The 50 Most Important Figures of Commercial Real Estate Finance

By The Editors April 2, 2019 8:00 am

reprints

The skyscrapers of New York City and all of America’s greatest cities are monuments to the power of the real estate industry that builds them.

But—as the titans who rank among the most powerful players in real estate finance know better than anyone—even the lowliest strip mall couldn’t rise from the ground without a lender ready to put dollars on the line. Thus, as ever, the landscape of commercial real estate finance in 2018 was chock full of its own monuments.

Take Blackstone’s $1.8 billion whole loan to jumpstart construction on one of the most important new office building projects in New York City: Tishman Speyer’s The Spiral at the recently opened Hudson Yards campus. Or Bank OZK’s $558 million financing package for The Estates at Acqualina in Sunny Isles Beach, Fla.—the largest condominium construction loan in Miami-Dade County this business cycle. Or Deutsche Bank’s $630 million construction loan in Los Angeles for Related Companies’ Frank Gehry–designed $1 billion mixed-use project, The Grand.

Each of these projects has the potential to make a bold mark on a premier American city. And pure real estate finance prowess made them all possible.

Recognizing achievements like these is what our annual Power 50 list is all about. It’s our chance to highlight the work of some of the industry’s boldest, sharpest and most creative minds. All three of those aforementioned lenders soared to new heights on our list this year. We offer a well-deserved tip of the cap to them.

But entrusting developers with ungodly sums of money isn’t the only way our honorees proved their mettle in 2018. As usual, an impressive crop of savvy, unrelenting finance brokers demonstrated their crucial role in steering the flow of capital.

This year, Newmark Knight Frank’s Dustin Stolly and Jordan Roeschlaub vaulted to the top spot among debt advisers with a remarkable expansion of their share. The duo, having done $6.5 billion of business in 2017, arranged $11.8 billion worth of debt deals last year, an 82 percent increase. When a small team of 12 flashes that kind of influence nationally, it proves size hardly matters.

On the other hand, if our jobs were to compare brokers to one another, we’d be working 24/7. Add lenders into the mix and . . . well, that’s when the honorees start showing up in our editors’ sleep (literally).

This year’s list grew with the arrival of some well-deserving new faces. Foremost among those was LoanCore Capital, a platform with major international backing that seems to have a finger in every pie, from floating-rate balance sheet debt to the red-hot world of collateralized loan obligations. Not far behind was Mesa West, a debt fund recently acquired by Morgan Stanley that lent $3.2 billion last year across state lines and asset classes. CapitalSource, a Beverly Hills, Calif.-based group that dabbles in the market’s thorniest products, construction and value-add bridge loans, is also worthy of a shout-out for its $2.4 billion in lending accomplished in 2018.

December’s uncertainty created some tremors that threatened a grand finale to this cycle that won’t seem to quit. The gradual tightening of the Fed’s reins quickly became a distant memory at the end of the year as volatility spooked the central bank into pledging a wait-and-see approach. But even that minor blip was a reminder of how just two dozen basis points can make or break a deal. As borrowers waited for the dust to settle, deal flow temporarily sputtered to a halt before the New Year.

This year has been brighter, and anyway, a bit of strife isn’t enough to intimidate the industry’s heaviest hitters. For one thing, our Power 50 warriors wouldn’t be featured in the following pages if they hadn’t earned their stripes in past cycles. For another, each figure earned a spot here via a reputation for excellent judgment. That means sensing which deals not to pursue as much as it means knowing when to break out the sharp elbows.

The Commercial Observer Power Gala held in Midtown Manhattan each June isn’t the only party these superstars of finance get an invite to. Every day, they’re front and center at one of the greatest shows the world of business has to offer where risks are often rewarded, where NDAs aren’t always honored and where mistakes can be ruinous. But in no other arena is the reward for hard work so tangible: money in their pockets and edifices that stand for centuries.—Cathy Cunningham, Mack Burke, Matt Grossman and Larry Getlen.

1. Michael Nash, Stephen Plavin, Jonathan Pollack and Tim Johnson

Co-Founder and Chairman of Blackstone Real Estate Debt Strategies; CEO of Blackstone Mortgage Trust; Global Head of Blackstone Real Estate Debt Strategies; Senior Managing Director at Blackstone Real Estate Debt Strategies

Last Year’s Rank: 2

The throngs of banks, debt funds, insurers and even landlords clamoring to issue debt against commercial real estate have never been broader or more diverse. But when Tishman Speyer went looking for single-source construction funding to build one of the most important commercial buildings currently underway in Manhattan, Hudson Yards’ The Spiral, there was only one lender it could dial up.

Last April, Blackstone came through with a massive $1.8 billion whole loan to fund the project through its real estate investment trust lending arm, Blackstone Mortgage Trust. How many real estate financiers could even dream of turning a deal like that?

“It was a good example of a transaction with significant scale, where we were the only true one-stop solution for Tishman Speyer,” said Tim Johnson. “In construction, there’s a lot of action after you close the loan. Asset management is one of our key strengths.”

Emphasis on “one of.”

At the risk of stating the obvious, the company’s seemingly endless access to capital and its dizzying global reach have consistently powered it towards ever more impressive heights as a real estate lender.

“[Last year] was the most productive year on the lending side that we’ve had,” Jonathan Pollack crowed. “We did deals on both coasts of the U.S., in Europe and in Australia in 2018. We’re able to cover the entire globe.”

In doing so, the New York City-based firm lent nearly $14 billion last year between its mortgage trust and real estate debt strategies businesses—a giant step above its $9.1 billion tally in 2017. And since 2016, Blackstone’s lending volume has notched 107 percent growth—an extraordinary two-year trajectory over a period when the industry has never been more competitive.

Still, the firm insists it’s not hiding any strategic cards up its sleeves. A focus on the good old fundamentals drives each of its deals, according to Blackstone’s leadership.

“We look for large transactions in the best-performing markets,” Pollack said. “As a lender, we always want to be supporting the best clients—because they’ll execute.”

Last year, that meant a heavy focus on the Far West Side of Manhattan. In addition to its Hudson Yards loan, Blackstone led the $650 million acquisition financing on Terminal Stores, L&L Holding Company and Normandy Real Estate Partners’ project to turn a former warehouse on 11th Avenue between West 27th and West 28th Streets into a chic retail hall.

The famously tight-lipped Blackstone ensemble was mum on any big plans for how it will shake up the industry in 2019. But here are two promises you can take to the bank: The company will remain on the cutting edge of the industry’s most creative debt strategies, and any comer will need to bring a special brand of virtuosity to challenge Blackstone’s reign.—Matt Grossman

2. Jeff DiModica and Dennis Schuh

President; Chief Originations Officer at Starwood Property Trust

Last Year’s Rank: 4

When it comes to what sets Starwood Property Trust apart from other non-bank commercial real estate lenders, sheer size and firepower are the Connecticut-based mortgage real estate investment trust’s most obvious endowments. In 2018, its core originations business put about $9 billion into the market—up from $7.5 billion a year earlier. And more than half of last year’s volume came from the deals Starwood says it’s best at: large loans on complex properties and portfolios. That work counted for $6 billion of its new debt last year, better than a 50 percent increase over the previous year’s level.

But in the view of Jeff DiModica, the biggest difference-maker for Starwood is its access to capital.

“We’re the only ones out there who used the high-yield market,” DiModica said, referring to the firm’s penchant for issuing affordable unsecured bonds for its lending. As of the end of 2018, the company had about $2 billion in bonds outstanding, and Moody’s hinted it was considering upgrading the company’s credit rating, which would reduce its borrowing costs further yet.

Combine that with the more than $8.6 billion the company enjoys in secured credit and you see why few competitors can match Starwood.

“We’ve methodically built a multi-cylinder engine that allows us to pivot to the highest relative value investments, borrow more efficiently and earn more [than other lenders] on the same deals,” DiModica gloated.

Starwood also proved in spades last year that it’s not afraid of getting its hands dirty with operating-business assets or the complexities of ground-up development. One of the biggest of such deals was a $375 million package—which included both senior debt and a mezzanine loan—on a 10-asset national hospitality portfolio owned by Urban Commons. Construction didn’t scare off Starwood either: It lent $213 million to the developers behind a giant new multifamily project under development by Cabot, Cabot & Forbes and Blue Vista in Brighton, Mass., on Boston’s outskirts. Projects like that might intimidate lesser lenders—but they merely whet Starwood’s appetite, according to Dennis Schuh.

“We rarely compete with smaller debt funds,” Schuh said. “We’d rather use our equity DNA to focus on larger, more complex deals.”—M.G.

3. Brian Baker and Al Brooks

Global Head of Commercial Mortgages at J.P. Morgan Securities; Head of J.P. Morgan Chase Commercial Real Estate

Last Year’s Rank: 3

For 2019’s Power 50 list, Commercial Observer consolidated some company spots. As such, No. 3 packs an especially powerful punch with the head of J.P. Morgan Chase commercial real estate and the global head of J.P. Morgan securities teaming up to represent the bank’s commercial real estate lending power in its totality.

It’s a duo few can compete with.

L.A.-based Al Brooks oversees a $100 billion loan portfolio. His dynamic team—which includes real estate banking business co-heads Chad Tredway and Priscilla Almodovar, as well as Alice Carr, the head of community development banking and Ed Ely, head of commercial term lending—was responsible for $24 billion in originations last year.

“It’s not a booming market, but what’s shocking to me is how consistent business has been and also the lack of noise we’ve experienced,” Brooks said.

At the same time, “we’re not pushing growth for the sake of growth; we just don’t do that. We continue to serve our customers and we do what we need to do to be competitive,” he added.

Notable transactions last year included a $495 million construction loan for Howard Hughes Corp.’s construction of 110 North Wacker Drive in Chicago and a $707 million financing for TF Cornerstone’s Hunters Point South in Long Island City, Queens. The latter deal included an affordable housing component, a key focus for Brooks’ group. The bank has been busy using all the tools available, including long-term LIHTC sources and new markets tax credit programs.

J.P. Morgan takes pride in providing a “frictionless experience” for its myriad borrowers, Brooks said, and has made strides in shortening its deal closing times. In 2018, roughly 50 percent of its deals were closed in under 30 days.

New York-based Brian Baker, meanwhile, racked up a hefty $16 billion in loans last year.

“2018 was a good year for us,” Baker said. “It got a little competitive, but we got to a very good place in terms of revenue and originations.”

Any competition quickly thinned out around the $100 million mark, Baker said, with the traditional lenders leading the charge for loans larger than $250 million.

J.P. Morgan Securities was the No.1 loan contributor for conduit and Single-Asset Single-Borrower CMBS, with notable CMBS deals led by the team including the $1.75 billion financing of Aventura Mall, a 2.2-million-square-foot super-regional mall in Aventura, Fla.; the $1 billion financing of a 300+ La Quinta national hotel portfolio; and the $678 million financing of AON Center, an 83-story, 2.8-million-square-foot trophy office tower in Chicago.

Then there was the bank’s $613.6 million construction financing for CIM Group and LivWrk’s 1.2-million-square-foot mixed-use project at 85 Jay Street in Dumbo, Brooklyn; a $327.9 million financing for CIM Group’s conversion of the Tribune Tower in Chicago into a residential project; and a $380 million financing for Tishman Speyer’s development of 11 Hoyt Street in Downtown Brooklyn.

Oh, and did we mention the bank is the No.1 underwriter of CLOs?

“The scale of J.P. Morgan allows us to be a one-stop shop for our clients, supporting their needs with a variety of solutions. That’s how we differentiate ourselves relative to our competition,” Baker said.—Cathy Cunningham

4. Doug Mazer, Kara McShane and Alan Wiener

Head of Real Estate Capital Markets; Head of Commercial Real Estate Capital Markets and Finance; Group Head of Multifamily at Wells Fargo

Last Year’s Rank: 1

As one of the country’s most consistent and omnipresent institutional real estate lenders, Wells Fargo continued to roll right along last year, combining massive commercial-lending balance sheet and securitization businesses with one of the country’s most active agency-sponsored multifamily lending shops. Though a year dominated top to bottom by debt funds saw the San Francisco bank cede its No. 1 rank from 2018, it should be no surprise the bank once again earned a showing near the very top of the standings.

When Alan Wiener sums it up by stating, “Wells is a huge real estate bank,” he knows of what he speaks. His team, for instance, was the top Fannie Mae lender nationwide last year, and lent $14.5 billion overall to owners of apartment complexes. That number includes some of the biggest New York City deals of 2018, including a $501 million loan for Rockpoint Group and Brooksville Company’s acquisition of Brooklyn’s Starrett City and a $407 million financing on The Durst Organization’s Via 57 West.

Shiny as they may be, those local transactions barely dent the surface of the bank’s national multifamily presence.

“Only about 10 or 15 percent of our multifamily work is in New York,” Wiener said.

Meanwhile, the bank’s commercial lending and securitization businesses, led by Doug Mazer and Kara McShane, turned in another eye-popping performance. Its capital markets group lent $10 billion last year, with another $16.8 billion in facility closings, upsizes, modifications and renewals. And in a down year for CMBS, Wells’ work as an issuer shined through. The bank launched 89 transactions worth $70.8 billion, including $51.6 billion it offered to the market as the lead or co-lead.

As benchmark interest rates have wobbled unpredictably this year and last, Mazer said that the key to maintaining lending volume is to lend an ear proactively to clients’ needs and concerns.

“What we’re really trying to do is to service our customers, and make sure we’re providing the most competitive terms,” he explained.

Already, he said, the new year is looking like the market has found steadier ground.

“It certainly looks like the pipeline is a lot more robust. We’re back off to the races.” —M.G.

5. Matt Borstein

Global Head of Commercial Real Estate at Deutsche Bank

Last Year’s Rank: 8

Not all the attention that Deutsche Bank garnered in the last year was positive (at least not concerning the bank’s private lending arm’s past business with the Trump Organization and the fact that the New York Attorney General’s office subpoenaed Deutsche’s banking records), but from a strictly commercial real estate point of view, there’s not much to complain about. Deutsche Bank originated $10.1 billion in CMBS loans in 2018—up from $9.95 billion in 2017—split between $7.9 billion in large loans and $2.3 billion in conduit loans. Its total balance sheet lending for the year, however, totaled $12.1 billion. And that’s even with the departure in April of Ed Adler, the bank’s head of U.S. originations.

Highlights from the bank’s significant 2018 work? A $463 million loan to developer Savanna to facilitate the $640 million purchase of 5 Bryant Park from Blackstone Group in May; a $750 million debt package for Harry Macklowe to finance construction of One Wall Street’s conversion from office to residential; and an $800 million financing for Silverstein Properties.

In November, Deutsche also provided $630 million in construction financing to Related Companies for The Grand, Related’s $1 billion, Frank Gehry-designed mixed-use development in Downtown Los Angeles.

As Commercial Observer reported, the Time Warner Center will be renamed the Deutsche Bank Center, thanks to Deutsche Bank leasing 1.1 million square feet of office space in the center, incorporating all of the building’s available office space save for the 20th floor. Deutsche is expected to move into the complex from its current home at 60 Wall Street in the third quarter of 2021.

Oh, and did anyone mention that there’s been talk of a merger with Commerzbank? Well, yes, the two institutions have been in formal talks, even if a deal is not definite.

Deutsche hit the ground running in 2019, with deals including $89.1 million to Jay Street Associates in January, backed by the 32-story office tower at 330 Jay Street in Brooklyn, and the following month, a $40 million CMBS loan to refinance the AC by Marriott Tucson Downtown in Tucson, Ariz.—Larry Getlen

6. James Flaum

Global Head of Commercial Real Estate Lending at Morgan Stanley

Last Year’s Rank: 6

In a market racked with uncertainty, Morgan Stanley remains steady as one of the most powerful banking institutions on this Power 50 list.

It churned out $18 billion in debt originations across its platforms in 2018, up from $16 billion in 2017—and which marked a 14 percent jump from 2016.

In the U.S. CMBS realm, Morgan Stanley ranked sixth among bookrunners last year with just over $7.5 billion securitized across 20 deals, representing a nearly 10 percent market share, although down from its $9.6 billion figure last year. The bank rounded out its 2018 total, logging a bank market total of $10.5 billion.

“[Our numbers] are consistent with previous years,” James Flaum said. “We’re typically running 10 to 20 originations annually and the split is usually 40 percent securitization; 40 percent bank and the other 20 percent toggles based on which markets are most effective for us. The bank market was most effective last year and the year before that it was securitization.”

Flaum said the banking behemoth’s lending tendencies remain in markets where “people live, work and play, in top cities and in state capitals in the U.S.” He said its focus is on “well-capped borrowers with skin in the game…on high-quality real estate, where there’s equity at risk.”

The bank market and loan syndication market proved more competitive for Morgan Stanley than the CMBS market last year, in general, Flaum said. While competition in this realm is “fierce” and mostly reserved for the industry’s heaviest hitters, Flaum shrugged off any notion that the shop can’t hold its own.

“It’s nothing we’re not used to,” he said. “We’re pretty consistent in these markets, so it was extremely competitive, but not unusually competitive. As soon as the market eases up [many players will] jump back in.”

The bank did approximately $4 billion in business in New York last year, including teaming up with New York Community Bank to provide a $900 million refinance of RXR Realty’s iconic Starrett-Lehigh Building. In the deal, $150 million was structured as a facility earn out, triggered by a new tenant signing a lease.

As for 2019, Flaum pointed to the Treasury’s rally since December and the tightening of spreads possibly causing an acceleration in refinances ahead of any possible downturn.

“It’s rare that you get tightening spreads and a rally in the treasury,” Flaum said. “[Historically, that could mean we’re nearing] a recession, and when that settles in people may get nervous.”

Despite popular recession talks, and without any indication that the cause could originate from the real estate market, don’t expect Morgan Stanley to flinch.—Mack Burke

7. David Bouton and Joseph Dyckman

Co-Heads of U.S. CMBS at Citigroup

Last Year’s Rank: 7

Seventeen billion dollars of real estate originations across conduit CMBS, SASB CMBS, syndications and warehouse lending: How do you like them apples?

In addition to leading the three largest SASB transactions in 2018, Citigroup priced 37 CMBS deals and ranked high on the league tables, as the No.4 CMBS bookrunner and loan contributor, the No. 4 agency CMBS bookrunner and No. 2 in conduit loan contributions.

“We think our success shows in the league tables, and we think we did the right deals,” David Bouton said.

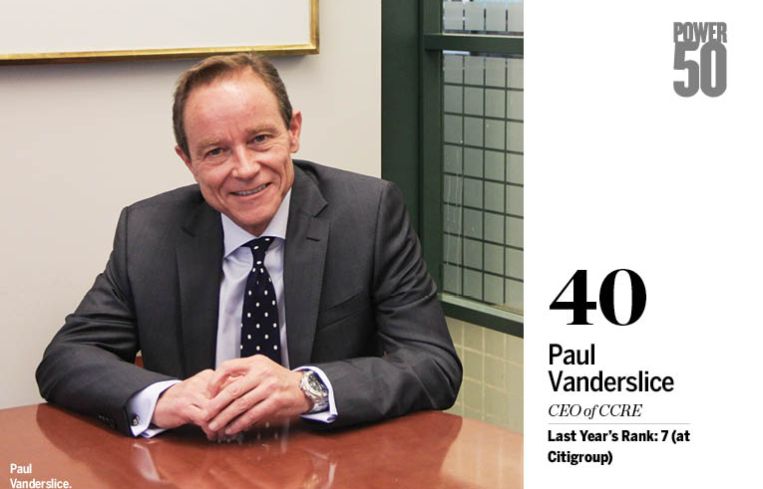

The CMBS co-heads stood strong, despite the departure of Paul Vanderslice in April for CCRE (he has since been replaced by Raul Orozco, a 10-year veteran of Citi’s CMBS group.)

Citi’s notable 2018 transactions included the $5 billion debt financing package for Blackstone’s $7.6 billion go-private of Gramercy Property Trust, the largest structured real estate transaction in 2018 and one of the largest since the financial crisis.

“It was complicated and it was large,” Bouton said. “We accessed different markets, we did a $3 billion floating-rate SASB, which was eight times oversubscribed, and we tightened pricing from guidance. We also did a $1.5 billion syndicated mortgage and mezzanine loan and kept $500 million on balance sheet, so we put a lot of capital into it.”

Citi also executed a $1.85 billion SASB financing for Brookfield Asset Management’s Atlantis Paradise Island in the Bahamas as well as a $1.9 billion SASB refinance of Blackstone’s BioMed Realty Trust, a portfolio of 27 properties.

In New York, the bank provided a $480 million loan to RFR, Kushner Companies and LIVWRK’s Dumbo Heights project in Brooklyn. The debt refinanced an existing bridge loan, also provided by Citi.

The bank’s average deal size grew in 2018, and its prowess for highly structured and complicated deals drew the sponsors as well as positioning it well for M&A deals where certainty, size and expertise are paramount.

In terms of M&A activity, “it was the year of some really big trades,” Joseph Dyckman said. In addition to the Gramercy Property Trust deal, Citi also participated in the financing of Brookfield’s acquisition of Forest City Realty Trust. The bank was the only lender to lead and participate in each of the transaction’s eight tranches.

Last year’s momentum has carried over into 2019 with Citi as sole bookrunner on the first CMBS transaction of 2019, a $830 million SASB deal for StorageMart across the U.S.

“We’ll continue to hustle,” Bouton said.—C.C.

8. George Gleason, Richard Smith, Brannon Hamblen and Greg Newman

Chairman and CEO; Managing Director of Originations in Northeast U.S.; President and COO of the Real Estate Specialties Group; Managing Director of Originations in Southeast U.S. at Bank OZK

Last Year’s Rank: 17

We don’t call them Bank of the O-yeah for nothing.

Despite increased competition, 2018 was another successful year for Bank OZK, with the lender selectively taking down some of the market’s largest development loans.

Widely considered the industry’s preeminent construction lender, Bank OZK racked up a cool $6 billion in originations last year. And unlike so many of its peers, the bank doesn’t sell loans down or syndicate debt, but instead holds every single loan on its balance sheet.

“We continue to maintain our discipline of low-leverage transactions with quality borrowers and quality real estate,” Richard Smith said. “If that brings higher transaction volume then great, but if it means less volume that’s fine also as we will continue to maintain our core disciplines.”

Notable deals include the $251 million construction loan for RAL Companies, Vanke U.S. and Oliver’s Realty Group’s Pier 6 luxury residential development at Brooklyn Bridge Park; a $275 million loan for Tishman Speyer’s 1.1-million-square-foot Jacx office property in Long Island City, Queens; and a $558 million construction loan for Trump Group’s The Estates at Acqualina in Sunny Isles Beach, Fla. The latter marks the largest construction loan in Miami-Dade County this real estate cycle.

A stock drop in October appeared to be a tempest in a teacup, with the stock rebounding quickly thereafter, and Bank OZK kicked off 2019 with a bang, closing a $350 million acquisition and renovation loan for GFI Capital Resources Group and Elliott Management’s purchase and transformation of the Parker New York hotel. Bank OZK executed the term sheet in mid-December 2018 and closed the transaction within four weeks.

“Our borrower profile has evolved over the years,” Smith said. “Today we target top-tier borrowers and marquee properties in prime locations, and we’ll continue to target that business.”

Case in point, in late March the lender made a $475 million construction loan on JDL Development and Wanxiang America Real Estate Group’s One Chicago Square development in the windy city.—C.C.

9. Richard Mack and Peter Sotoloff

Co-Founder and CEO; CIO and Managing Partner at Mack Real Estate Credit Strategies

Last Year’s Rank: 29

Increasing your originations from $4 billion to $6 billion? I guess that makes you the Mack Daddy.

“It was a record year for the platform and we were running on all cylinders,” Peter Sotoloff said. “When we look at our competitors, we were probably in the top two or three most productive alternative lenders. A lot of people talk about the competition, but we were able to find very interesting opportunities at very compelling credit metrics.”

Of Mack Real Estate Credit Strategies’ total 2018 lending volume, roughly 50 percent comprised refinances, 30 percent was construction debt and 20 percent was acquisition financing. Its average loan size topped $200 million, with roughly 50 percent of deal volume in New York, and the rest scattered around major markets including Washington, D.C., and Philadelphia.

One example is Mack’s $380 million construction loan for Penzance’s The Highlands mixed-use project in Rosslyn, Va., in September—planned before the announcement of Amazon’s HQ2 in nearby Crystal City.

“Even pre-HQ2, the project is in an excellent location with not a lot of new supply,” Sotoloff said. “This transaction showed our creativity in providing solutions. Many of our competitors competed for this deal but we were able to win because we understood the borrower’s business plan and we were very creative in terms of providing a favorable structure.”

And in the City of Brotherly Love, Mack provided Post Brothers with a $178 million loan for the recapitalization of Piazza at Schmidt’s Commons, an 11-building multifamily portfolio in the Northern Liberties neighborhood.

Then there was the $210 million refinance for Brookfield Asset Management’s Brill Building in Times Square. The direct deal closed within three weeks and—despite the market being pretty squirrely in December—Mack was able to hold all terms and deliver.

Yet another notable transaction was Mack’s $503 million refinance of three of Al Rayyan Tourism Investment Company’s hotel properties: the Manhattan Times Square Hotel in New York, the St. Regis Washington, D.C., and the St. Regis Bal Harbour in Miami.

“We’re not trying to be everything to everyone,” Sotoloff said. Instead, Mack focuses on high-quality assets in high barrier-to-entry markets with strong, repeat sponsorship.

“Our reputation speaks for itself; we’ve created a one-of-a-kind franchise,” he said. “We have people who—once they see the experience with us and how efficient we are—generally want to go direct to us for all of their other needs. It’s really a testament to how we do business in terms of underwriting, creativity and speed, in addition to having an attractive cost and structure.”

Mack’s forward pipeline of roughly $4 billion says it all.—C.C.

10. Warren de Haan, Boyd Fellows, Chris Tokarski and Stew Ward

Managing Partners at ACORE Capital

Last Year’s Rank: 9

It may be a lender-eat-lender world out there. But last year, one of the debt-fund world’s brightest stars managed to put more capital into the market than ever before.

ACORE Capital upped its volume by nearly 15 percent, bringing $5.7 billion in new debt to the market, compared with an even $5 billion in 2017. Not bad for a firm that’s a month away from celebrating just its fourth anniversary.

The young firm’s impressive lending statistics come from a hunger to get as broad a picture of the national market as possible, its leaders say.

“We strive to see every deal possible across the entire U.S.A., and in all property types that fit our investment parameters,” Warren de Haan said. “When we execute this strategy well, we wind up winning a diversified portfolio both geographically as well as with respect to property type.”

What’s more, ACORE’s accomplishments came despite a rough end to the year for U.S. financial markets, a period that Boyd Fellows said bent—but didn’t break—a long bull market’s resolve.

“The volatility in the fourth quarter created challenges for many of our clients, particularly on new acquisitions,” Fellows recalled. “But it also gave us the opportunity to stand out as a lender our clients can absolutely count on, even when the market creates uncertainty.”

Borrowers indeed counted on ACORE in droves last year to finance some of the country’s most interesting and complex development and repositioning deals. In October, the platform was responsible for a $169.8 million loan against a sprawling portfolio of industrial, office and retail properties controlled by Alto Real Estate Funds and Northstar Commercial Partners—a deal that combined both senior and mezzanine debt.

And in a deal at the start of 2018, ACORE teamed with LaSalle Investment Management to lead a $105 million bridge loan on a freshly built condominium and apartment tower in Nashville: 505 Church Street, the city’s tallest residential building.

A real estate-first approach is one of the firm’s biggest strengths, de Haan affirmed.

“We continue to grow our asset management team, a key client service differentiator when dealing with complex, transitional loans,” he said.—M.G.

11. Jeff Fastov

Senior Managing Director, Credit Strategies at Square Mile Capital Management

Last Year’s Rank: 18

“We’re kind of the old guard at this point,” said Jeff Fastov, considering his shop’s pedigree among a growing horde of new debt lenders.

The firm—which delivers first mortgages, mezzanine loans and preferred equity—added another billion to last year’s origination total, bringing its volume to $4.5 billion in 2018, benefitting from the reputation it established early on in the debt fund game.

“I think what we saw was an ever-increasing share of repeat business, which is gratifying,” Fastov said. “We can efficiently do follow-on business on negotiated terms, which produces a better term for us because we spend more time executing transactions and responding to borrowers we know as opposed to chasing new accounts. Our whole business, now, is more efficient and more profitable.”

Fastov pointed to a $172 million loan backed by a mixed-use project in Cleveland as one that best represented the firm’s tastes and capabilities. The floating-rate financing replaced debt from the construction of Pinecrest, a 750,000-square-foot project at 200 Park Avenue in the affluent Cleveland suburb of Orange Village. It features two office buildings and 87 residential apartments as well as 400,000 square feet of retail space on a 58-acre plot. The financing was aimed to reduce interest costs and included funds to fully stabilize the asset.

“[The building has a] significant retail component, and we’re very selective on retail,” Fastov said. “It’s in Cleveland, of all things, which is not thought of as a high-growth market.”

Fastov called the project a “prototype of the future” when it comes to experiential retail in a live, work and play environment. “We think it’ll really compete well with older product.”

Shops there include Whole Foods, West Elm, Williams-Sonoma, a movie theater and Recreational Equipment, Inc. (REI). “You can practice in a kayak [at that REI],” Fastov said. “You can’t get that on the internet. This is where retailers will want to be because that’s where people will want to be.”

Going forward, Fastov thinks the only market changes to come are “the beginnings of distress.”

He added, “So I think we’re going to continue to try to see [every deal] we can in the market and make sure the risk and returns we’re targeting for our funds remain consistent by being more selective over time.”—M.B.

12. Miriam Wheeler and Ted Borter

Co-heads of the Americas Real Estate Financing Group at Goldman Sachs

Last Year’s Rank: 16

In 2018, Goldman Sachs originated $14 billion in commercial real estate debt and ranked third among U.S. CMBS bookrunners with an 11.6 percent market share and just over $8.9 billion in issuance across 24 deals, according to Commercial Mortgage Alert. That issuance total marks a 24 percent decline from 2017, in line with the overall narrative of a slowing mortgage-backed securities space.

It’s quite a legacy for the new team to look after.

Miriam Wheeler and Ted Borter have taken the reins from Goldman Sachs’ David Lehman (who left this January to join Connecticut’s Department of Economic and Community Development under Gov. Ned Lamont) as co-heads of real estate financing.

Wheeler oversees large loan originations and is responsible for structuring senior mortgages as well as mezzanine loans. She joined Goldman Sachs in 2005, was named a managing director a decade later and was eventually made partner last year.

Borter, an industry vet who started at Goldman in 1997 and was elevated to managing director in 2002, is the head of the firm’s commercial mortgage finance business in North America.

In addition to their massive CMBS book, the bank also ranked third in loan contributions last year at $8.6 billion—$2.4 billion in conduit and $6.2 billion in single-borrower transactions—good for an 11.3 percent market share.

With a new, veteran regime in place of Lehman, watch out for this highly-respected duo in 2019.—M.B.

13. Dustin Stolly and Jordan Roeschlaub

Vice Chairmen and Co-Heads of Debt and Structured Finance at Newmark Knight Frank

Last Year’s Rank: 33

Even in 2018’s uber-competitive market, some players’ deal volume continued to soar, and that’s putting it lightly.

Case in point: Dustin Stolly and Jordan Roeschlaub, who almost doubled their deal volume, closing $11.8 billion worth of loans in 2018 compared with $6.5 billion in 2017. The dynamic duo racked up 97 transactions last year and a further 34 (representing an additional $3.4 billion) as 2019 kicked off.

“I think it was a function of our partnership just gelling,” Stolly said of the skyrocket in volume compared with the previous year. “We really hit our stride and this was really our first year working together as a team.”

“We’ve managed to do all of that volume with a delta force of a 12-person team that still runs fairly lean relative to some of our competition,” Roeschlaub added.

Their 2018 deal sheet reads like a who’s who of borrowers—from Blackstone to Normandy Real Estate Partners to Related Companies to RFR—with deal sizes ranging from $10 million to $1.6 billion. And a substantial chunk of last year’s business came from repeat borrowers.

Notable transactions included whales like the $1.8 billion acquisition financing and refinancing of 20 Times Square on behalf of Maefield Development and Fortress Investment Group (led by Natixis); the $250 million refinance of Normandy, Meadow Partners and AM Property Holding Corp’s 80-90 Maiden Lane (with Invesco as the lender); the $342 million refinance of 850 Third Avenue (with Natixis as senior lender and Paramount Group in the mezz position); and two loans totaling $355 million to refinance three of Nightingale Properties and Wafra Capital Partners’ office properties in Philadelphia’s Central Business District (with KKR and TPG).

The competitiveness of the debt markets was a stand-out trend for 2018, the debt duo said, and with that competition only heating up in 2019, it’s a great time to be a borrower.

“Spreads continue to compress and any transaction in any major [metropolitan statistical area] is being very aggressively bid,” Stolly said. “Most of our business last year was floating-rate and that’s really a snapshot of the capital that has been chasing transactions in the market.”

The twosome and their team have been proactive in coming up with creative ideas for clients and are enjoying a high volume of inbound calls as opposed to having to chase deals down.

“We’ve got a real passion for what we do, and so does our entire team,” Stolly said. “Everyone is competitive and intellectually curious, and the best outcome always seems to be accomplished for clients. That’s why the big names continue to hire us.”—C.C.

14. Jeffery Hayward and Michele Evans

Head of Multifamily; Senior Vice President and COO of Multifamily at Fannie Mae

Last Year’s Rank: 14

The future may be uncertain for the government-sponsored entities that back residential mortgages, given that their temporary government conservatorship has now persisted for a decade. But questions about the path forward barely dented Fannie Mae’s momentum last year.

Under the steady leadership of Jeffery Hayward and Michele Evans—who, combined, have spent nearly 60 years at the institution—Fannie Mae provided $65 billion in financing for multifamily sponsors last year. That was down slightly from 2017, when the agency set a volume record for the second straight year. But in Hayward’s view, quality must trump quantity when asset prices look questionable.

“We all know that real estate is cyclical,” Hayward said. “Part of our job is to provide stability to the market, and that means you have to maintain standards.” As the business cycle approaches a virtually unprecedented 11th year, Fannie Mae emphasized keeping loan-to-value ratios reasonable and ensuring healthy debt coverage levels, helping prevent lenders from overextending themselves in a too-eager search for yield in multifamily lending.

That’s not to say Fannie Mae shied away from having an impact. The agency’s work financed nearly 770,000 apartment units in 2018—and 90 percent of them housed or will house families that earn no more than 120 percent of area median incomes.

What’s more, Fannie Mae’s nine-year-old green bonds program has emerged as an unlikely example of a massively successful corporate effort to promote environmental design.

“We’ve been recognized as the largest issuer of green bonds in the world, having done $20 billion of that business last year,” Evans said, referring to a nod from the international Climate Bonds Initiative. “This effort is very focused on having positive environmental and social impact on the marketplace.”

The program has been responsible for saving 5.9 billion gallons of water and vast amounts of electricity, helping renters reduce utility bills by $72 million.

Hayward sees that achievement as a perfect complement to the agency’s affordability mission.

“We’re all on this journey of trying to house America for the people who have the least,” Hayward said. “Affordability is a pervasive problem and all of us will have to do our best and try to help.”—M.G.

15. Debby Jenkins, John Cannon, Stephen Johnson and David Leopold

Head of Multifamily Business; Senior Vice President of Production and Sales; Vice President of Small Balance Loan Business; Vice President of Targeted Affordable Sales and Investments at Freddie Mac

Last Year’s Rank: 13

When you finish the year with a record volume of business under your belt, what else can you do for a follow-up act in the next 12 months but raise the bar once more?

That’s exactly what Freddie Mac accomplished in 2018, once again topping its previous high-water mark for multifamily loan purchases after performing that same feat in 2017. Along with its slightly older sister, Fannie Mae, the junior government-sponsored entity continued to drive the commercial multifamily debt markets in a big way last year, buying up $78 billion in financings on apartment buildings and other commercial housing complexes.

And proving that no pair of siblings would be complete without a little friendly rivalry, Freddie also proudly widened the gap between its market share and Fannie Mae’s, claiming 53 percent of the business to Fannie Mae’s 47 percent.

According to Debby Jenkins, who took over the multifamily business line in the fall after its previous chief, David Brickman, was promoted to Freddie Mac’s president last year, that’s the biggest gap between the two agencies in their half-a-century in the markets.

Granted, there’s always uncertainty around a leadership change, especially as a figure like Brickman, a leading light in multifamily finance, moves on from day-to-day management of Freddie’s multifamily lending. But in a red-hot environment for apartment deals, there’s no reason to think Freddie will miss a step under Jenkins’ leadership.

“It’s been a decade of really great times in multifamily overall,” Jenkins said, reflecting on a 10-year-old bull market for rental properties. “And there’s a difference with this cycle relative to the last one: we’re leading the industry.”

As proud as the agency is of its pace-setting volume, it’s equally keen to avow that it’s stringently resisted pressures to loosen credit standards.

“I think you get to a leadership position by [business] volume—but with leadership comes responsibility,” said John Cannon. “If you move away from that, you could have the tendency to have far-reaching effects in the industry.”—M.G.

16. Ralph Herzka and Yoni Goodman

Chairman and CEO; President at Meridian Capital Group

Last Year’s Rank: 10

Since he founded Meridian Capital Group almost 30 years ago, Ralph Herzka has grown the New York City-based brokerage into a massive presence on the national lending scene that’s consistently a force to be reckoned with.

The company’s work in 2018 was no exception. It closed around $37 billion of transactions, with impressive ledgers of business both on its home turf and elsewhere. In the Big Apple, it advised on $20 billion worth of debt deals, while arranging $17 billion in debt elsewhere in America. As Yoni Goodman, the firm’s president as of this January, pointed out, either one of those figures on its own would be enough for a strong ranking among national mortgage brokers.

“We handily beat our past totals in 2018,” Goodman said, noting that Meridian did about $32.5 billion in lending business the previous year. “2018 was an absolutely successful year, extremely fast-paced and extremely competitive.”

In addition to an impressive geographic reach, few firms work on as diverse an array of deals as Meridian does. About $17 billion in business came from deals worth less than $25 million each, Goodman said. But the company also churned out $8.5 billion in deals worth more than $100 million each. That’s remarkable coverage of both ends of the market.

Close to home, in October, it helped Daishin Securities, a Korean firm, land a $100 million mortgage to support its purchase of 400 Madison Avenue. It also found a lender, Madison Realty Capital, for Accurate Builders and Developers of New Jersey’s 1,161-unit development portfolio in that state, in a deal worth $258 million.

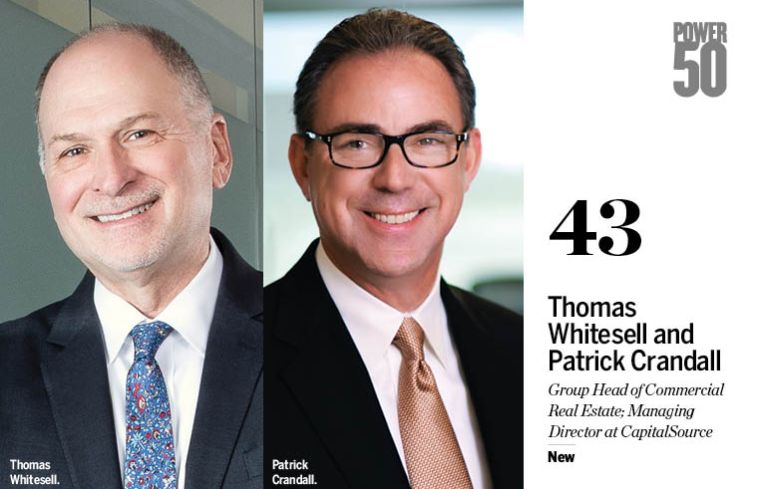

But don’t underestimate the firm’s work in other markets: Over the summer, Meridian arranged a $117 million CapitalSource financing for a major residential project in Los Angeles, The Residences at Wilshire Curson.—M.G.

17. Grant Frankel, Philip McKnight and Ken Ziebelman

Managing Directors at Eastdil Secured

Last Year’s Rank: 12

While these three Eastdil Secured veterans arranged a combined $14.5 billion with their team of 10 out of the firm’s New York offices, altogether, the company dealt on $54 billion in debt.

That’s down from its $57.1 billion company-wide figure in 2017, but still a prodigious jump up from its $41.1 billion in 2016.

“We have a very interactive group, and we work a lot with each other,” Grant Frankel said of the company’s reach, with over 50 debt professionals globally. “We saw a tremendous amount of refinance business and more construction as well.”

Frankel said the firm benefitted from its exposure to retail at a time when “[there’s so much] talk about how difficult it is,” he said. “We did grocery-anchored centers to higher-leveraged [repositioning] loans to other deals north of $1 billion.”

That’s evidenced by this team’s fingerprints on one such deal, the 10-year, $1.75 billion CMBS loan to Turnberry Associates and Simon Property Group for their 2.2-million-square-foot Florida retail monster, the Aventura Mall in Miami. Led by J.P. Morgan Chase, a trio of Deutsche Bank, Morgan Stanley and Wells Fargo were on the deal. J.P. Morgan funded 34 percent of the loan, and each of the other three banks financed 22 percent. A $750 million portion of the loan was securitized into a single-asset, single-borrower CMBS deal, called Aventura Mall Trust 2018-AVM and issued by J.P. Morgan. The remainder of the $1.75 billion loan is slated for future CMBS securitization.

In November, the group arranged a 10-year, $600 million loan from Bank of China, Helaba and Deka Immobilien to refinance L&L Holdings’ 200 Fifth Avenue.

“That was a 10-year balance sheet loan with banks,” Frankel said. “The fact that the bank market was willing to go 10 [years] was an interesting aspect of that.”

The shop also procured north of $550 million each on a trio of portfolio deals.

“Our platform and culture gives us a strong ability to handle larger, more complicated deals that need more structuring, whether it’s construction or refinancing,” Ken Ziebelman said.—M.B.

18. Steve Kenny, Brad Dubeck and Ken Cohen

East Region Real Estate Executive; Senior Vice President and New York and New Jersey Market Executive; U.S. Head of Commercial Real Estate Structured Finance at Bank of America

Last Year’s Rank: 28

Bank of America did about $26 billion in total debt originations in 2018.

Led by Steve Kenny and Brad Dubeck, the bank’s balance sheet business registered in at a whopping $20 billion, around $3 billion of that in New York, Dubeck said.

The newest addition to Bank of America’s Power 50 list ranking is its head of structured finance, Ken Cohen, who oversaw the bank’s origination of over $5.2 billion in CMBS, good for a nearly 7 percent market share and up 4 percent from last year, according to Commercial Mortgage Alert.

As a CMBS bookrunner, the bank’s volume dipped 7.5 percent, while actually growing its market share to nearly 7 percent, reflecting its strong position in the space despite the slowdown in the CMBS market.

Among their greatest hits, Bank of America led a $650 million financing to MCR Development and Building and Land Technology (BLT) backed by a portfolio of 53 Marriott and Hilton select-service and extended-stay hotels across 15 states and 31 markets. The deal included Wells Fargo and two other mezzanine lenders.

It also lent $170 million to Related Companies to refinance $148 million in acquisition debt from the company’s purchase of 27 Drydock Avenue, an eight-story life sciences property in Boston.

Thanks to the effects of e-commerce on retail Bank of America pivoted to value-add and construction opportunities as well as a fuller syndication market.

“Sponsors seemed to be more in need of subordinate capital as opposed to senior debt,” Dubeck said. “And also, it was a positive for us, if we liked a deal, that many banks, including [us]were more willing to hold larger loans [on their balance sheets] because of competition.”

As the bank slugs through the mud of a late-cycle environment, it’s putting more focus on its borrower clients that it knows will deliver should there be a negative turn in the market. —M.B.

19. David Durning and Marcia Diaz

CEO; Managing Director and Head of Originations at PGIM Real Estate Finance

Last Year’s Rank: 21

After years of financing in the $15 billion range—the total for 2017 was $14.8 billion, up from $13.9 billion the year before—PGIM originated $18.1 billion in 2018 and hopes to at least match that number in 2019.

The company attributes this uptick to significant growth in its multifamily, industrial and core-plus lines of business.

“Across all of our capital sources, all the agency business plus our core investors, general accounts, and some of our third-party investors, we did a lot of multifamily business,” said Marcia Diaz. “Within our core space, we were very active in the industrial space. We did a lot of large portfolios in industrial, and that comprised about 30 percent of our core production.”

Similarly, David Durning said, “The key development for us last year was the focus we’ve given to investing in the core-plus space. We’ve made investments in talented people in broadening our skill set organizationally. We put almost a billion dollars of that money to work this year, and even in how we service those loans, we’re building [more] capability.”

Another exciting development for PGIM last year was its broadened focus on global markets, with $1.4 billion in originations coming in across borders, including from Australia, Canada, Japan and throughout Europe.

What’s more, a new crop of outside investors is pushing PGIM to take on more creative financings.

“Over the last few years, we have been raising more capital from third-party investors, and those investors have a more diverse appetite then we have historically seen,” Durning said. “So, in addition to what we traditionally got from our core investment activities, we have investors who are more interested in the higher yields. Not super high yields, not high yield real estate debt, but core-plus.”

One massive deal saw PGIM team partner with the New York State Teachers’ Retirement System to provide $1.1 billion in financing for a 146-property, nearly 22-million-square-foot industrial portfolio in 18 markets across the U.S.

Durning sees all of this as indicative of a very promising year ahead.

“For 2019, we’re targeting, and have the appetite for, another $18 billion-plus year,” he said.—L.G.

20. Larry Kravetz

Head of CMBS Finance at Barclays Capital

Last Year’s Rank: 26

He isn’t Lenny Kravitz, but he certainly does rock.

In addition to increasing Barclays’ loan originations to $8.5 billion in 2018 from $6.5 billion the year prior, Larry Kravetz launched its balance sheet loan program in 2018 and came out of the gate swinging. The bank racked up $3.25 billion in balance-sheet originations in its opening year and made its market debut with the $850 million financing of Blackstone’s Kensington office portfolio.

“It opened a lot of eyes to what our risk profile was and also our ability to take down big deals and successfully execute them,” Kravetz said. “It actually became a really wonderful first deal for us to do, as far as advertising our presence in the market.”

Barclays’ footprint is expanding significantly, thanks to its balance sheet and warehouse lending activities (the latter of which quadrupled in 2018), but CMBS is still “right in the middle of what we do,” Kravetz noted.

“We’re not de-emphasizing CMBS, we’re just broadening what we’re putting out into the industry,” he said.

The bank was sole or co-lead lender on 12 SASB deals and continued to grow its conduit business. While the overall conduit market was down 11 percent, Barclays’ conduit volume for loans under $50 million was instead up 6 percent.

Notable CMBS transactions included the $1.33 billion refinancing of Blackstone’s Willis Tower in Chicago—the largest single-property standalone CMBS transaction in 2018—and the $550 million financing of Colony Capital’s Courtyard by Marriott Portfolio.

Barclays was a bookrunner on the first commercial real estate collateralized loan obligation (CRE CLO) of 2019 and Kravetz expects the bank’s active role in the space to continue throughout the year.

“In providing the warehouse facilities to our CRE CLO issuer clients we’re building our pipeline, but for us it’s part of a bigger strategy to be a more active financing source for our clients,” Kravetz said.—C.C.

21. Greg Murphy

Head of Real Estate & Hospitality, Natixis CIB Americas

Last Year’s Rank: 25

Zut alors! Pardon my French, but Natixis Real Estate Capital had a pretty stellar 2018, racking up $7.84 billion in originations. That total—up from $7.52 billion in 2017—included $3.44 billion in balance sheet loans and $4.4 billion in CMBS.

“It was our biggest year ever,” Greg Murphy said. “At the same time, it was definitely a harder-fought year. Spreads tightened, the competition was especially fierce and in the CMBS market there was less activity, so it was a harder-fought business all the way around. But, it was a great year for us.”

Stand-out New York deals included the $1.8 billion financing for Maefield Development’s hotel and retail project at 20 Times Square and the $342 million refinance of HNA Group’s 850 Third Avenue, but Natixis has been busy closing deals from coast to coast.

“We’ve done a lot to diversify our business away from just New York, but we’re still focused on gateway cities,” Murphy said.

An example of that was Natixis’ $265 million loan to Extell Development for its InterContinental Boston hotel at 500 Atlantic Avenue in the city’s Financial District, which Murphy described as a “great deal with a repeat sponsor.”

Murphy attributes part of the bank’s success to its global reach and ability to source capital from all over the world. Between 2016 and 2018 Natixis doubled its distribution in Asia and EMEA.

Last year was also a year of internal promotions at Natixis. Michael Magner was named the head of originations for real estate and hospitality Americas; Jerry Tang became the global head of real estate and hospitality distribution; and David Schwartz was named the head of Natixis’ Los Angeles office for real estate and hospitality in the Americas.

As far as 2019 goes, Murphy said he doesn’t see the competition letting up, but Natixis has an impressive pipeline of deals teed up.

“It feels like it’s going to be a pretty good year,” he said. —C.C.

22. Gino Martocci and Peter D’Arcy

Executive Vice President and Head of Commercial Banking; Head of Commercial Real Estate and New York Area Executive at M&T Bank

Last Year’s Rank: 22

M&T Bank posted a strong year in 2018, utilizing freshly established credit platforms and leveraging its pedigree in the syndication market.

The bank’s balance-sheet originations grew slightly but remained relatively stable at $11.7 billion in 2018, from just over $11 billion in 2017. Of the 2018 total, $2.5 billion was distributed through M&T’s growing debt capital markets business, contributing to a record year for the company’s commercial real estate loan distributions.

Its new business originations—not including refinance activity—was up substantially to over $16 billion, driven by stronger balance-sheet originations and “largely by growth in our off-balance-sheet-platform capabilities,” Peter D’Arcy said.

“We had a very good 2018,” Gino Martocci said. “We’ve added a new program, a life insurance platform in the last 18 months and we have well over $1 billion in that.” The bank doled out an additional $5 billion in originations through its off-balance-sheet subsidiary M&T Realty Capital Corp., which was launched in the last 18 months; the $5 billion total included well over $1 billion in deals through its correspondent insurance placement business that the bank integrated in 2018 and continues to build upon.

Amidst the market’s ever-expanding pool of capital sources and growing competition, M&T’s insurance platform has allowed the bank to place long-term, fixed-rate debt while retaining servicing rights, providing its extensive roster of seasoned clients a wider selection of products.

And in what was a thin syndication market last year, M&T led a consortium of banks—along with RXR Realty—in providing a $530 million construction package to Gary Barnett and his Extell Development Company for its 68-story Brooklyn Point project at 138 Willoughby Street in Downtown Brooklyn.

“There was clearly a big tightening of non-bank competitors and we stood out because of our relationships,” D’Arcy said. “We maintained a lot of activity with top sponsors…One thing I’ve heard from larger [non-bank lenders] is we’re very tough to bump off on the [large deals] they want to get to.”—M.B.

23. Robert Merck and Gary Otten

Head of Real Estate and Agricultural Finance; Head of Real Estate Debt Strategies at MetLife

Last Year’s Rank: 20

MetLife’s commercial real estate loan origination volume dipped to $12.9 billion in 2018 from $14 billion the year prior, after record highs in 2015 and 2016.

“I’d say for the market itself, there weren’t as many opportunities, but that said, it was still a very strong year,” said Robert Merck. “We continue to build our asset management business and client [roster] on the commercial mortgage side as well.”

MetLife’s typical “down-the-middle” loan sits at 60 percent loan-to-value and at a 10-year fixed rate.

“We do a lot of short-term floaters—we’ve really run the gamut—but we’re usually in the first-mortgage space as there continues to be good relative value there,” Merck said. “We’re competing against other life companies and some banks doing balance-sheet and single-asset single-borrower CMBS players.”

In April 2018, MetLife provided a $205 million, 10-year fixed-rate loan to a joint venture between Jack Resnick & Sons and the Ruben Companies to refinance 110 East 59th Street, a Class-A office building.

In December, the insurer provided a $141 million loan to Clarion Partners for its $282 million acquisition of the 22-story office and retail building at 114 West 41st Street from Blackstone.

And to kick off 2019, the life insurer provided a 12-year, $300 million loan to The Macerich Company backed by the firm’s 540,000-square-foot enclosed outlet mall, Fashion Outlets of Chicago, at 5220 Fashion Outlets Way in Rosemont, Ill.—M.B.

24. Aaron Appel, Adam Schwartz, Jonathan Schwartz and Keith Kurland

Vice Chairman; Executive Vice President; Managing Director; Managing Director at JLL

Last Year’s Rank: 34

JLL’s Aaron Appel described his team’s business as “ever-evolving and certainly expanding.”

That’s accurate for 2018—and beyond. At the time of this interview in early March, news of the brokerage’s $2 billion acquisition of former competitor HFF hadn’t yet come to light. With the addition, JLL’s global reach has vastly expanded and its potential access to eager international capital has skyrocketed.

With just over $11 billion in loan originations across over 100 transactions in 2018—a 25 percent increase over 2017’s figure—JLL’s debt team of 30, led by the quartet of stars on this list, was involved in some of the year’s most high-profile deals.

One was the firm’s $2.2 billion debt and equity arrangement for Moinian Group and Boston Properties on the construction of their 2-million-square-foot office tower at 3 Hudson Boulevard.

“[3 Hudson Boulevard] was a transaction that involved a generational family owner looking for development partners to come in and spearhead the [project],” Appel said. “We brought in a joint venture partner who had developmental capabilities in what was a highly competitive investment. We also facilitated additional capital and set in place a structure for the project to be built in 2019 and 2020.”

Appel’s group also procured $750 million in construction financing from Deutsche Bank for Macklowe Properties‘ office-to-residential condominium conversion One Wall Street. That’s after Macklowe abandoned negotiations with J.P. Morgan Chase following more than a year of deliberating. Macklowe is developing 566 condominium units, with retail at the building’s base, in partnership with Qatari billionaire Sheikh Hamad Bin Jassim Bin Jaber al-Thani.

“One Wall Street will be the largest condo conversion in the history of the city,” Appel said. “It was a hugely complex partnership and there was noise in the background on the sponsorship side. The sheer size of the for-sale housing [portion] was somewhat of a challenge to finance, with the complexity of taking a pre-war office building and having that converted to for-sale condos.”—M.B.

25. James Carpenter and John Adams

Senior Executive Vice President and Chief Lending Officer; First Senior Vice President, Chief Administrative Officer and Senior Lending Officer at New York Community Bank

Last Year’s Rank: 24

New York Community Bank originated $7.1 billion in loans in 2018, up 13 percent from its 2017 totals. And in a year when nationwide multifamily developers were eager to bring more supply online to meet ever-higher demand for more apartments, originations on housing complexes were particularly lucrative for the bank, up 23 percent from 2017.

According to the company’s year-end financial report, NYCB’s loan portfolio increased $1.8 billion, or 5 percent, for the year, surpassing $40 billion. The company attributes this growth to “our flagship multifamily loan product, which increased 6 percent during the year and currently stands at just under $30 billion.”

In September, NYCB teamed with Morgan Stanley to provide $900 million to RXR Realty for the refinancing of its 2.3-million-square-foot, 19-story Starrett-Lehigh Building at 601 West 26th Street between 11th and 12th Avenues. This allowed RXR to pay down $525 million in existing debt and fund the repositioning of the building’s retail space.

Other prominent deals included a $73.5 million loan to Kushner Companies for the $102.5 million acquisition and renovation of the Prospect Place multifamily community in Hackensack, N.J. NYCB also loaned $46 million to Castle Lanterra Properties for the refinancing of the 224-unit multifamily complex The Lena in Raritan, N.J.

In October, the company announced a merger between its commercial bank subsidiary, New York Commercial Bank, and its primary subsidiary, New York Community Bank. According to a company release, the merger will allow “all 30 branches of the Commercial Bank [to] operate as branches of the Community Bank.”—L.G.

26. Willy Walker

Chairman and CEO of Walker & Dunlop

Last Year’s Rank: 19

If demographics are destiny, multifamily assets seem fated to become an ever-more crucial facet of America’s housing landscape.

Few firms are closer to the center of that action than Walker & Dunlop.

Last year, the Bethesda, Md.-based lender was the No. 2 contributor to Fannie Mae financings, going toe-to-toe with the top dog, Wells Fargo. That’s an impressive feat for a firm that’s been public for less than a decade. Combine that achievement with strong showings in the standings for Freddie Mac and U.S. Department of Housing and Urban Development deals—plus a bit of balance-sheet business—and you get a grand total of $25 billion in debt originations.

That funds a whole lot of apartments.

On the other hand, the year also presented new challenges in the guise of interest rates that finally saw fit to tick higher, which depressed deal flow, according to Willy Walker.

“There wasn’t a ton of growth, and it was one of those years where you really had to work hard to do it, because the overall transaction volumes came down,” Walker said.

As a result, the company’s originations took a slight hit from their 2017 levels, when Walker & Dunlop lent $27.9 billion. Still, the company’s revenues grew 2 percent last year—not a bad showing in such a relentlessly competitive environment.

Meanwhile, the firm has been unremitting about toeing the line on credit characteristics and underwriting.

“Our average [loan-to-value ratio] last year—on all $25 billion—was 65 percent,” Walker claimed. “And our average [debt service coverage ratio] was 1.42. There are clearly deals that come in to us where we say we don’t like them, based on the sponsor, asset, leverage levels or what have you.”

What’s more, Walker has been pounding the pavement between Capitol Hill office buildings, advocating for a continued role for the agencies in the multifamily markets.

“I think there’s the opportunity for a grand deal that gets housing finance reform done,” Walker said. “I think the Democrats and Republicans are closer together on the issues than they realize.”—M.G.

27. Steve Kohn, Dave Karson, Gideon Gil, John Alascio

Vice Chairman and President of Equity, Debt & Structured Finance; Executive Managing Director; Executive Director; Executive Director at Cushman & Wakefield

Last Year’s Rank: 46

When the trio of owners behind 575 Lexington Avenue were seeking a refinancing last year worth more than $400 million, they tapped one of the savviest debt advisory teams in the city: Cushman & Wakefield’s Steve Kohn, Dave Karson, Gideon Gil and John Alascio. (Alex Hernandez also worked on the transaction.)

And when Brookfield Property Partners was hunting for $650 million in financing to fund its purchase of a stake in Waterside Plaza, a residential development on Manhattan’s East River shoreline, Kohn’s group once again fit the bill.

All in all, last year the group arranged 53 lending deals worth a total of $6.2 billion—an impressive bound above its total from 2017, when it did $5.3 billion of business. More impressive yet has been the trajectory of C&W’s average deal size of late. In 2016, it typically worked on transactions valued at $66 million a piece. Last year, that figure was $117 million—better than a three-quarters improvement.

But the team’s work isn’t just limited to Manhattan, or even New York City.

“We cover all the major markets, and some beyond that,” Kohn said. “Our clients are a mix of private developers and operators, as well as private equity funds, pension funds, insurance companies, offshore entities.”

The list goes on. As does the roster of lenders C&W works with to match clients with the right provider of debt.

“We find capital from just about every source you can imagine,” Kohn added.

New Jersey, Florida and especially Pennsylvania have also become important regions for Kohn’s group at C&W: Its five deals in the Keystone State in 2018 alone were worth nearly $300 million.

“We’ve seen a lot of New Yorkers going down to Philadelphia to make acquisitions recently,” Kohn said.—M.G.

28. Chris Lee and Matt Salem

Head of Real Estate Americas; Head of Real Estate Credit at KKR

Last Year’s Rank: 40

Last year was a milestone year for KKR Real Estate Finance Trust (KREF). In addition to marking the platform’s first full year as a public company, it was its fourth full year of operations as KKR’s first dedicated real estate credit strategy.

“The business grew and evolved,” Salem said. “We focused on our existing businesses and we executed efficiently while increasing our activity. On the direct lending side we had a record origination year of $2.7 billion, so we’re a very large participant in that market now. And on the CMBS B-piece side of the business—through our RECOP fund—we were the leading B-piece investor last year and the largest risk retention investor in the space.”

KREF has quickly demonstrated its wherewithal as a leader in the transitional debt space. Its $2.7 billion origination total was an 84 percent increase on 2017’s $1.5 billion total. Fifty percent of that business came from repeat borrowers, and KREF maintained a competitive edge by providing certainty of execution up front and ongoing asset management post-close.

In November, the company closed KREF 2018-FL1, a $1 billion managed Commercial Real Estate Collateralized Loan Obligation (CRE CLO)—one of the largest CRE CLOs issued post-crisis.

“We have the ability to offer competitive pricing in this environment while still providing an attractive return to our investors,” Lee said.

KKR has also been lending to more sophisticated sponsors in larger markets.

“We’ve gravitated towards a larger loan size—our average loan was over $140 million last year—so once you get above $100 to $150 million, the air starts to get thinner from a competitive perspective,” Lee said.

Notable 2018 transactions include a $341 million senior loan for an Atlanta and Tampa, Fla. multifamily portfolio on behalf of Cortland Partners, and a $214 million loan for Related Beal’s $276 million acquisition of 451 D Street in Boston’s Seaport District.

Today, its commercial real estate loan portfolio sits at roughly $4.1 billion—two times increased from the end of 2017 and more than a three-times increase from the second quarter of 2017, when it completed its IPO.—C.C.

29. Tom Traynor and James Millon

Executive Vice Presidents at CBRE

Last Year’s Rank: 30

James Millon and Tom Traynor transformed CBRE’s debt advisory practice when they moved over from Deutsche Bank two years ago, and in 2018, the dynamic duo was going strong.

Their New York-based team, a small but nimble outfit, churned through an impressive $2.9 billion in debt deals last year. That figure included the $647 million financing to turn a self-storage facility on Manhattan’s West Side into Terminal Stores, a major new retail project; as well as financings on national portfolios owned by KKR, Harrison Street Real Estate Capital and Greenfield Partners worth more than $500 million combined.

Granted, last year’s haul was a decline from the eye-watering $5.1 billion the outfit tallied in 2017. But that’s par for the course when you’re big-game hunting.

“We’re looking for the big, complicated deals that we know institutional clients are going to be involved in,” Millon explained. “Sometimes you have situations where, with those large deals, you don’t know when they’re going to pop up.”

Case in point: thus far, in 2019, the group is already well on its way to topping last year’s numbers on the backs of two major transactions.

“[We’ve] closed a $700 million multifamily portfolio for Rockwood and Mill Creek and the $910 million Space Center Industrial Portfolio for Blackstone,” Millon enthused. The multifamily deal brought financing to a group of nine assets spread nationally across as many states, and, alas, a spokeswoman for CBRE said that the Blackstone financing was too hush-hush to discuss further.

Of course, the team’s already an old hand at big deals. 2018’s list also included a $180 million loan on Oxford Property Group’s Aalto57 building in Manhattan, and a $192.7 debt deal on behalf of Walton Street Capital for The Landing at MIA, a big mixed-use campus in Miami.—M.G.

30. Dan Bennett, Jordan Bock and Brett Kaplan

Head of Capital Markets; CIO; Head of Originations at LoanCore Capital

Last Year’s Rank: New

With $4.4 billion in originations last year including $3.6 billion in balance-sheet business to add to an overall mortgage book now worth $12 billion, it should be no surprise to see LoanCore Capital making its mark. The versatile Greenwich, Conn.-based shop bounds onto the Power 50 list as the highest-ranked lender among this year’s first-time honorees.

The platform’s leaders, Dan Bennett, Jordan Bock and Brett Kaplan, are fresh off of issuing the largest whole-loan commercial real estate collateralized loan obligation in history last year: a $1.05 billion deal in June that securitized 27 transitional loans in cities across the country. Then there’s the firepower and flexibility afforded by support from two gargantuan public investment pools: the Canadian Pension Plan Investment Board, and GIC, Singapore’s sovereign wealth fund.

In a crowded marketplace, flexibility has been the secret sauce, according to LoanCore’s executive team.

“We can do fixed-rate, floating-rate, short-term, long-term, and come up with creative structure,” Bock said. The financial wherewithal to work on $100 million-plus deals, as well as “the ability to do things that are complicated,” have both been competitive advantages, he added.

Indeed, LoanCore turned in a remarkably diverse range of debt deals last year, from the $170 acquisition loan that funded the purchase of what used to be Midtown Manhattan’s W Hotel to a $42 million refinancing for a major Salt Lake City office tower that had run into delinquency issues on its previous CMBS deal.

Itself a CMBS lender on longer-term debt, LoanCore sees its willingness to retain risk on its balance sheet as a key differentiator.

“We are a risk retainer on all the deals we do,” Kaplan said. “We’re making all our own credit decisions, particularly on the fixed-rate side. It’s the closest thing to a balance-sheet product in the CMBS world.”

Meanwhile, the firm is hoping that significant expansion of its CLO business will propel it towards an even more active 2019.—M.G.

31. Matthew Masso and Stefanos Arethas

Head of Commercial Real Estate Finance; Head of Commercial Real Estate Origination at Credit Suisse

Last Year’s Rank: 32

CMBS-first lenders were up against a competitive landscape last year, and even the inimitable Credit Suisse lending team had its hands full working to keep pace. Last year saw the bank’s market share drop by nearly a quarter as both bookrunner and contributor, according to statistics from Commercial Mortgage Alert.

“Real estate owners are less certain about where to allocate capital if they sell, and buyers think they may get a better price if they wait,” Stefanos Arethas explained. “Competition among lenders remains stiff.”

But Arethas and Matthew Masso proved more than capable of churning out deals. In March 2018, Credit Suisse led a $1.35 billion single-borrower transaction that funded a 50-asset retail portfolio controlled by SITE Centers—formerly known as DDR—at a moment when only the savviest lenders have the confidence to wrangle big shopping center deals against the disruptive rise of e-commerce. To make matters worse, 12 of the properties were in Puerto Rico, still reeling from Hurricane Maria.

“Despite all that, the team was able to structure a deal that not only protected investors and led to overwhelming demand for the bonds, but also met the needs of the client and helped to facilitate the creation of their new company,” Masso said.

But the slowdown in private-label CMBS conduits last year also has Credit Suisse looking to build out more powerful balance-sheet and warehouse businesses. That initiative was in evidence last year with the bank’s $400 million bridge loan on Plum Healthcare’s portfolio of California nursing homes.

“We feel that many of the structural changes in certain areas of the real estate health care lending space, such as skilled nursing, are working through the system,” Arethas said. “With a potential bottoming out of credit, that’s a good place to be lending to.”—M.G.

32. Steve Rosenberg

Chairman and CEO of Greystone

Last Year’s Rank: 38

Greystone had a busy 2018, growing its commercial mortgage origination balance to a record $10.3 billion from $9.5 billion in 2017 while expanding its footprint in the industry.

“I think it was a great year for our growth,” Steve Rosenberg said. “Our mission is to be the number-one lender in the country for commercial real estate, starting out with multifamily and health care.”

Rosenberg’s Fannie Mae and Freddie Mac volume was $6.7 billion. It ranked as the number-one lender for Housing and Urban Development (HUD) multifamily and health care loans on the year at $1.8 billion and ranked in the top 10 for both Fannie Mae ($3.9 billion) and Freddie Mac ($2.61 billion) multifamily debt originations.

It was also the top producer of small-balance loans for Fannie (loans at $3 million or less nationwide and at $5 million or less in “high-cost” markets) and it also ranked third in Fannie affordable housing financing.

Along with its robust government-sponsored enterprise presence, Greystone also closed its first eight-year real estate debt fund, totaling $750 million, increasing its bridge and mezzanine lending capacity to north of $3 billion; the firm deployed just over $1 billion in bridge debt last year. Its investment sales division also closed transactions exceeding $2.2 billion.

In September 2018, Greystone closed the first-ever seniors housing collateralized loan obligation, a $300 million pool comprising only health care assets.

While they were at it, they launched Greystone Labs, the technology innovation wing of the firm that’s headed up by Rosenberg’s son, Zac. Right now, it’s developing online services to decrease the amount of time it takes to close an agency loan.

“We’re constantly pushing down process times, using tech, and we’re also starting to experiment in digitally reaching out to real estate owners the same way that single-family has transformed into an online business,” Rosenberg said. “Our belief is there’s no reason why any property should take more than 24 hours for a commitment and then a few days to close.”—M.B.

33. Robert Verrone and Christopher Herron

Principal; Managing Director at Iron Hound Management Company