfolio of three high-rise office buildings in downtown Orlando, Fla. It also originated $335 million on Warner Center Towers, a six-building office complex in Los Angeles, and provided $60 million on the Graham Industrial Portfolio, a collection of 10 industrial properties scattered throughout the southeast.

“It was also a year where I was surprised by the demand in floating-rate loans,” Otten said. “I was surprised because interest rates are up and treasuries yields are up. I expected people to try to lock in rates, but there wasn’t much of a trend there at all, which for us is unusual, being a life company. We’re doing about 50 percent of our business in the floating-rate space.”

They didn’t stop there. Globally, MetLife’s real estate platform, which includes origination and asset management capabilities, saw an 9.1 percent increase from last year to $76.4 billion in global equity assets managed.—M.B.

21. David Durning and Marcia Diaz

President and CEO; Global Head of Originations at PGIM Real Estate Finance

Last Year's Rank: 17

PGIM Real Estate Finance saw a slight jump in its origination number in 2017 to $14.8 billion from $13.9 billion in 2016.

“In a year where transaction volume was down, we managed to slightly increase originations domestically and have an increase year-over-year related to our international activities,” David Durning said. “Our participation in riding the wave of multifamily financings was a record year for us as well.”

This activity was headlined by PGIM setting record-highs in lending on multifamily properties and logistics centers in 2017, according to Durning. The company also poured $1.5 billion into international markets such as Australia, Canada, Japan, the U.K. and other countries within the Euro area.

“The big story for us was that we’ve always been a strong lender to industrial properties—we’ve liked industrial for a long period of time—but last year we did over one third of our business in logistical properties, which is a historic record-high for us,” Durning said. PGIM offers a variety of loans, including preferred equity and mezzanine pieces as well as agency products. For last year’s list, PGIM said it began offering financing on more core-plus assets with value-add potential, in which it invested roughly $184 million in 2017.

“We’re off to a very good start [in our core-plus lending],” Marcia Diaz said. “We started building momentum in the fourth quarter of [2017] and that has carried over into 2018. Our target this year is $1 billion, and with deals closed and signed up we’re already on target to do that, so we feel really good.”

One notable transaction the company announced in November included two loans totaling $275 million that it provided to refinance Trinity Place Phases 1 and 3 in downtown San Francisco. The 10-year refinancing package on the apartment complex, when combined with an already in-place $73 million loan on Trinity Place Phase 2, put PGIM’s exposure to the property at $348 million. Trinity Place Phases 1, 2 and 3 were completed in 2009, 2013 and 2017, respectively.—C.C. and M.B.

22. Gino Martocci and Peter D’Arcy

Co-Head of Commercial Banking and Executive Vice President; Regional President of New York City and Long Island and Head of the Commercial Real Estate segment at M&T Bank

Last Year's Rank: 19

Gino Martocci and Peter D’Arcy’s astute deal-making has helped them navigate this currently crowded market of real estate lenders as they’ve followed their clients—many of whom have borrowed from the bank for 15 to 40 years, according to Martocci—to where they’re looking to unload equity.

The bank reported financing just over $11 billion worth of business on the year, down from approximately $13 billion in 2016. But, that didn’t keep M&T out of some of New York’s most attractive deals on the year.

“The market in general was slower, but we had a very good year,” D’Arcy said. “We were active during a period that included a pullback from competitors on certain products.”

In one of its first major deals last year, M&T lent $120 million to Silverstein Properties in February to facilitate the firm’s purchase of a majority stake in the Movielab building at 619 West 54th Street from Taconic Partners. Taconic kept a 10 percent stake in the 325,000-square-foot, 10-story property, The New York Post first reported at the time.

In September, the bank provided $250 million in floating-rate financing in the form of a land loan to a development trio—Midtown Equities, Rockwood Capital and HK Organization—to refinance Empire Stores, a 443,000-square-foot, mixed-use development at 55 Water Street, along Brooklyn’s East River waterfront in Dumbo. The loan was arranged by Eastdil Secured and had a term of five years, including extension options.

“Empire Stores was one of the earlier large redevelopments of retail and office in Brooklyn,” D’Arcy said. “We’re very proud of the project, and we think it’s wonderful. We’re happy to have played a role in it.”

In November, M&T paired with Natixis as co-lead arrangers to lend a $195 million senior loan to landlords SL Green Realty Corp. and PGIM to refinance and help complete the lease up of Tower 46, the 347,694-square-foot office building at 55 West 46th Street. It was a floating-rate, interest only loan with a three-year initial term and three, one-year extensions.

Martocci said: “I think staying close to your clients and understanding where they think the market is going and where they’re making their equity investments and why [is what’s important for us].”—M.B.

23. Joseph Fingerman and John Zieran

Co-Heads of Commercial Real Estate at Signature Bank

Last Year's Rank: 7

George Klett’s retirement late last year marked the end of an era for Signature Bank, which had thrived under his leadership for 10 years. Prudence and conscientiousness were the watchwords during the industry veteran’s tenure, who bragged of having never lost even a dollar on any of the 7,000 loans he originated during his career.

Now that two of Klett’s longtime lieutenants, Joseph Fingerman and John Zieran, have taken the helm, the theme is continuity above all else. “There haven’t been any wholesale changes,” Zieran said. “We’re still working with the people we always worked with,” referring to the rest of Signature’s team of about 20 who work in commercial real estate originations.

It’s that roster of familiar faces that keeps longtime customers from straying far, the New York-based executives explained. “[Clients] come back for the single point of contact,” Fingerman said. “They’re able to come to John and me because these are relationships that span decades. They’ve been borrowing from the team for years.”

“We take the execution risk out of the equation,” Zieran added. “There are no surprises.”

The same could be said of Signature’s lending results. The bank always seems to notch dependably impressive loan figures considering its business rarely takes it beyond the tri-state area. Last year, total debt funded was down about 25 percent for the team in an increasingly crowded financing market. But Signature still cleared $4.4 billion in lending: not bad for a home-town shop that consistently ranks among major financial journals’ lists of the most trustworthy financial institutions.

As to whether to expect a resurgence or a continued slide in 2018, the bank’s new leaders are probing their tea leaves for any signs of where interest rates will go next.

“If the rates move up too fast, that will be a problem,” Fingerman said. “Hopefully, it will be slow, steady rate increases. Buyers and sellers will start to see eye to eye, and transaction volumes will pick up.”—M.G.

24. James Carpenter and John Adams

Senior Executive Vice President and Chief Lending Officer; First Senior Vice President, Chief Administrative and Senior Lending Officer at New York Community Bank

Last Year's Rank: 8

New York Community Bank originated $6.4 billion in commercial real estate financing in 2017 with $3.7 billion of that secured by property within the five boroughs. NYCB’s main focus was on multifamily lending, which represented 80 percent of its total New York City lending in 2017, and the bank anticipates continued emphasis on rent-regulated multifamily in 2018.

Significant deals for the bank in 2017 included the refinancing of a package of nine multifamily Bronx properties containing 529 apartments with an aggregate loan amount of $70 million; the refinancing of 12 multifamily properties totaling 1,062 units and two commercial properties consisting of five retail spaces and 20 offices located in Manhattan, Queens and the Bronx, for $174 million; and the refinancing of a portfolio of 11 multifamily properties comprised of 534 apartments and five offices in the Bronx, Queens, and Manhattan with an aggregate loan amount of $96.8 million. All of these were structured as individual loans on a five-year fixed-rate term.

The bank also refinanced a $92 million multifamily portfolio with 763 units in Brooklyn and Manhattan. The 10-year financing was structured as individual loans with a rate fixed for the initial three years with fixed adjustments in years four and six.—L.G.

25. Greg Murphy

Head of Real Estate Finance Americas at Natixis Real Estate Capital

Last Year's Rank: 42

When it comes to lending, some banks just have that je ne sais quoi.

“We had a very good year,” Greg Murphy said.

No doubt. Last year Natixis Real Estate Capital more than doubled its $3.2 billion 2016 origination volume to $7.52 billion, across 105 loans and 47 states. That total includes $2.84 billion in securitized loans—making Natixis the number 10 contributor to U.S. deals—and $2.88 billion in syndicated loans, including senior mortgages, B-notes, mezzanine loans and preferred equity.

Murphy’s saw a significant increase in floating-rate lending, the volume mirroring the market’s overall increase in floating-rate CMBS. “What we tried to do was find places where we could add the most value to our clients and our investors,” Murphy explained. “We were able to match up the right capital with the right deals, whether it was on the bank syndication side or finding buyers of higher-yielding B-notes and mezz, both domestically and internationally.”

Stand-out transactions include a $480 million construction loan for EchelonSeaport, a 1.3-million-square-foot mixed-use project in Boston’s Seaport Square; a $266 million acquisition loan for Amazon’s Bellevue, Wash., office; a $475 million loan on RFR Realty’s 285 Madison Avenue (Natixis’ share was $270 million) near Grand Central Terminal; and a $359 million loan to Ivanhoe Cambridge for 85 Broad Street in FiDi.

“We were able to create the first CMBS green bonds on 85 Broad Street,” Murphy said. “That was a very exciting deal. It was complex and we sold subordinated debt, securitized some of it in a conduit deal and also had some standalone rake bonds that we were able to make into green bonds.”

It’s an initiative that Natixis is championing. “We have a bank-wide effort to find ways to do more in the green space,” Murphy said. “We’re looking for opportunities to improve our green profile.”—C.C.

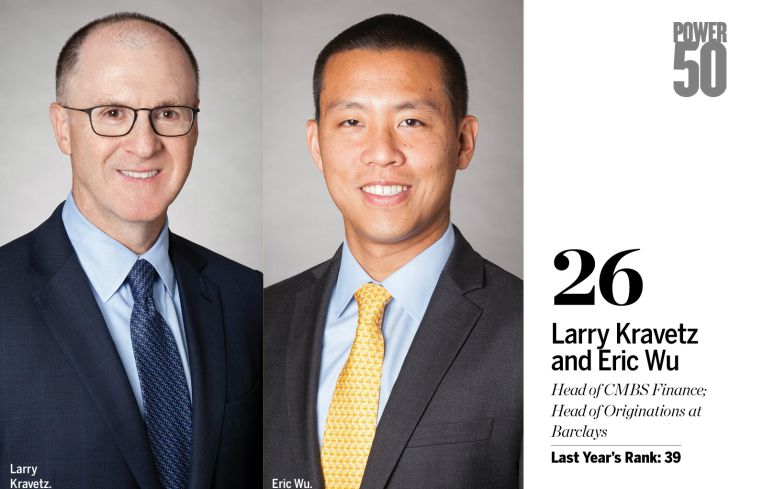

26. Larry Kravetz and Eric Wu

Head of CMBS Finance; Head of Originations at Barclays

Last Year's Rank: 39

“We had a great year last year,” Larry Kravetz said. “We did $3.5 billion in 2016, and last year we almost doubled that and did $6.5 billion. We clicked on all cylinders.”

The majority of that volume was CMBS. On the conduit side Barclays’ volume was up about 25 percent—outperforming the market, which was flat overall—and the bank led or co-led nine standalone deals.

In New York one of the most notable transactions was the $430 million fixed-rate financing of 225 and 233 Park Avenue South, Buzzfeed’s location as well as the marketing headquarters for Facebook. “The owner did a phenomenal job of turning what was a B-building and turning it into a very attractive asset,” Kravetz said. “There were lots of moving parts and it was a complicated deal. All of our competitors wanted a piece, and we won on structure and pricing.”

“We exited the loan in a number of conduit transactions,” Wu added. “What we did is we sold a big part of the loan as a mezzanine loan. So there was a $250 million senior mortgage and a $180 million subordinate piece. A lot of competitors were looking at it as a standalone deal, and we thought this gave us an advantage.”

The standalone deals Barclays led include a $712 million refinance of the historic Hotel del Coronado hotel in Miami on behalf of Blackstone Group and a $540 million loan on the JW Marriott Grande Lakes and the Ritz-Carlton Grande Lakes in Florida, also on behalf of Blackstone.

Barclays showed its muscle in taking down part of the $2.2 billion refinance of Caesars Palace Las Vegas. The complex financing involved five lenders and took a year to put together. “The deal was part of Caesars coming out of bankruptcy, and a number of corporate financings had to be sequenced with it. There was a long period of advisory work to get them to the point where they had the right financing structure to emerge from bankruptcy,” Kravetz said.

“One thing that CMBS in general and Barclays in particular does well is that we’re comfortable taking down size and we can write big checks,” Wu said. “Plus, we get universally strong reviews about our ability to execute.”

The bank is in the process of its first balance sheet closing—and has a goal of $2 billion in balance sheet deals this year—which will add a fourth leg to its conduit, large loan and warehouse lending businesses. We also should expect to see more activity in CRE CLOs and in Freddie Mac K-series securitizations. Look out!—C.C.

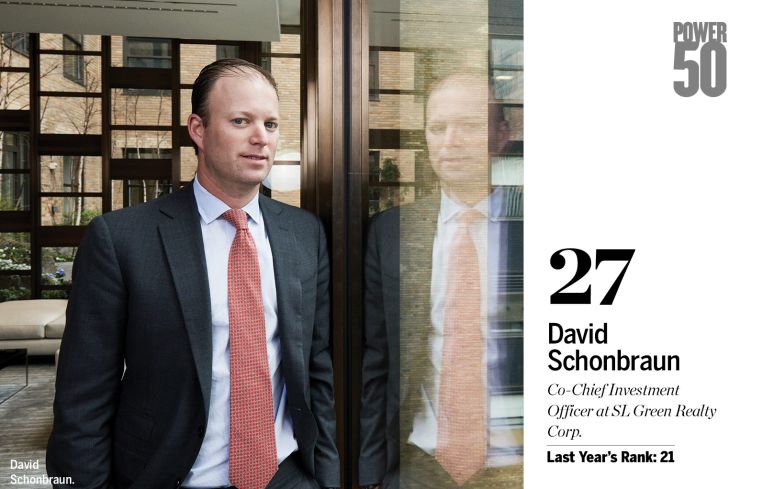

27. David Schonbraun

Co-Chief Investment Officer at SL Green Realty Corp.

Last Year's Rank: 21

It’s not easy being green, once sang Kermit. But, David Schonbraun is proving him wrong.

“Last year was a great year for us,” David Schonbraun said. “We produced north of $210 million in revenues for the company and we did about $1.5 billion in gross originations.”

Schonbraun also led SL Green’s side of its acquisition of a 49 percent stake in Worldwide Plaza (along with RXR). His team’s bread and butter is New York City assets. “We’re not focused on doing as much originations as possible to grow the book as big as possible,” he said. “We try to pick the best assets and best returns to keep our portfolio around the $2.2 billion mark, and within there we optimize.”

SL Green deploys a barbell strategy to lending, often anchoring the bottom of the capital stack—as it did in HNA’s acquisition of 245 Park Avenue—and improving pricing.

It bought a $250 million existing mortgage on Sitt Asset Management’s embattled Two Herald Square, whose foreclosure auction is pending. Then there’s the $170 million mortgage on Normandy Real Estate Partners’ acquisition and redevelopment of ABC Carpet & Home’s headquarters at 888 Broadway.

“We went from buying a mezzanine loan on a 100-percent-leased building to a whole loan on an existing asset to doing a new redevelopment loan,” Schonbraun said, “so we kind of play all throughout the capital stack.”

And let’s not forget the upsized $647 million loan on Industry City on Brooklyn’s waterfront [together with Bank of China], on behalf of a group of developers led by Belvedere Capital and Jamestown.—C.C.

28. Steve Kenny and Brad Dubeck

East Region Real Estate Executive; Commercial Real Estate Banking Executive at Bank of America

Last Year's Rank: 20

Bank of America inked solid commercial real estate business in 2017, originating more than $6.4 billion in CMBS. That strong performance was good for a 23 percent increase over the prior year, as the bank held steady with just under 7 percent market share among U.S. CMBS bookrunners.

But with heightened lending competition from private-equity upstarts and increasingly aggressive life insurers, the bank has had to run twice as fast just to stay in place.

“I think competition—fierce competition—has entered every corner of the industry,” Brad Dubeck said. “In the old days, lending was [a business] with structure and pricing power. Now, competition is everywhere. We were surprised how active the life insurance companies would be in the short-term lending space.”

Dubeck, who works alongside Steve Kenny, explained that the bank is constantly rebalancing its portfolio to maintain exposures in the sectors where it’s most bullish. With retail under threat from e-commerce, Bank of America has found itself steering clear of mildewed malls and shopping centers.

“Retail is a very small part of our origination portfolio,” Dubeck explained. “I can’t think of any large-scale retail transactions that were done last year.”

Instead, the bank has taken up a stronger interest in a booming trade in warehouse and distribution financing nationwide—again, thank e-commerce—as well as opportunities to lend against apartments.

“We’d like to do more industrial, and we’re also being very mindful of Class-A multifamily units around the country,” Dubeck said. “We have a very granular portfolio, and we want to keep the mix about the same.”—M.G.

29. Richard Mack and Peter Sotoloff

East Region Real Estate Executive; Commercial Real Estate Banking Executive at Bank of America

Last Year's Rank: 49

“Oh, the line forms on the right, babe. Now that Macky’s back in town.”

And Bobby Darin’s song, “Mack the Knife,” seems to hold strong in the case of Mack Real Estate Credit Strategies, which vaulted up the Power 50 list this year thanks to a stellar 2017. (Last year was its debut at no. 49.)

Mack went ahead and doubled its volume last year, racking up a smooth $4 billion in originations compared with $2 billion the previous year, with an average deal size of $200 million.

“It’s endemic of the opportunity and demand for our capital, but we’re not about volume, we’re about borrower relationships,” Peter Sotoloff said. “We saw a lot of really interesting situations on very high-quality real estate, and there were some very large transactions in there that are textbook for why we exist as a transitional lender.”

One of those large transactions was a $315 million construction and recapitalization of Penn-Florida Companies’ Via Mizner—a 2-million-square-foot mixed-use project in Boca Raton, Fla. comprised of five components: an 85-unit luxury condominium building; a 164-key hotel; a 366-unit apartment building; 60,000 square feet of retail space and a golf club.

“There were a lot of moving parts to the deal that most people aren’t equipped to get their arms around,” Sotoloff said.

New York property feathers in its cap include a $305 million construction loan for Lightstone Group’s 59-story condominium tower at 130 William Street in the Financial District, a $200 million bridge loan for Ceruzzi Properties’ development of 520 Fifth Avenue in Midtown and a $55 million acquisition loan for Meadow Partners’ 175 West 95th Street on the Upper West Side.

“For anything large and transitional there is still—in our view—limited competition,” Sotoloff said. “There’s still a very robust environment when you’re doing things of a large size in transitional lending.”

Mack is targeting $5 billion in originations in 2018, with $2.7 billion in closed and in-closing deals already under its belt. But, it maintains a thoughtful approach to lending. “We’re very selective,” Sotoloff said, “regarding who we’re transacting with and the markets we’re in.”—C.C.

30. James Millon and Tom Traynor

Executive Vice Presidents at CBRE

New

When James Millon and Tom Traynor joined CBRE from Deutsche Bank a little over a year ago they hit the ground running, sprinting even, arranging $5.1 billion in financings. Their first deal out of the gate was perhaps one of the year’s most talked-about: the $1.77 billion acquisition financing for HNA’s purchase of 245 Park Avenue. Talk about an impressive debut!

“It was a monster deal,” Millon said. “We worked on it for a very long time.”A monster, indeed, and second only to the financing of the General Motors Building in terms of size. (“The GM building comes around every 10 years, and unfortunately this was the year,” Traynor said and laughed.)

Traynor attributes the dynamic duo’s immediate success to three factors. “There’s the skillset and relationships we brought having been principals at an investment bank, CBRE plugging us into an amazing global platform and our ability to form partnerships with some of the players at CBRE—whether it’s Darcy Stacom and Bill Shanahan or the other investment sales teams around the country.”

Millon and Traynor also gave props to colleagues Ethan Gottlieb and Mark Finan for being instrumental in the team’s success.

Deal highlights for the dynamic duo include an $800 million, six-year floating-rate loan on Fosun’s 28 Liberty Street Downtown (Deutsche Bank and HSBC provided the refi) and Atlanta-based Stonemont Financial Group’s $1.3 billion acquisition financing for a portfolio of 100 retail, office and industrial properties across 20 states.

“The best part about this role is that we’re not on the other side of the table from our clients; we’re sitting on the same side, advising them [unlike before]. The second part is that it’s pretty entrepreneurial,” Traynor said.

“From a client perspective, we’ve seen it, done it and lived it—and many times with that client—so there’s a level of comfort there,” Millon said. “From a lenders’ perspective, we frankly weren’t sure what the lenders would think of us, but we problem-solve, we spot issues early and we address them. Lenders are juggling 20 deals at a time, so the more efficient you can make the process the better it is for them.” Along with speed of execution, the pair’s ability to dig deep on more complicated deals is becoming a calling card.

“Stonemont was 83 percent leverage with a lot of mezzanine, 245 Park was fixed-rate financing which is unusual, and 28 Liberty was Fosun’s first deal in the U.S., so they really needed an adviser,” Traynor said. “Certain deals lend themselves to quick executions, but we’re even better with the really hairy deals where the clients really need help.”

“We’re building something that didn’t exist at this massive organization; large loan institutional debt advisory,” Millon said. “So that’s been really fun even though it’s been a lot of hard work. But the good news is there’s a lot still to come and there’s a lot of room for growth.”—C.C.

32. Christopher LaBianca

Head of Commercial Mortgage Originations at UBS

Last Year's Rank: 34

“It was a good year,” Christopher LaBianca said. “It was challenging, certainly, on the CMBS side. There was a lot of trepidation at the beginning of the year with risk retention being implemented. But for us, it turned out to be a good thing because we were an issuer and the market favored lenders who were issuers or willing to use their balance sheet for a B-piece angle. The guys who were not doing that found themselves on the outside looking in.”

Indeed, UBS racked up $3 billion in total originations last year, completing 13 securitizations and issuing eight deals off its own shelf.

“As a year it was flat from the conduit perspective,” LaBianca said. “[As conduit issuers], we were all fighting against the banks to keep some of [these loans] in the conduit world. We were trying to keep our market [share in an] overall finance market that was still healthy.” Under LaBianca’s guidance, UBS also grew the bank’s contributions to CMBS last year to $2.5 million, about 2.5 percent higher than 2016’s level.

Increasingly aggressive ranks of lenders have forced him—and every other lender—to fight harder for each and every opportunity, in “head-to-head combat,” LaBianca said, but UBS held its own on the battlefield.

One of last year’s deal highlight was a joint $550 million refinancing with Natixis on Yorkshire and Lexington Towers, a pair of Upper East Side apartment buildings ,that rolled over three-year-old debt from Deutsche Bank.

This year, the bank is busy readying its balance sheet lending program, where it will be making traditional balance sheet loans and bridge loans on assets that are near stabilization.UBS hopes to use it as a feeder program for its CMBS program, LaBianca said.It has also been busy providing warehouse financing to CLO originators.—C.C.and M.G.

Head of Commercial Mortgage Originations at UBS

Last Year's Rank: 34

“It was a good year,” Christopher LaBianca said. “It was challenging, certainly, on the CMBS side. There was a lot of trepidation at the beginning of the year with risk retention being implemented. But for us, it turned out to be a good thing because we were an issuer and the market favored lenders who were issuers or willing to use their balance sheet for a B-piece angle. The guys who were not doing that found themselves on the outside looking in.”

Indeed, UBS racked up $3 billion in total originations last year, completing 13 securitizations and issuing eight deals off its own shelf.

“As a year it was flat from the conduit perspective,” LaBianca said. “[As conduit issuers], we were all fighting against the banks to keep some of [these loans] in the conduit world. We were trying to keep our market [share in an] overall finance market that was still healthy.” Under LaBianca’s guidance, UBS also grew the bank’s contributions to CMBS last year to $2.5 million, about 2.5 percent higher than 2016’s level.

Increasingly aggressive ranks of lenders have forced him—and every other lender—to fight harder for each and every opportunity, in “head-to-head combat,” LaBianca said, but UBS held its own on the battlefield.

One of last year’s deal highlight was a joint $550 million refinancing with Natixis on Yorkshire and Lexington Towers, a pair of Upper East Side apartment buildings ,that rolled over three-year-old debt from Deutsche Bank.

This year, the bank is busy readying its balance sheet lending program, where it will be making traditional balance sheet loans and bridge loans on assets that are near stabilization.UBS hopes to use it as a feeder program for its CMBS program, LaBianca said.It has also been busy providing warehouse financing to CLO originators.—C.C.and M.G.

32. Matthew Masso and Stefanos Arethas

Head of Commercial Real Estate Finance; Head of Commercial Real Estate Loan Origination at Credit Suisse

Last Year's Rank: 50

Last year marked Matt Masso and Stefanos Arethas’ first in new roles at the helm of commercial real estate finance for the Zurich-based Credit Suisse—and the pair hit the ground running.

“We started 2017 with me stepping into my seat and Stefanos stepping into the head of originations role, so we had to go out and reintroduce ourselves to the market,” explained Matt Masso. It was a smooth transition by all measures.

“Everything went very well in terms of volume, and we ended up doing $3.7 billion in conduit and single-borrower CMBS loans,” Masso said. “We didn’t do a conduit deal until June because we were starting from scratch in terms of our loan inventory, but then we did a deal every couple of months. That’s our plan: to continue to issue deals off our own shelf and be in the market fairly regularly.”

Arethas agreed, emphasizing how important it is to big CMBS borrowers that Credit Suisse was the bookrunner behind more than $3.1 billion in mortgage-backed securities last year—more than double its 2016 issuance figures.

“What caught us by surprise is just how competitive it was between CMBS lenders, particularly with regard to conduit deals,” Arethas said. “But, we continue to compete, and the number of active lenders in the space continues to decline from the 2015 highs. The market is really starting to value the execution and certainty of dealing with the issuer that is controlling the shelf.”

High points for the firm include the market leading structure undergirding their CSMC 2017-CHOP transaction, the first single-borrower CMBS issuance to include nonrated bonds instead of a carved out mezzanine loan.

“We decided it was a more efficient structure to put the entire mortgage into the trust and issue non-rated bonds out of a single borrower deal, having the risk retention at the bottom. That really opened up those bonds to a different investor base and every other dealer has since followed suit.”—C.C. and M.G.

33. Dustin Stolly and Jordan Roeschlaub

Vice Chairmen and Co-Heads of Debt and Structured Finance at Newmark Knight Frank

New

Dustin Stolly left his position as a managing director at JLL in May 2017 and two months later joined forces with Newmark Knight Frank’s Jordan Roeschlaub to head up the firm’s debt and structured finance division, forming one of the most talented and formidable debt arranging duos around.