CBRE: US CRE Lending Markets Expand in Q3 Despite Global Volatility

By Cathy Cunningham December 2, 2016 4:52 pm

reprints

Commercial real estate lending markets expanded in the third quarter with U.S. capital markets conditions becoming a “safe haven” following Brexit-borne volatility, according to CBRE data first provided to Commercial Observer.

Both private commercial mortgages and public commercial mortgage-backed securities markets benefited from tightening credit spreads, meaning that both the number of loan closings and the volume of issuance increased.

CMBS issuance increased to $19.2 billion in the third quarter, a significant increase from the second quarter’s $11.4 billion.

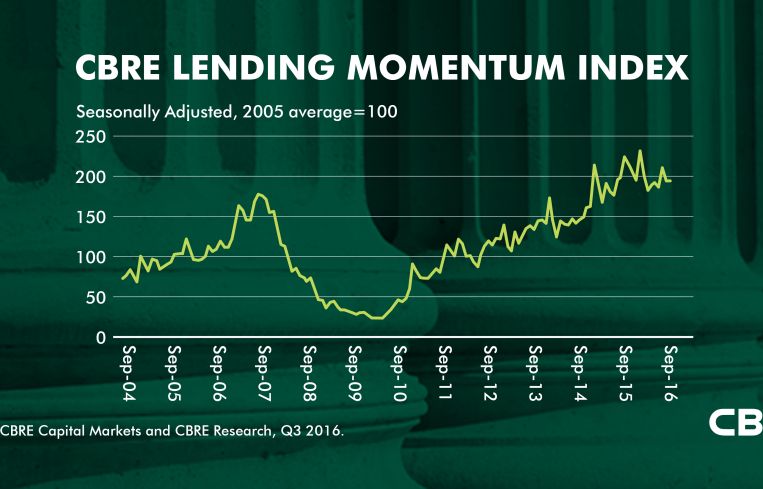

U.S. commercial loan closings were tracked using the CBRE “Lending Momentum Index,” which increased by 4.3 percent in September to 194, indicating a recovery in loan closings compared with March, when the index hit a low of 182. Although the index is still down 13.1 percent from 2015, “the positive lending momentum over the past year is encouraging, especially when viewed against capital markets uncertainty and the direction of U.S. interest rates,” analysts wrote.

Further, agency multifamily origination not only increased in the third quarter but is on pace to set a new record for 2016. Fannie Mae and Freddie Mac’s loan volume spiked to $30.2 billion, a substantial jump from $19.6 billion in the second quarter.

Bank lending cooled, largely due to increased scrutiny on bank underwriting standards and a tightening of credit policies—with bank lenders accounting for 31 percent last quarter compared with 40 percent in the previous quarter. “While debt availability remains favorable, there are signs that some lenders are becoming more cautious,” analysts wrote last week, adding that “a rising percentage of banks are tightening credit standards, especially for construction and multifamily loans.”

But while traditional lenders stepped back, other lenders jumped in to carry the torch. Life companies and CMBS lenders in particular took a larger piece of the pie in non-agency lending activity.

Life companies accounted for 35 percent of lending volume tracked by CBRE up from 20 percent in the second quarter, while CMBS conduit lenders accounted for roughly 15 percent, an uptick from 10 percent in the second quarter.

CBRE also took a closer look at standards on closed loans during the last quarter and found that underwriting standards had tightened, with higher debt service coverage ratios and debt yields as well as fewer having interest-only terms.

As 2016 draws to a close, two issues are positioned to shape the direction of real estate capital markets, analysts noted. Firstly, investors should prepare for some short-term volatility following the anticipated Federal Reserve interest rate hike this month.

“Now that the election is over, investors are likely to focus on the Federal Reserve’s December policy meeting,” Brian Stoffers, the global president of debt and structured finance at CBRE Capital Markets, said.

The second issue is the degree to which CMBS origination capacity will meet the increasing refinance demand from CMBS loans maturing. “While there are promising signs that many originators will meet the requirements, there are concerns of increased loan pricing of 15 to 25 basis points and constrained debt availability,” analysts wrote.—C.C.