Each year, the Real Estate Board of New York selects six real estate professionals, be they specialists in residential or commercial sales or leasing, to bestow its Bernard H. Mendik Lifetime Leadership in Real Estate award; Young Real Estate Man of the Year award; Kenneth R. Gerrety Humanitarian award; Louis Smadbeck Broker Recognition award; Harry B. Helmsley Distinguished New Yorker award; and George M. Brooker Management Executive of the Year award.

Below, we honor this year’s honorees with a series of profiles and illustrations.

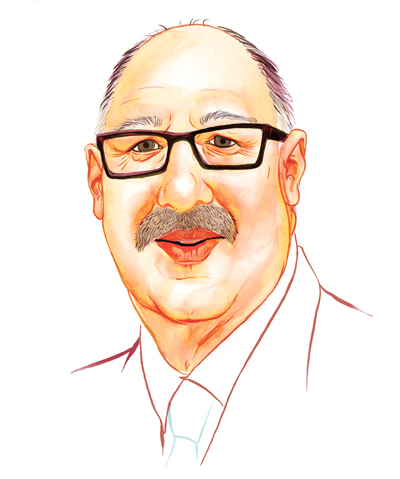

Some 50 years ago, Dick Concannon found himself in the engine room of a Midtown Manhattan office building.

Growing up in Merrick, N.Y., Mr. Concannon had always been mechanically inclined, able to take things apart and put them together. He’d attended Long Island University’s CW Post College “for a while” and needed a job, he said. Thanks to his father-in-law, who was a building superintendent, Mr. Concannon was at the core of a complex system that supplied heat, air-conditioning and power to a huge tower full of office workers.

“I thought I died and went to heaven,” he said.

In the five decades since, Mr. Concannon’s career has blossomed in ways he couldn’t have anticipated. He’s moved up the ranks at Rudin Management Co., where he’s been senior vice president of the operations department for the past 15 years. At Rudin, he’s been responsible for electrical, plumbing, HVAC and safety systems for 16 office buildings and 20 residential properties. In addition, he was administrator of environmental policy and remediation, served on the Rudin Energy Procurement Committee and even helped develop a pandemic-flu plan for the company’s employees.

Along the way, he’s become an expert in everything from asbestos removal to energy efficiency, and acted as an adviser to the Real Estate Board of New York on these subjects and myriad other management issues. Now, as he prepares to retire, he’s been named to receive the George M. Brooker Management Executive of the Year Award, which honors the memory of the first vice president of REBNY’s Management Division.

“Whenever we need someone to look at regulations, it was always Dick sitting at a table with us, giving his input,” REBNY President Steven Spinola said. “As a result, we have a better code today.

“He is respected tremendously by his colleagues,” and has been a “resource for us on every management issue,” Mr. Spinola added. “He had the judgment to not just learn from others, but implement new ideas.”

Over the years, Mr. Concannon has seen dramatic changes in building safety and efficiency standards and played a key role in implementing them.

Around the time he started, fire risk became a big issue for New York office buildings. Five people had been killed and 69 injured in blazes at two nearly completed office towers, prompting New York City Fire Commissioner John T. O’Hagan to push for the adoption of what would become Local Law 5 of 1973, then the toughest high-rise fire-safety law in the nation, according to The New York Times.

The law mandated a fire alarm and communication system for buildings higher than 100 feet and sprinklers for most centrally air-conditioned buildings, and it required that elevators be programmed to return to the ground floor in a fire. The law also said buildings had to have safety directors to advise tenants on what to do in the event of a fire, Mr. Concannon said.

“It was a very stringent fire safety plan, and it worked,” he said. “As building managers, we welcomed it. It gave us tools to work with. It made buildings safer.”

The 9/11 terrorist attack in 2001 was another watershed event for building managers.

Mr. Concannon learned of the looming disaster in a phone call from his right-hand man, Gene Boniberger, who was on the sidewalk outside Rudin’s building at 32 Avenue of the Americas when the first plane flew by on its way to the World Trade Center. When the second plane struck the complex, “we all knew what was going on,” Mr. Concannon said.

After an intense debate in the uncertain moments after the planes crashed, he decided it would be safer to keep workers inside rather than evacuate, a move that saved occupants of buildings nearby from exposure to the cloud of dust that spread through the area when the towers collapsed.

Expenses for security quadrupled after the attack, as Mr. Concannon installed turnstiles, security cameras and emergency food lockers and implemented training for security personnel. “After 9/11, I realized we should have a plan for non-fire emergencies,” Mr. Concannon said. He came up with a 40-page document outlining a building’s procedures and showing where its exits are. The plan, which preceded the city’s own 2006 non-fire emergency plan, amounts to a more useful “readers digest version”—in contrast, he said, to the inch-and-a-half-thick “door stops” that some buildings hand out.

Responding to concerns over potential blackouts during peak energy usage periods, Mr. Concannon and Mr. Boniberger came up with the Emergency Electrical Load Reduction Plan to curtail drains on the power grid through such steps as turning off perimeter lights and shutting down a quarter of a building’s elevators.

Last fall’s Hurricane Sandy is likely to bring about more changes for building managers, Mr. Concannon said, noting that the disaster came only 20 years after the last so-called 100-year storm hit the city.

“The comfort zone of the 100-year storm is gone,” he said. “We had flood prevention barricades, secured things and had elevator mechanics and glaziers on standby, but this storm was unprecedented.”

The real estate industry is “resilient,” and it is already responding by moving electrical switch gear and other critical systems out of basements and looking at ways to “harden buildings,” according to Mr. Concannon. The current code requiring oil tanks to be on bottom floors will probably have to be changed, he said.

Now 70 years old, Mr. Concannon said he is ready to make way for Mr. Boniberger’s promotion. “It’s time to step back and let somebody else take over,” he said. “I’ll always be available to the Rudins. They’re terrific.”

The feeling is mutual. “This award honors Dick for his accomplishments as a real estate professional, but, to us, he is practically a member of our family,” said Eric Rudin, president of Rudin Management.

“Everyone at our company, and all our tenants, have benefited in some way from his dedication, hard work and unwavering commitment to excellence over the years. I can’t think of a more deserving recipient for this award than Dick Concannon.” skleege@gmail.com

“I thought I died and went to heaven,” he said.

In the five decades since, Mr. Concannon’s career has blossomed in ways he couldn’t have anticipated. He’s moved up the ranks at Rudin Management Co., where he’s been senior vice president of the operations department for the past 15 years. At Rudin, he’s been responsible for electrical, plumbing, HVAC and safety systems for 16 office buildings and 20 residential properties. In addition, he was administrator of environmental policy and remediation, served on the Rudin Energy Procurement Committee and even helped develop a pandemic-flu plan for the company’s employees.

Along the way, he’s become an expert in everything from asbestos removal to energy efficiency, and acted as an adviser to the Real Estate Board of New York on these subjects and myriad other management issues. Now, as he prepares to retire, he’s been named to receive the George M. Brooker Management Executive of the Year Award, which honors the memory of the first vice president of REBNY’s Management Division.

“Whenever we need someone to look at regulations, it was always Dick sitting at a table with us, giving his input,” REBNY President Steven Spinola said. “As a result, we have a better code today.

“He is respected tremendously by his colleagues,” and has been a “resource for us on every management issue,” Mr. Spinola added. “He had the judgment to not just learn from others, but implement new ideas.”

Over the years, Mr. Concannon has seen dramatic changes in building safety and efficiency standards and played a key role in implementing them.

Around the time he started, fire risk became a big issue for New York office buildings. Five people had been killed and 69 injured in blazes at two nearly completed office towers, prompting New York City Fire Commissioner John T. O’Hagan to push for the adoption of what would become Local Law 5 of 1973, then the toughest high-rise fire-safety law in the nation, according to The New York Times.

The law mandated a fire alarm and communication system for buildings higher than 100 feet and sprinklers for most centrally air-conditioned buildings, and it required that elevators be programmed to return to the ground floor in a fire. The law also said buildings had to have safety directors to advise tenants on what to do in the event of a fire, Mr. Concannon said.

“It was a very stringent fire safety plan, and it worked,” he said. “As building managers, we welcomed it. It gave us tools to work with. It made buildings safer.”

The 9/11 terrorist attack in 2001 was another watershed event for building managers.

Mr. Concannon learned of the looming disaster in a phone call from his right-hand man, Gene Boniberger, who was on the sidewalk outside Rudin’s building at 32 Avenue of the Americas when the first plane flew by on its way to the World Trade Center. When the second plane struck the complex, “we all knew what was going on,” Mr. Concannon said.

After an intense debate in the uncertain moments after the planes crashed, he decided it would be safer to keep workers inside rather than evacuate, a move that saved occupants of buildings nearby from exposure to the cloud of dust that spread through the area when the towers collapsed.

Expenses for security quadrupled after the attack, as Mr. Concannon installed turnstiles, security cameras and emergency food lockers and implemented training for security personnel. “After 9/11, I realized we should have a plan for non-fire emergencies,” Mr. Concannon said. He came up with a 40-page document outlining a building’s procedures and showing where its exits are. The plan, which preceded the city’s own 2006 non-fire emergency plan, amounts to a more useful “readers digest version”—in contrast, he said, to the inch-and-a-half-thick “door stops” that some buildings hand out.

Responding to concerns over potential blackouts during peak energy usage periods, Mr. Concannon and Mr. Boniberger came up with the Emergency Electrical Load Reduction Plan to curtail drains on the power grid through such steps as turning off perimeter lights and shutting down a quarter of a building’s elevators.

Last fall’s Hurricane Sandy is likely to bring about more changes for building managers, Mr. Concannon said, noting that the disaster came only 20 years after the last so-called 100-year storm hit the city.

“The comfort zone of the 100-year storm is gone,” he said. “We had flood prevention barricades, secured things and had elevator mechanics and glaziers on standby, but this storm was unprecedented.”

The real estate industry is “resilient,” and it is already responding by moving electrical switch gear and other critical systems out of basements and looking at ways to “harden buildings,” according to Mr. Concannon. The current code requiring oil tanks to be on bottom floors will probably have to be changed, he said.

Now 70 years old, Mr. Concannon said he is ready to make way for Mr. Boniberger’s promotion. “It’s time to step back and let somebody else take over,” he said. “I’ll always be available to the Rudins. They’re terrific.”

The feeling is mutual. “This award honors Dick for his accomplishments as a real estate professional, but, to us, he is practically a member of our family,” said Eric Rudin, president of Rudin Management.

“Everyone at our company, and all our tenants, have benefited in some way from his dedication, hard work and unwavering commitment to excellence over the years. I can’t think of a more deserving recipient for this award than Dick Concannon.” skleege@gmail.com

Dottie Herman sprang into action in the aftermath of Hurricane Sandy.

Ms. Herman, the president and chief executive officer of Douglas Elliman, posted newspaper ads welcoming people to drop off supplies at the company’s offices or just come in to warm up and use the phones. Her “Eye on Real Estate” show on WOR radio—usually devoted to such subjects as estate taxes and financing—also focused on hurricane recovery.

“As I was giving information, people started giving money,” she said. “A man phoned in and donated helicopters!” Everyone in the company, which ranks as New York’s biggest residential brokerage and the fourth-largest in the nation by sales, helped in the hurricane efforts, she said. The response ranged from picking up and dropping off supplies to donating fuel and shelter. One landlord offered months of free rent to hurricane victims, she said, while another good Samaritan brought in some generators.

“We really just organized it,” she said. “So many people helped. It was unbelievable. It wasn’t a plan, it just happened.” The impulse to help was nothing new to Ms. Herman, this year’s recipient of the Real Estate Board of New York’s Kenneth R. Gerrety Humanitarian Award, which celebrates the memory of a REBNY executive vice president who provided valuable community service to his hometown of Garden City, N.Y.

“I’m very involved in a lot of things,” Ms. Herman said. “I don’t sit behind a desk. I’m a hands-on person. I believe at the end of the day you have to make a difference. You can’t change the world, but you can make a difference.” Ms. Herman began her career on Long Island, where she has been a contributor to the Sunrise Fund at Stony Brook University Medical Center, a program established to raise awareness and funds for pediatric oncology programs. She recalled being approached about 15 years ago by the head of oncology at the state-run hospital, which was looking to build a facility where family members could stay while their children were receiving treatment.

“I ended up getting involved. I got builders involved,” Ms. Herman said. “I met parents with little kids. I just reached out. I don’t know how you could not.”

Ms. Herman was also honored at the 12th Annual Heart of the Hamptons Gala in 2008, receiving the Distinguished Community Leadership Award for her continual support and contributions, and she is a longtime patron of the American Heart Association. The battle against heart disease, the biggest killer of women, “was personal to me,” she said.

“Most women have different symptoms from men,” she said. “I had symptoms many years ago and didn’t know it.”

When she went to the hospital with chest pains, she was initially told she was fine, Ms. Herman recalled. When the pains persisted, doctors advised her she might have acid reflux or an ulcer. It took a stress test to reveal the real cause.

“I was really in shock,” Ms. Herman said. “I ended up finding out I had a blocked artery. I’m lucky—I fought it. I could’ve not been lucky. I’m really big on making people aware,” she added. “If you’re aware, you don’t have to be sick.”

Ms. Herman has also supported the Tilles Center for the Performing Arts, the Southampton Hospital, the Katz Institute for Women’s Health and Katz Women’s Hospital located at North Shore University Hospital in Manhasset, and LIJ Medical Center in New Hyde Park.

In 2009, Ms. Herman received the Outstanding New Yorker Award from the Guardian Angels, with whom Ms. Herman said she shares a commitment to keeping the city safe.

Ms. Herman’s charitable impulses have been bolstered by her growing success in the New York area real estate market. She bought Prudential Long Island Realty in 1989 and Douglas Elliman, Manhattan’s largest brokerage firm, with her partner Howard Lorber in 2003.

Today, Douglas Elliman has over 3,800 real estate professionals and 675 employees working in more than 60 offices in Manhattan, Brooklyn, Queens, Long Island including the Hamptons and the North Fork, Westchester, and Riverdale. Ms. Herman also controls real estate services, including commercial and retail leasing and sales, relocation and settling-in services, and new development consulting. The business empire includes Manhattan’s largest residential property manager, Douglas Elliman Property Management, as well as DE Title and DE Capital Mortgage.

Ms. Herman says she’s grateful for the strength of the New York City residential real estate market, which wasn’t hit as hard as most areas by the 2008 financial crisis and has recovered faster.

“You should kiss the ground you walk on in New York City,” she said. “Because we got bruised; we didn’t get killed.”

While most of the U.S. housing market is still 30 percent below where it was before the crisis, New York City is “close to” recovery, Ms. Herman said. She credited Mayor Mike Bloomberg’s efforts to keep the city “safe, competitive and clean.”

The Manhattan housing market posted 2,598 sales over the last three months of 2012, the largest fourth-quarter total in at least 25 years, a Douglas Elliman report showed this month. The number of listings fell 34 percent from a year earlier to 4,749.

“We think that between rising rents and an improving economy and record mortgage rates, you’re going to see prices go up” in 2013, she said.

Price indicators for the fourth quarter were “mixed,” the report found, as the median sale price slipped 2 percent to $837,500 and the average rose 1 percent to almost $1.5 million.

Sales were driven by “looming changes to federal tax laws and general economic improvement,” the report said. Douglas Elliman had its best month ever in December, Ms. Herman said.

The Hamptons market has been “busy,” as people tried to sell properties to take advantage of capital gains or pass on properties to their children before the tax rates change.

“A lot of people” are investing in properties as rents rise in the resort area, she said. skleege@gmail.com

Ms. Herman, the president and chief executive officer of Douglas Elliman, posted newspaper ads welcoming people to drop off supplies at the company’s offices or just come in to warm up and use the phones. Her “Eye on Real Estate” show on WOR radio—usually devoted to such subjects as estate taxes and financing—also focused on hurricane recovery.

“As I was giving information, people started giving money,” she said. “A man phoned in and donated helicopters!” Everyone in the company, which ranks as New York’s biggest residential brokerage and the fourth-largest in the nation by sales, helped in the hurricane efforts, she said. The response ranged from picking up and dropping off supplies to donating fuel and shelter. One landlord offered months of free rent to hurricane victims, she said, while another good Samaritan brought in some generators.

“We really just organized it,” she said. “So many people helped. It was unbelievable. It wasn’t a plan, it just happened.” The impulse to help was nothing new to Ms. Herman, this year’s recipient of the Real Estate Board of New York’s Kenneth R. Gerrety Humanitarian Award, which celebrates the memory of a REBNY executive vice president who provided valuable community service to his hometown of Garden City, N.Y.

“I’m very involved in a lot of things,” Ms. Herman said. “I don’t sit behind a desk. I’m a hands-on person. I believe at the end of the day you have to make a difference. You can’t change the world, but you can make a difference.” Ms. Herman began her career on Long Island, where she has been a contributor to the Sunrise Fund at Stony Brook University Medical Center, a program established to raise awareness and funds for pediatric oncology programs. She recalled being approached about 15 years ago by the head of oncology at the state-run hospital, which was looking to build a facility where family members could stay while their children were receiving treatment.

“I ended up getting involved. I got builders involved,” Ms. Herman said. “I met parents with little kids. I just reached out. I don’t know how you could not.”

Ms. Herman was also honored at the 12th Annual Heart of the Hamptons Gala in 2008, receiving the Distinguished Community Leadership Award for her continual support and contributions, and she is a longtime patron of the American Heart Association. The battle against heart disease, the biggest killer of women, “was personal to me,” she said.

“Most women have different symptoms from men,” she said. “I had symptoms many years ago and didn’t know it.”

When she went to the hospital with chest pains, she was initially told she was fine, Ms. Herman recalled. When the pains persisted, doctors advised her she might have acid reflux or an ulcer. It took a stress test to reveal the real cause.

“I was really in shock,” Ms. Herman said. “I ended up finding out I had a blocked artery. I’m lucky—I fought it. I could’ve not been lucky. I’m really big on making people aware,” she added. “If you’re aware, you don’t have to be sick.”

Ms. Herman has also supported the Tilles Center for the Performing Arts, the Southampton Hospital, the Katz Institute for Women’s Health and Katz Women’s Hospital located at North Shore University Hospital in Manhasset, and LIJ Medical Center in New Hyde Park.

In 2009, Ms. Herman received the Outstanding New Yorker Award from the Guardian Angels, with whom Ms. Herman said she shares a commitment to keeping the city safe.

Ms. Herman’s charitable impulses have been bolstered by her growing success in the New York area real estate market. She bought Prudential Long Island Realty in 1989 and Douglas Elliman, Manhattan’s largest brokerage firm, with her partner Howard Lorber in 2003.

Today, Douglas Elliman has over 3,800 real estate professionals and 675 employees working in more than 60 offices in Manhattan, Brooklyn, Queens, Long Island including the Hamptons and the North Fork, Westchester, and Riverdale. Ms. Herman also controls real estate services, including commercial and retail leasing and sales, relocation and settling-in services, and new development consulting. The business empire includes Manhattan’s largest residential property manager, Douglas Elliman Property Management, as well as DE Title and DE Capital Mortgage.

Ms. Herman says she’s grateful for the strength of the New York City residential real estate market, which wasn’t hit as hard as most areas by the 2008 financial crisis and has recovered faster.

“You should kiss the ground you walk on in New York City,” she said. “Because we got bruised; we didn’t get killed.”

While most of the U.S. housing market is still 30 percent below where it was before the crisis, New York City is “close to” recovery, Ms. Herman said. She credited Mayor Mike Bloomberg’s efforts to keep the city “safe, competitive and clean.”

The Manhattan housing market posted 2,598 sales over the last three months of 2012, the largest fourth-quarter total in at least 25 years, a Douglas Elliman report showed this month. The number of listings fell 34 percent from a year earlier to 4,749.

“We think that between rising rents and an improving economy and record mortgage rates, you’re going to see prices go up” in 2013, she said.

Price indicators for the fourth quarter were “mixed,” the report found, as the median sale price slipped 2 percent to $837,500 and the average rose 1 percent to almost $1.5 million.

Sales were driven by “looming changes to federal tax laws and general economic improvement,” the report said. Douglas Elliman had its best month ever in December, Ms. Herman said.

The Hamptons market has been “busy,” as people tried to sell properties to take advantage of capital gains or pass on properties to their children before the tax rates change.

“A lot of people” are investing in properties as rents rise in the resort area, she said. skleege@gmail.com

Contract negotiations between local 32BJ of the Service Employees International Union and New York’s residential landlords couldn’t have come at a worse time for Mike Fishman, the local president.

In 2008, following the worst financial crisis since the Great Depression, revenue was falling for the owners of the some 4,000 apartment buildings where the union’s members were employed as doormen, superintendents and maintenance workers.

At the same time, actuaries were saying that the cost of providing health insurance was about to skyrocket. Mr. Fishman would have to hammer out a pact to replace a contract that had been negotiated during the boom—one that had included “relatively generous” wage increases, according to Howard Rothschild, president of the Realty Advisory Board on Labor Relations, who was on the other side of the negotiations.

“We presented the data, saying, ‘if you want an increase in wages, it may not be there,’” Mr. Rothschild recalled. “Mike stepped back and said, ‘What if we could save you a certain amount of money off health insurance?’”

That led to the formation of a health care committee, composed of union and industry representatives, with a mission of cutting $70 million a year from costs. The effort paid off with even greater savings—an average of $90 million a year—as insurance contracts were put out to bid and a wellness program was instituted. The savings were the key to a new contract in 2010 for the apartment workers and made it easier to negotiate a deal between the union and the city’s commercial property owners in 2011.

“Mike Fishman not only understands labor, and not only understands the needs of his members, but also he understands the needs of the industry,” Mr. Rothschild said. “He’s the type of person that not only can think outside the box but also can think of ways of slightly changing the box so a deal can ultimately be concluded.”

Mr. Fishman, now the international executive vice president of Washington-based SEIU, is receiving the Harry B. Helmsley Distinguished New Yorker Award from the Real Estate Board of New York. The honor comes as states like Michigan, Ohio and Wisconsin—where Mr. Fishman got his start as a union leader—enact right-to-work laws and other policies to limit unions’ clout in negotiations with government and industry.

“New York is still a place where unions play a valuable role in maintaining a city that works for everyone,” said Mr. Fishman, who maintains that the anti-union efforts in other states are worsening poverty and weakening schools. “That’s not the kind of country we want to live in.”

He said he welcomes the recognition from the real estate organization.

“We are a balance in the industry. We help maintain good jobs; we also help maintain good development,” Mr. Fishman said. “It’s not always an easy relationship. We have those things we agree to work on together, those things we agree to disagree on and those things we need to fight each other on, but we keep talking. Fundamentally, we have an understanding that we are each a part of the fabric of New York.

“I’m honored to be the recipient of this award, and the first labor person to get it,” Mr. Fishman said. “It’s a sign of respect for the people who work in the industry. I think the country could learn something from New York and the relationships we’ve built.”

Mr. Fishman lived in Queens until he was 6 years old, when his family moved to Connecticut. His father was an electrical worker and union member who went back to school, got a degree and became a community college teacher. Mr. Fishman learned the trade that eventually led to his union career from his grandfather, who was a storefront carpenter in Brooklyn.

“I was working on a job as carpenter in Wisconsin,” he said. “We built wood-frame houses. The local needed someone to organize the non-union crews.”

Mr. Fishman spent the next 20 years with the carpenters’ union, becoming a national organizer. He joined SEIU in 1996 as assistant to the president and then chief of staff. He was elected four times as president of Local 32BJ and led organizing drives that more than doubled membership. SEIU 32BJ is the largest private-sector union in New York State and the largest property services union in the country, with 120,000 members in eight states and the District of Columbia.

The local initially consisted mostly of New York elevator operators, at a time when the city’s lifts were “considered the largest transportation system in the world, even though it was vertical,” Mr. Fishman said.

Today the largest division is the commercial group, representing 60,000 office building cleaners. The residential division consists of about 30,000 workers, and the school division represents 10,000 cleaners, building engineers, maintenance workers, bus drivers, aides and food service employees. The security division has grown to 15,000 private security officers from 1,000 just a decade ago.

The union also has a division representing theaters and stadiums and one representing window cleaners. The last round of bargaining with commercial landlords, in 2011, was “difficult,” but the union was able to strike “a deal that was good for both sides,” Mr. Fishman said. The union also formed a committee to find ways of cooperating with the industry.

Common interests including supporting affordable housing and making sure the landmarks commission doesn’t “get overzealous,” he said. Union members have come out to support controversial projects like the Barclays Center in Brooklyn and the St. Vincent’s Hospital redevelopment.

Mr. Fishman said he’s been less involved in New York issues since taking his position with the national union, though Hurricane Sandy focused his attention on the need to “make sure people are taken care of and we have good development” as the area recovers.

For the past two years, Mr. Fishman said, he’s been working on ways to encourage investment in infrastructure by pension funds. Gov. Andrew Cuomo is “very much in favor of it,” Mr. Fishman said. “Hurricane Sandy gave us more incentive.” skleege@gmail.com

In 2008, following the worst financial crisis since the Great Depression, revenue was falling for the owners of the some 4,000 apartment buildings where the union’s members were employed as doormen, superintendents and maintenance workers.

At the same time, actuaries were saying that the cost of providing health insurance was about to skyrocket. Mr. Fishman would have to hammer out a pact to replace a contract that had been negotiated during the boom—one that had included “relatively generous” wage increases, according to Howard Rothschild, president of the Realty Advisory Board on Labor Relations, who was on the other side of the negotiations.

“We presented the data, saying, ‘if you want an increase in wages, it may not be there,’” Mr. Rothschild recalled. “Mike stepped back and said, ‘What if we could save you a certain amount of money off health insurance?’”

That led to the formation of a health care committee, composed of union and industry representatives, with a mission of cutting $70 million a year from costs. The effort paid off with even greater savings—an average of $90 million a year—as insurance contracts were put out to bid and a wellness program was instituted. The savings were the key to a new contract in 2010 for the apartment workers and made it easier to negotiate a deal between the union and the city’s commercial property owners in 2011.

“Mike Fishman not only understands labor, and not only understands the needs of his members, but also he understands the needs of the industry,” Mr. Rothschild said. “He’s the type of person that not only can think outside the box but also can think of ways of slightly changing the box so a deal can ultimately be concluded.”

Mr. Fishman, now the international executive vice president of Washington-based SEIU, is receiving the Harry B. Helmsley Distinguished New Yorker Award from the Real Estate Board of New York. The honor comes as states like Michigan, Ohio and Wisconsin—where Mr. Fishman got his start as a union leader—enact right-to-work laws and other policies to limit unions’ clout in negotiations with government and industry.

“New York is still a place where unions play a valuable role in maintaining a city that works for everyone,” said Mr. Fishman, who maintains that the anti-union efforts in other states are worsening poverty and weakening schools. “That’s not the kind of country we want to live in.”

He said he welcomes the recognition from the real estate organization.

“We are a balance in the industry. We help maintain good jobs; we also help maintain good development,” Mr. Fishman said. “It’s not always an easy relationship. We have those things we agree to work on together, those things we agree to disagree on and those things we need to fight each other on, but we keep talking. Fundamentally, we have an understanding that we are each a part of the fabric of New York.

“I’m honored to be the recipient of this award, and the first labor person to get it,” Mr. Fishman said. “It’s a sign of respect for the people who work in the industry. I think the country could learn something from New York and the relationships we’ve built.”

Mr. Fishman lived in Queens until he was 6 years old, when his family moved to Connecticut. His father was an electrical worker and union member who went back to school, got a degree and became a community college teacher. Mr. Fishman learned the trade that eventually led to his union career from his grandfather, who was a storefront carpenter in Brooklyn.

“I was working on a job as carpenter in Wisconsin,” he said. “We built wood-frame houses. The local needed someone to organize the non-union crews.”

Mr. Fishman spent the next 20 years with the carpenters’ union, becoming a national organizer. He joined SEIU in 1996 as assistant to the president and then chief of staff. He was elected four times as president of Local 32BJ and led organizing drives that more than doubled membership. SEIU 32BJ is the largest private-sector union in New York State and the largest property services union in the country, with 120,000 members in eight states and the District of Columbia.

The local initially consisted mostly of New York elevator operators, at a time when the city’s lifts were “considered the largest transportation system in the world, even though it was vertical,” Mr. Fishman said.

Today the largest division is the commercial group, representing 60,000 office building cleaners. The residential division consists of about 30,000 workers, and the school division represents 10,000 cleaners, building engineers, maintenance workers, bus drivers, aides and food service employees. The security division has grown to 15,000 private security officers from 1,000 just a decade ago.

The union also has a division representing theaters and stadiums and one representing window cleaners. The last round of bargaining with commercial landlords, in 2011, was “difficult,” but the union was able to strike “a deal that was good for both sides,” Mr. Fishman said. The union also formed a committee to find ways of cooperating with the industry.

Common interests including supporting affordable housing and making sure the landmarks commission doesn’t “get overzealous,” he said. Union members have come out to support controversial projects like the Barclays Center in Brooklyn and the St. Vincent’s Hospital redevelopment.

Mr. Fishman said he’s been less involved in New York issues since taking his position with the national union, though Hurricane Sandy focused his attention on the need to “make sure people are taken care of and we have good development” as the area recovers.

For the past two years, Mr. Fishman said, he’s been working on ways to encourage investment in infrastructure by pension funds. Gov. Andrew Cuomo is “very much in favor of it,” Mr. Fishman said. “Hurricane Sandy gave us more incentive.” skleege@gmail.com

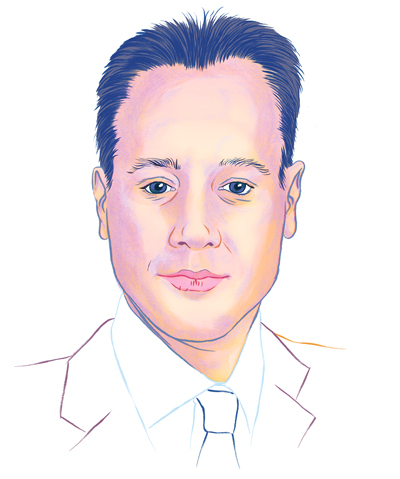

A client recently asked Woody Heller whether he thought one of the potential risks to the New York real estate investment market was what happens, or doesn’t, in Washington, D.C.

Mr. Heller, executive managing director at Studley, said the risk is less than some people think.

“Given the fact that Manhattan attracts international capital, despite the disorder in Washington, the U.S., and Manhattan in particular, continue to compare favorably on a global basis” he said in an interview. “The single greatest element that impacts prices is capital flows. Capital flows for Manhattan will continue to be strong for the next several years. The ongoing imbalance between those who desire to buy and the properties available for purchase continues to suggest that pricing will remain strong and probably continue to increase in the foreseeable future.”

Mr. Heller, who has closed more than $6.5 billion of asset and note sale transactions comprising about 33 million square feet, is a two-time winner of the Real Estate Board of New York’s Most Ingenious Deal of the Year award. And this week, he’ll be receiving the Louis Smadbeck Broker Recognition Award from the group. He is a governor at REBNY and chairman of the sales broker committee.

A New York native, Mr. Heller started his career at Jones Lang Wooton (later Jones Lang LaSalle), where he counted Paul Pariser and Charles Bendit among his early mentors. Both are now at Taconic Investment Partners.

Mr. Heller worked his way up from an entry-level position as an analyst to handling investment sale activities in New York City, before joining Studley in 2003. He’s known for having engineered the sales of the Citigroup Center and the Rhinelander Mansion, leased to Polo Ralph Lauren, and the purchase of the Drake Hotel development site.

He has also structured mortgages, equity joint ventures and note sales, including the sale of the notes and mortgage on the Chrysler Building. In 2007, he won the Most Ingenious Deal of the Year award for the sale of the New York Law School development site in Tribeca, a transaction that closed in 2006. Mr. Heller received the same honor in 2004 for the sale of McGraw Hill’s 45 percent C-corporation interest in 1221 Avenue of the Americas the previous year.

“For some reason, complicated deals seem to find me,” Mr. Heller told The Commercial Observer in 2010.

Even with uncertainty over the presidential election and the shadow being cast on the economy by the so-called fiscal cliff, Mr. Heller said the past year has been active in his four areas of focus, with deals closing on office, residential and retail properties and a transaction about to be completed on a development site.

Among the residential deals was the sale of 111 Kent Avenue in Brooklyn, which he said set a record price per square foot in New York outside of Manhattan. The buyer, American Realty Advisors, paid $55.5 million, or more than $895,000 for each of the 62 apartments in the Williamsburg building, a price The New York Times called “stunning even in a hot market.”

The Times attributed the boom in the market for Brooklyn rental apartment properties to low interest rates, rising rents and difficulty of obtaining mortgages to buy apartments. Studley represented Stellar Management in the sale. Mr. Heller said buyers of Brooklyn rental apartments are confident in their ability to keep buildings filled.

“We think Brooklyn is a happening spot,” Mr. Heller said. “It’s geographically proximate, and transportation in and out of Manhattan is good. The neighborhoods are interesting; many are still low-rise and have not been overdeveloped.”

Some Brooklyn neighborhoods have the feel of a Tribeca or a Soho, a quality that is increasingly hard to find in Manhattan, he said. One of the pleasures of Brooklyn life is taking the ferry to Manhattan, he said, tracing Studley’s interest in the borough to his partner, Will Silverman, who lives in Brooklyn Heights.

“It used to be Brooklyn was a price-alternative location,” Mr. Heller said. “We no longer think of it that way. Now people live there as a lifestyle choice.”

Mr. Heller also handled the city’s biggest residential deal of the year, selling the Madison Belvedere, a rental property located at 10 East 29th Street in Manhattan, for $300 million to Invesco. Studley represented Rose Associates, which had developed the 50-story residential tower, one of the tallest newly constructed multifamily assets in the borough, in 1998.

On the office side, Mr. Heller sold the Rose family’s half interest in 1 Battery Park Plaza in lower Manhattan for $80 million, giving the Rudin family full ownership. The 885,645-square-foot office tower, built in 1970, was virtually fully leased at the time of the sale.

Studley also completed a sale of a 12-story office building at 31 West 27th Street in Chelsea for $65 million. Some observers had speculated that the seller, Sharif El-Gamal, overpaid when he bought the property for $45.7 million in 2009. The buyer was Walnut Hill Group.

In a recent Studley deal, American Realty Capital New York Recovery REIT purchased 256 West 38th Street for $48.6 million on Dec. 26. The seller—a joint venture of East End Capital and GreenOak Real Estate—had bought the property in 2011 for about $30 million.

Acting as the sole broker, Studley sold the retail condominiums at 465 Broadway to Savanna for $57 million. The sale by GLL Real Estate Partners was financed with a $42 million acquisition loan from Mesa West Capital and equity from Savanna Real Estate Fund II.

In another retail-related deal, JPMorgan Chase & Co. paid $87.5 million for an eight-story building at 525 Broadway, where a profitable branch is located.

REBNY President Steven Spinola said the Louis Smadbeck Award signifies the esteem in which Mr. Heller is held by his peers.

“Woody is the kind of person who wakes up in the morning and thinks real estate, understands economics and knows the market inside out,” Mr. Spinola said. “It means he has the total respect of the commercial division here.”

Mr. Heller serves as a member of the Young Men’s/Women’s Real Estate Association, the National Realty Conference, the Royal Institution of Chartered Surveyors and the Real Estate Lenders Association. skleege@gmail.com

Mr. Heller, executive managing director at Studley, said the risk is less than some people think.

“Given the fact that Manhattan attracts international capital, despite the disorder in Washington, the U.S., and Manhattan in particular, continue to compare favorably on a global basis” he said in an interview. “The single greatest element that impacts prices is capital flows. Capital flows for Manhattan will continue to be strong for the next several years. The ongoing imbalance between those who desire to buy and the properties available for purchase continues to suggest that pricing will remain strong and probably continue to increase in the foreseeable future.”

Mr. Heller, who has closed more than $6.5 billion of asset and note sale transactions comprising about 33 million square feet, is a two-time winner of the Real Estate Board of New York’s Most Ingenious Deal of the Year award. And this week, he’ll be receiving the Louis Smadbeck Broker Recognition Award from the group. He is a governor at REBNY and chairman of the sales broker committee.

A New York native, Mr. Heller started his career at Jones Lang Wooton (later Jones Lang LaSalle), where he counted Paul Pariser and Charles Bendit among his early mentors. Both are now at Taconic Investment Partners.

Mr. Heller worked his way up from an entry-level position as an analyst to handling investment sale activities in New York City, before joining Studley in 2003. He’s known for having engineered the sales of the Citigroup Center and the Rhinelander Mansion, leased to Polo Ralph Lauren, and the purchase of the Drake Hotel development site.

He has also structured mortgages, equity joint ventures and note sales, including the sale of the notes and mortgage on the Chrysler Building. In 2007, he won the Most Ingenious Deal of the Year award for the sale of the New York Law School development site in Tribeca, a transaction that closed in 2006. Mr. Heller received the same honor in 2004 for the sale of McGraw Hill’s 45 percent C-corporation interest in 1221 Avenue of the Americas the previous year.

“For some reason, complicated deals seem to find me,” Mr. Heller told The Commercial Observer in 2010.

Even with uncertainty over the presidential election and the shadow being cast on the economy by the so-called fiscal cliff, Mr. Heller said the past year has been active in his four areas of focus, with deals closing on office, residential and retail properties and a transaction about to be completed on a development site.

Among the residential deals was the sale of 111 Kent Avenue in Brooklyn, which he said set a record price per square foot in New York outside of Manhattan. The buyer, American Realty Advisors, paid $55.5 million, or more than $895,000 for each of the 62 apartments in the Williamsburg building, a price The New York Times called “stunning even in a hot market.”

The Times attributed the boom in the market for Brooklyn rental apartment properties to low interest rates, rising rents and difficulty of obtaining mortgages to buy apartments. Studley represented Stellar Management in the sale. Mr. Heller said buyers of Brooklyn rental apartments are confident in their ability to keep buildings filled.

“We think Brooklyn is a happening spot,” Mr. Heller said. “It’s geographically proximate, and transportation in and out of Manhattan is good. The neighborhoods are interesting; many are still low-rise and have not been overdeveloped.”

Some Brooklyn neighborhoods have the feel of a Tribeca or a Soho, a quality that is increasingly hard to find in Manhattan, he said. One of the pleasures of Brooklyn life is taking the ferry to Manhattan, he said, tracing Studley’s interest in the borough to his partner, Will Silverman, who lives in Brooklyn Heights.

“It used to be Brooklyn was a price-alternative location,” Mr. Heller said. “We no longer think of it that way. Now people live there as a lifestyle choice.”

Mr. Heller also handled the city’s biggest residential deal of the year, selling the Madison Belvedere, a rental property located at 10 East 29th Street in Manhattan, for $300 million to Invesco. Studley represented Rose Associates, which had developed the 50-story residential tower, one of the tallest newly constructed multifamily assets in the borough, in 1998.

On the office side, Mr. Heller sold the Rose family’s half interest in 1 Battery Park Plaza in lower Manhattan for $80 million, giving the Rudin family full ownership. The 885,645-square-foot office tower, built in 1970, was virtually fully leased at the time of the sale.

Studley also completed a sale of a 12-story office building at 31 West 27th Street in Chelsea for $65 million. Some observers had speculated that the seller, Sharif El-Gamal, overpaid when he bought the property for $45.7 million in 2009. The buyer was Walnut Hill Group.

In a recent Studley deal, American Realty Capital New York Recovery REIT purchased 256 West 38th Street for $48.6 million on Dec. 26. The seller—a joint venture of East End Capital and GreenOak Real Estate—had bought the property in 2011 for about $30 million.

Acting as the sole broker, Studley sold the retail condominiums at 465 Broadway to Savanna for $57 million. The sale by GLL Real Estate Partners was financed with a $42 million acquisition loan from Mesa West Capital and equity from Savanna Real Estate Fund II.

In another retail-related deal, JPMorgan Chase & Co. paid $87.5 million for an eight-story building at 525 Broadway, where a profitable branch is located.

REBNY President Steven Spinola said the Louis Smadbeck Award signifies the esteem in which Mr. Heller is held by his peers.

“Woody is the kind of person who wakes up in the morning and thinks real estate, understands economics and knows the market inside out,” Mr. Spinola said. “It means he has the total respect of the commercial division here.”

Mr. Heller serves as a member of the Young Men’s/Women’s Real Estate Association, the National Realty Conference, the Royal Institution of Chartered Surveyors and the Real Estate Lenders Association. skleege@gmail.com

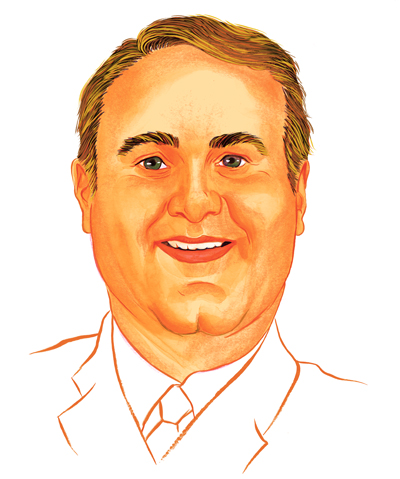

When William Montana started in the real estate business, he could be seen circulating through the offices of what was then Newmark & Co., pen and notebook in hand.

“I’ve had lots of mentors throughout the years,” Mr. Montana said. “I would sit with every senior broker or professional there. People were very generous with their time and advice.”

In the almost 25 years since, Mr. Montana, who is now a managing director at Studley and the chairman of the real Estate Board of New York’s commercial brokerage division, has displayed the same generosity toward aspiring real estate professionals and city residents in general.

As past president and chairman emeritus of the Young Men’s/Women’s Real Estate Association of New York, he’s helped mentor students in real estate programs at Baruch College, New York University and Columbia University, built housing with Habitat for Humanity and raised money for New York Cares, among other charities.

He was selected by the young men and women’s group, an offshoot of REBNY, to receive the Young Real Estate Man of the Year Award, given on the basis of integrity, professionalism and personal ethics. Mr. Montana, 48 (the cut off for the award is 50), is an enthusiastic advocate of real estate as a career, in part because it is a field where one can be productive until late in life. His grandfather, Bill Montana, was a commercial broker who completed his last deal at age 84.

Mr. Montana grew up in a real estate family. His grandfather, a commercial real estate broker, practiced in Westchester, and his grandmother, Theresa, was a residential broker in the area. His father Ronald, is a periodontist who has invested in numerous real estate ventures, while his stepfather, Ed Zibro, is a commercial real estate broker in Florida.

An avid skier, Mr. Montana attended college at the University of Colorado at Boulder, where he studied interpersonal communications and economics. He said it was always in his mind that he would return to New York to continue in the footsteps of his forebears.

“Real estate is a great career for a young person because there’s so many facets,” he said. “It’s a great industry because you can evolve what you do. Leasing, sales, development, construction, design, finance—there’s so many ways to plug into this industry and evolve.”

He’d noticed that almost all successful people “at some point would gravitate toward investing in real estate,” Mr. Montana said. “I just thought, ‘why not start out there?’”

Mr. Montana had contemplated getting into the development side of the business, but companies weren’t hiring in the aftermath of the stock market crash of 1987, and so he started as a leasing broker at Newmark (now Newmark Grubb Knight Frank). He was then recruited by Edward S. Gordon Co., where he spent four years.

“ESG was a very hungry, aggressive firm at the time,” he recalls. “They were looking to really professionalize the industry—as Studley has done and taken to an even higher level.”

He joined Studley in 1996 after being recruited by two friends at the firm, David Goldstein and Matt Barlow, both now directors. Since then, Mr. Montana has cut deals on more than a million square feet of space, representing an array of clients that range from law firms, technology companies and insurance companies to nonprofit organizations, call centers and biotechnology companies.

Mr. Montana describes his role as “advising companies and other organizations on how to make very good, well-informed real estate decisions.”

One recent “kickoff meeting” with a nonprofit company that is looking for new space illustrates his approach, he said.

The session was attended by 10 people, including Mr. Montana, the project manager and people in different roles at the company, such as the chief financial officer, the head of facilities, the chief executive officer and the head of human resources. Mr. Montana posed “a lot of probing questions” about what each of them would need and want in a new space.

“The answers they’ll provide will give us unique criteria by which to judge all the alternatives in the marketplace,” he said. “A good process yields great results.” Mr. Montana’s job is made easier by the “desirable product” he has to sell in New York City. He credits the city government’s efforts to combat crime and create a more diverse economy under Mayors Rudy Giuliani and Michael Bloomberg.

“It started with Giuliani,” Mr. Montana said. “He made the city safe and clean. When you’ve got a safe and clean city, people want to live and work here, tourists want to visit, and great things happen when those things exist.”

Mayor Bloomberg has worked to attract universities, including the planned Cornell University technology graduate school campus on Roosevelt Island. The effort “will pay dividends for decades to come,” Mr. Montana said. The city’s plan to rezone the area around Grand Central Station to allow the construction of modern buildings around the transportation hub is a “smart thing to do,” he added.

“On a long-term basis, we need to provide modern buildings for the large international firms that we need to house,” Mr. Montana said. Currently, New York’s building stock “is very old compared to other international cities.”

Gridlock in the nation’s capital remains a concern.

“The divisiveness that exists in Washington right now has been paralyzing,” he said, adding that solutions exist if legislators can find the political will. “They need to put the interests of the U.S. ahead of their careers and make brave decisions.”

Tax and regulatory issues are especially important to the banks, insurance companies and funds that continue to be a key component of the New York commercial real estate market.

“The financial services industry is still in a holding pattern, because the regulatory landscape is uncertain,” Mr. Montana said. “Once the ground rules have been set, it’s my opinion that financial services firms will quickly figure out how to operate and will hire people again. When that happens, you’re going to see the market get much tighter in terms of availability.” skleege@gmail.com

“I’ve had lots of mentors throughout the years,” Mr. Montana said. “I would sit with every senior broker or professional there. People were very generous with their time and advice.”

In the almost 25 years since, Mr. Montana, who is now a managing director at Studley and the chairman of the real Estate Board of New York’s commercial brokerage division, has displayed the same generosity toward aspiring real estate professionals and city residents in general.

As past president and chairman emeritus of the Young Men’s/Women’s Real Estate Association of New York, he’s helped mentor students in real estate programs at Baruch College, New York University and Columbia University, built housing with Habitat for Humanity and raised money for New York Cares, among other charities.

He was selected by the young men and women’s group, an offshoot of REBNY, to receive the Young Real Estate Man of the Year Award, given on the basis of integrity, professionalism and personal ethics. Mr. Montana, 48 (the cut off for the award is 50), is an enthusiastic advocate of real estate as a career, in part because it is a field where one can be productive until late in life. His grandfather, Bill Montana, was a commercial broker who completed his last deal at age 84.

Mr. Montana grew up in a real estate family. His grandfather, a commercial real estate broker, practiced in Westchester, and his grandmother, Theresa, was a residential broker in the area. His father Ronald, is a periodontist who has invested in numerous real estate ventures, while his stepfather, Ed Zibro, is a commercial real estate broker in Florida.

An avid skier, Mr. Montana attended college at the University of Colorado at Boulder, where he studied interpersonal communications and economics. He said it was always in his mind that he would return to New York to continue in the footsteps of his forebears.

“Real estate is a great career for a young person because there’s so many facets,” he said. “It’s a great industry because you can evolve what you do. Leasing, sales, development, construction, design, finance—there’s so many ways to plug into this industry and evolve.”

He’d noticed that almost all successful people “at some point would gravitate toward investing in real estate,” Mr. Montana said. “I just thought, ‘why not start out there?’”

Mr. Montana had contemplated getting into the development side of the business, but companies weren’t hiring in the aftermath of the stock market crash of 1987, and so he started as a leasing broker at Newmark (now Newmark Grubb Knight Frank). He was then recruited by Edward S. Gordon Co., where he spent four years.

“ESG was a very hungry, aggressive firm at the time,” he recalls. “They were looking to really professionalize the industry—as Studley has done and taken to an even higher level.”

He joined Studley in 1996 after being recruited by two friends at the firm, David Goldstein and Matt Barlow, both now directors. Since then, Mr. Montana has cut deals on more than a million square feet of space, representing an array of clients that range from law firms, technology companies and insurance companies to nonprofit organizations, call centers and biotechnology companies.

Mr. Montana describes his role as “advising companies and other organizations on how to make very good, well-informed real estate decisions.”

One recent “kickoff meeting” with a nonprofit company that is looking for new space illustrates his approach, he said.

The session was attended by 10 people, including Mr. Montana, the project manager and people in different roles at the company, such as the chief financial officer, the head of facilities, the chief executive officer and the head of human resources. Mr. Montana posed “a lot of probing questions” about what each of them would need and want in a new space.

“The answers they’ll provide will give us unique criteria by which to judge all the alternatives in the marketplace,” he said. “A good process yields great results.” Mr. Montana’s job is made easier by the “desirable product” he has to sell in New York City. He credits the city government’s efforts to combat crime and create a more diverse economy under Mayors Rudy Giuliani and Michael Bloomberg.

“It started with Giuliani,” Mr. Montana said. “He made the city safe and clean. When you’ve got a safe and clean city, people want to live and work here, tourists want to visit, and great things happen when those things exist.”

Mayor Bloomberg has worked to attract universities, including the planned Cornell University technology graduate school campus on Roosevelt Island. The effort “will pay dividends for decades to come,” Mr. Montana said. The city’s plan to rezone the area around Grand Central Station to allow the construction of modern buildings around the transportation hub is a “smart thing to do,” he added.

“On a long-term basis, we need to provide modern buildings for the large international firms that we need to house,” Mr. Montana said. Currently, New York’s building stock “is very old compared to other international cities.”

Gridlock in the nation’s capital remains a concern.

“The divisiveness that exists in Washington right now has been paralyzing,” he said, adding that solutions exist if legislators can find the political will. “They need to put the interests of the U.S. ahead of their careers and make brave decisions.”

Tax and regulatory issues are especially important to the banks, insurance companies and funds that continue to be a key component of the New York commercial real estate market.

“The financial services industry is still in a holding pattern, because the regulatory landscape is uncertain,” Mr. Montana said. “Once the ground rules have been set, it’s my opinion that financial services firms will quickly figure out how to operate and will hire people again. When that happens, you’re going to see the market get much tighter in terms of availability.” skleege@gmail.com

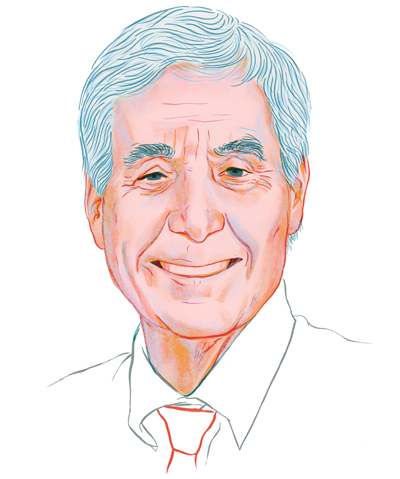

Donald Zucker, who’s never invested in office properties before or since, made one exception—but only because it involved Bernard H. Mendik.

In that transaction, which was many years ago, Mr. Zucker says he took a small partnership interest in the purchase of an East Side office building by his friend, who died in 2001.This year, Mr. Zucker says, he’s especially gratified to accept the Bernard H. Mendik Lifetime Leadership in Real Estate Award.

“He was one of the sweetest people that ever lived—a wonderful guy in every way,” Mr. Zucker said. “It was a pleasure to say ‘yes’ to receive this reward, because his name is on it.”

Mr. Zucker, who specializes in residential lending and development, is being recognized for his exceptional accomplishment in the profession and his lifetime of leadership in New York real estate, including his service in the city government under Mayors Ed Koch and Rudy Giuliani.

As a member of the executive committee of the Real Estate Board of New York, “He’s been a total supporter of everything we’ve done in the past decade plus,” said Steven Spinola, president of the group. “When you say, ‘Who can you get to provide support for this, whatever it may be?’ Donald Zucker is always at the top of the list.”

Mr. Zucker grew up in Brooklyn, where he attended Lincoln High School. He went on to study banking and finance at New York University and worked briefly at H. Hentz & Co., a Bernard Baruch firm, before being called to serve his country in the U.S. Army from 1953 to 1955. He returned to a job at Pearce Mayer & Greer, then the city’s No. 1 real estate office in sales.

“They hired me as a beginner to be part of a new mortgage department,” Mr. Zucker recalled. He made “$25 a week against future commissions.”

After “three years well spent,” he went to work for Jack Halperin of J. Halperin & Co., which was known for doing the mortgage work for the suburban developer Levitt & Sons and was active in Federal Housing Administration development in New York at the time.

He started Donald Zucker Company, a real estate mortgage firm, in 1961, and built his first apartment project, a 20-story, 177-unit building on West 12th Street, in 1963. Fifty years later, he expressed amazement that he could get the deal done “with no partner and no such thing as a second mortgage.”

Since then, Mr. Zucker has brought more than 4,000 apartments to the Manhattan market. He controls a construction/development company, a national mortgage brokerage firm and an asset management company and employs about 300 people.

In 1986, he took a full-time post as adviser on construction to Mayor Ed Koch, helping with everything from renovating police headquarters to building jails and homeless housing.

“I was a big fan of Ed Koch. I tried to help in any shape, manner or form I could,” Mr. Zucker said. “It was the best three years of my life. I hope that I made a difference.”

The city had about $2 billion under construction with nobody overseeing the work, Mr. Zucker said.

“I convinced them to put on far more supervision,” he said. “In the private sector, you wouldn’t think of building without full-time supervision,” whereas the city’s supervisors were responsible for two or three projects at once.

“It was impossible,” Mr. Zucker recalled. “I got them to change that. At the end, it was a very beneficial thing.”

Mr. Zucker, a Democrat, also served as chairman of the School Construction Authority for Mayor Rudy Giuliani, after some holdovers from the Koch administration recommended him.

“I did the same thing there that I did with the city,” Mr. Zucker said of his service in school construction. “I insisted on more supervision, but consistent supervision. Some of the school projects were huge.”

As Mr. Zucker focused on working for the city, he turned day-to-day control of his company over to his wife, Barbara Hrbek Zucker, and their daughter Laurie Zucker Lederman, who is still involved in the business.

“My wife, of course, is my perennial adviser,” he said. “I believe in women’s intuition.”

Mr. Zucker credits REBNY for providing the industry with a more effective voice.

“Everything that goes on in the real estate world—tax abatement programs for construction, relationships with the buildings department, what’s going on in the zoning world—every aspect is something that the real estate board gets involved in,” he said.

The biggest change he’s seen in his five decades in the business is the evolution of the city, especially Manhattan, into “the icon of the world,” Mr. Zucker said.

“The whole world wants to be here,” he said. “Between the institutions, the museums, Lincoln Center, we are a very desirable city in this world. Our real estate has become just as desirable.”

He credits Mayor Guiliani’s efforts to curb crime for expanding the area that’s suitable for development.

“I used to say when I started in this business, if I can walk to it in Manhattan, I can build it,” Mr. Zucker said. “Then I did the marathon in 1987 and said, if I can run to it, I can build it.”

About 15 years ago, Mr. Zucker started a project on Second Street between Avenues C and D. “People thought I was crazy,” he said. Today, he said, there is no neighborhood of Manhattan that’s considered off-limits.

Mr. Zucker said he expects to focus more on condominium projects.

“I can’t see a future for me as a rental housing developer right now,” he said. “It’s very difficult to get a site to build on.”

Among his current projects is Love Lane Mews, a group of former garage buildings in a secluded area of Brooklyn Heights that have been transformed into two townhouses and 38 luxury condominium units. The townhouses were quickly sold for $5 million, he said, and there are only five condo units left. skleege@obsever.com

In that transaction, which was many years ago, Mr. Zucker says he took a small partnership interest in the purchase of an East Side office building by his friend, who died in 2001.This year, Mr. Zucker says, he’s especially gratified to accept the Bernard H. Mendik Lifetime Leadership in Real Estate Award.

“He was one of the sweetest people that ever lived—a wonderful guy in every way,” Mr. Zucker said. “It was a pleasure to say ‘yes’ to receive this reward, because his name is on it.”

Mr. Zucker, who specializes in residential lending and development, is being recognized for his exceptional accomplishment in the profession and his lifetime of leadership in New York real estate, including his service in the city government under Mayors Ed Koch and Rudy Giuliani.

As a member of the executive committee of the Real Estate Board of New York, “He’s been a total supporter of everything we’ve done in the past decade plus,” said Steven Spinola, president of the group. “When you say, ‘Who can you get to provide support for this, whatever it may be?’ Donald Zucker is always at the top of the list.”

Mr. Zucker grew up in Brooklyn, where he attended Lincoln High School. He went on to study banking and finance at New York University and worked briefly at H. Hentz & Co., a Bernard Baruch firm, before being called to serve his country in the U.S. Army from 1953 to 1955. He returned to a job at Pearce Mayer & Greer, then the city’s No. 1 real estate office in sales.

“They hired me as a beginner to be part of a new mortgage department,” Mr. Zucker recalled. He made “$25 a week against future commissions.”

After “three years well spent,” he went to work for Jack Halperin of J. Halperin & Co., which was known for doing the mortgage work for the suburban developer Levitt & Sons and was active in Federal Housing Administration development in New York at the time.

He started Donald Zucker Company, a real estate mortgage firm, in 1961, and built his first apartment project, a 20-story, 177-unit building on West 12th Street, in 1963. Fifty years later, he expressed amazement that he could get the deal done “with no partner and no such thing as a second mortgage.”

Since then, Mr. Zucker has brought more than 4,000 apartments to the Manhattan market. He controls a construction/development company, a national mortgage brokerage firm and an asset management company and employs about 300 people.

In 1986, he took a full-time post as adviser on construction to Mayor Ed Koch, helping with everything from renovating police headquarters to building jails and homeless housing.

“I was a big fan of Ed Koch. I tried to help in any shape, manner or form I could,” Mr. Zucker said. “It was the best three years of my life. I hope that I made a difference.”

The city had about $2 billion under construction with nobody overseeing the work, Mr. Zucker said.

“I convinced them to put on far more supervision,” he said. “In the private sector, you wouldn’t think of building without full-time supervision,” whereas the city’s supervisors were responsible for two or three projects at once.

“It was impossible,” Mr. Zucker recalled. “I got them to change that. At the end, it was a very beneficial thing.”

Mr. Zucker, a Democrat, also served as chairman of the School Construction Authority for Mayor Rudy Giuliani, after some holdovers from the Koch administration recommended him.

“I did the same thing there that I did with the city,” Mr. Zucker said of his service in school construction. “I insisted on more supervision, but consistent supervision. Some of the school projects were huge.”

As Mr. Zucker focused on working for the city, he turned day-to-day control of his company over to his wife, Barbara Hrbek Zucker, and their daughter Laurie Zucker Lederman, who is still involved in the business.

“My wife, of course, is my perennial adviser,” he said. “I believe in women’s intuition.”

Mr. Zucker credits REBNY for providing the industry with a more effective voice.

“Everything that goes on in the real estate world—tax abatement programs for construction, relationships with the buildings department, what’s going on in the zoning world—every aspect is something that the real estate board gets involved in,” he said.

The biggest change he’s seen in his five decades in the business is the evolution of the city, especially Manhattan, into “the icon of the world,” Mr. Zucker said.

“The whole world wants to be here,” he said. “Between the institutions, the museums, Lincoln Center, we are a very desirable city in this world. Our real estate has become just as desirable.”

He credits Mayor Guiliani’s efforts to curb crime for expanding the area that’s suitable for development.

“I used to say when I started in this business, if I can walk to it in Manhattan, I can build it,” Mr. Zucker said. “Then I did the marathon in 1987 and said, if I can run to it, I can build it.”

About 15 years ago, Mr. Zucker started a project on Second Street between Avenues C and D. “People thought I was crazy,” he said. Today, he said, there is no neighborhood of Manhattan that’s considered off-limits.

Mr. Zucker said he expects to focus more on condominium projects.

“I can’t see a future for me as a rental housing developer right now,” he said. “It’s very difficult to get a site to build on.”

Among his current projects is Love Lane Mews, a group of former garage buildings in a secluded area of Brooklyn Heights that have been transformed into two townhouses and 38 luxury condominium units. The townhouses were quickly sold for $5 million, he said, and there are only five condo units left. skleege@obsever.com