The 50 Most Important Figures of Commercial Real Estate Finance

By The Editors April 5, 2017 9:00 am

reprints

Was it a sweet ‘16? Only for some of the industry’s powerhouses.

Most banks saw a decrease in lending activity last year, as did some of the larger institutional private funds. It was, undoubtedly, the year of the alternative lenders, who filled the construction and transitional debt void nicely, upping their originations significantly on the way. Life companies didn’t fall far behind and, in several cases, outperformed their 2015 figures.

That said, we added a few private lenders to our rankings, like Mesa West Capital at No. 40 and Mack Credit Real Estate Strategies at No. 49. A bigtime U.K. hedge fund even earned an honorable mention. Acore Capital, which was founded in May 2015, jumped up to the No. 10 spot from No. 39 last year, very much due to its tremendous growth in the bridge-lending space.

And one notable addition was Bank of the Ozarks. The Little Rock bank that could was exceptionally active on the construction lending front and scored the No. 31 spot.

Janet Yellen—who had landed the No. 20 spot on our list last year as the fate of interest rates were uncertain—still yields a huge amount power over the financial markets, but almost all of the lenders Commercial Observer spoke with now expect a couple of more quarter-point rate hikes and have baked those changes into their underwriting. If anything, industry experts see interest rate increases as an indication of economic growth (and for some, a way to increase pricing).

Now, under the Trump administration, there are new faces (one who also happens to have produced a number of Hollywood films) who stand a greater chance at dictating what happens in the financial markets.—Danielle Balbi and Cathy Cunningham

1. Raymond Qiao

Chief Lending Officer at Bank of China

Last Year’s Rank: 3

On the campaign trail, now-President Donald Trump rattled against long-standing trade policies with China. At one point he suggested placing a 45 percent tariff on the country. He even labeled China as a currency manipulator.

But the commander in chief can’t scare Chinese money away from U.S. real estate lending. In fact, Chinese money played a huge role last year—not only in real estate investments in the U.S. but also on lending within America’s own borders.

The big fish in Chinese lending in America is the Bank of China and its numbers do not disappoint. Not only did the giant originate $4.5 billion in commercial real estate loans; it became a landlord when its brand new U.S. headquarters building, 7 Bryant Park, opened its doors to tenants.

As far as lending goes, the bank kept its geographic focus on gateway markets like New York, San Francisco, Los Angeles, Chicago, Washington, D.C., and Miami, and 70 percent of its transactions in 2016 were backed by income-producing properties, Raymond Qiao said. When it came to construction deals, Bank of China was more selective and opted to back developments in dense in-fill locations. In fact, Bank of China was one of five lenders to take down the whopping $1.5 billion construction loan for SL Green Realty Corp.’s One Vanderbilt.

The bank also provided a number of refinancings for its clients, including a $314 million loan to Jamestown, George Comfort & Sons and Loeb Partners on a 15-story office building at 63 Madison Avenue in NoMad and a $60 million mortgage for Jeff Sutton’s single-tenanted retail property at 661 Eighth Avenue in Times Square. On the West Coast, Bank of China provided a $390 million construction-take-out loan for Crescent Height’s Ten Thousand, a 40-story, luxury rental building in Los Angeles.

Looking forward, Qiao said that while the new administration’s tone is pro-commerce, it’s too early to tell if commercial real estate will benefit. But in regards to rising interest rates, he said, “expensive money will reduce transaction volume across the board, especially for those buyers dependent on a lower cost of funding.”—D.B.

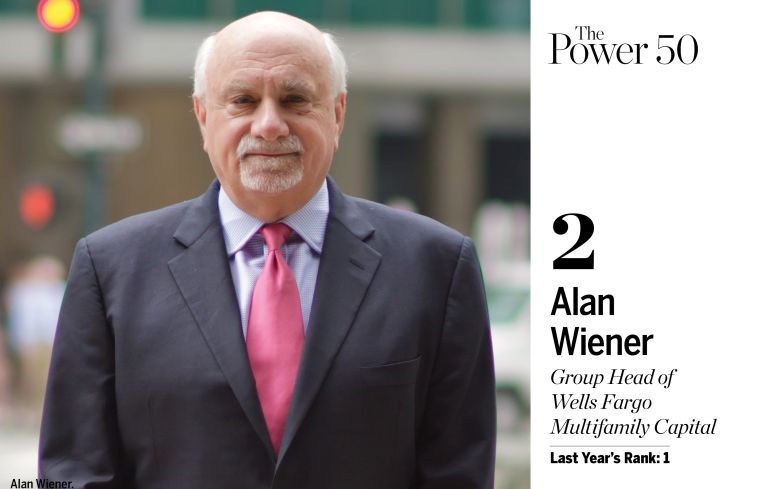

2. Alan Wiener

Group Head of Wells Fargo Multifamily Capital

Last Year’s Rank: 1

When Alan Wiener talked about Wells Fargo’s activity in 2015 for the Top 50 list last year, he said it would be a difficult 12 months to duplicate. Yet, in 2016 his team originated roughly the same amount of debt, finishing off the year with $15 billion in loans provided across the country.

The San Francisco-based lending giant started the year off strong, closing on a $2.6 billion loan for Starwood Capital Group’s purchase of a national multifamily portfolio from Equity Residential. Wiener’s team also worked on the origination of a $500 million credit facility to national manufactured housing owner YES! Communities. The Denver-based owner-operator used the proceeds to consolidate its portfolio last August.

Outside of those two major deals, much of Wells Fargo’s 2016 was characterized by flow business, or refinancings, of conventional, affordable and senior housing across the United States. “People wanted to lock in low interest rates,” Wiener said. “That’s happening this year as well.”

As far as where interest rates will go in 2017, Wiener said there is no real way of knowing. “If I knew that, I could just stop working and invest in futures,” he joked. “I think interest rates will go up incrementally but not a lot.”

One of the real issues that could affect not only the business Wiener oversees at Wells Fargo but also affordable housing across the nation is potential tax reform. He explained that if tax credits become less attractive to investors, more subsidies from city and state municipalities will be needed, and that combination would likely result in the creation and preservation of less housing.

That said, Wiener’s group remains fully committed to financing all types of housing. Last year in New York City, the bank lent on Related Group’s 400-unit, fully affordable Marine Terrace apartment complex in Astoria, Queens. The loan refinanced old debt on the property and funded the creation of 23 more units on the site to provide supportive housing for veterans. In November, Wells Fargo originated an $80.4 million construction loan and invested $67 million in low-income housing tax credits for the development of St. Barnabas Hospital in the Bronx. On completion, the property will house 314 affordable units, a medical care facility, a retail space and a day care center.—D.B.

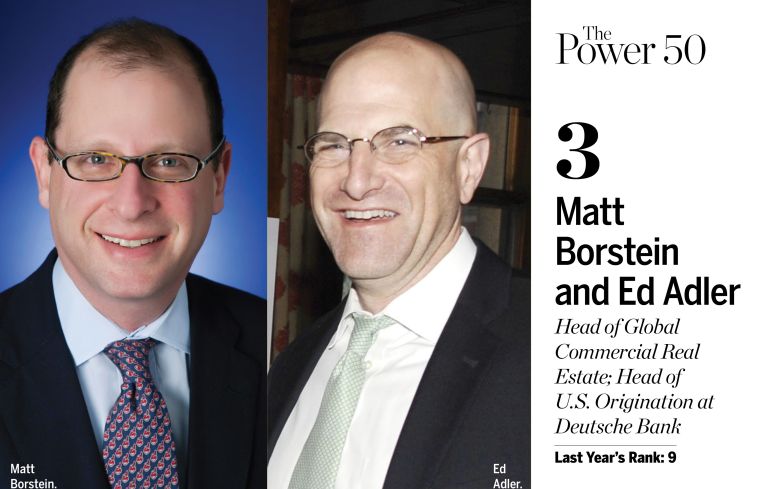

3. Matt Borstein and Ed Adler

Head of Global Commercial Real Estate; Head of U.S. Origination at Deutsche Bank

Last Year’s Rank: 9

Deutsche Bank started off with a bang last year with a $780 million financing in February. The bank provided CalPERS, the California pension fund, with a first mortgage for 787 Seventh Avenue, as Commercial Observer reported at the time.

“That got us running really well,” Matt Borstein said.

Also in the first quarter, Deutsche was part of a consortium of banks that provided about $1.2 billion in refinancings to Brookfield Property Partners for 225 Liberty Street.

After this, Borstein said executives spent a considerable amount of time reassessing market conditions knowing that risk retention was coming up and large trades needed to be completed.

“We had to address how to deal with risk retention in the market,” Borstein said. “Deutsche in particular started that process a little ahead of everyone else.”

One of the bank’s successes Borstein touted was 10 Hudson Yards. Deutsche securitized the $1.2 billion mortgage on the site. He called this “the highlight of the year” and a “landmark transaction for us and the city.”

The German bank was the first to have both the L-shaped and horizontal risk retention compliant structures under its belt, as well as the first to take down a single-asset, single-borrower deal for 667 Madison Avenue under the new regulation.

In total, Deutsche acted as bookrunner on 25 CMBS deals totalling $9.7 billion in 2016. It contributed $7.9 billion to CMBS last year, or 11.9 percent of market share, according to Commercial Mortgage Alert, down from roughly 18 percent in 2015.

“I think [667 Madison] got the ball rolling for us and the rest of the market to see how these deals could be done going forward,” Borstein said. “I think that was an important deal for us and the market in general.”

After 18 months of shying away from construction lending, Deutsche jumped back into that side of the market. That included a $650 million deal for Gary Barnett’s Extell Development at 251 South Street.

“He had an important need on an important asset,” Borstein said. “We stepped up for him.”

The company is active in the bridge loan space, especially in New York City. That included 441 Ninth Avenue on the Far West Side and the Doubletree by Hilton hotel at 346-350 West 40th Street, which each exceeded $200 million.

All this came amid a company restructuring and an investigation into allegations that the bank misled investors in the packaging, securitization, marketing, sale and issuance of residential mortgage-backed securities between 2006 and 2007. This January, Deutsche agreed to a $1.7 billion settlement. And the bank is sorting out how to deal with its relationship with President Donald Trump, to whom the bank lent roughly $300 million before inauguration. Bloomberg Politics noted, “What makes matters more complicated is that the U.S. government has been investigating Deutsche Bank’s failure to flag trades by wealthy Russians who spirited $10 billion out of Russia.” A bank spokesman declined to comment on the situation.

Borstein assured that the commercial real estate group has remained unscathed.

He noted, “We did not see a single lost piece of business due to complications at Deutsche Bank.”—Lauren Elkies Schram

4. Michael Nash, Stephen Plavin, Jonathan Pollack and Tim Johnson

Co-Founder and Chairman of Blackstone Real Estate Debt Strategies; CEO of Blackstone Mortgage Trust; Global Head of Blackstone Real Estate Debt Strategies; Senior Managing Director at Blackstone Real Estate Debt Strategies

Last Year’s Rank: 2

Blackstone Group spreads its financing across three businesses: its origination platform Blackstone Real Estate Debt Strategies (BREDS), its real estate investment trust Blackstone Mortgage Trust (BXMT) and its hedge fund management platform that trades commercial mortgage-backed securities. Across BREDS and BXMT, the private equity giant lent a total of $6.7 billion in 2016, down from $14 billion in 2015 (when it purchased the $14 billion GE Capital Real Estate portfolio).

Despite the decrease, nearly $7 billion in debt deals is still quite a bit of action, and it places Blackstone ahead of many of its competitors. Last year, BREDS’ business was primarily driven by its institutional clients in major core markets like San Francisco, Los Angeles and Seattle, and according to a spokeswoman, “the opportunities were made possible by our ability to act fast, bring certainty to a transaction and serve as a ‘one-stop’ solution for our borrowers.”

That said, Blackstone was very active in New York City and, in November 2016, provided a $349.5 million construction loan to The Georgetown Company and Pershing Square Capital Management for the repositioning of 787 11th Avenue, a former Ford dealership.

The following month, Blackstone provided two hefty acquisition loans, including a $200 million financing for Savanna’s purchase of The Falchi Building in Long Island City, and a $158.8 million mortgage for Patriarch Equities, Sionio Group and Highgate’s buy of the Stewart Hotel at 371 Seventh Avenue in Midtown.—D.B.

5. Steven Mnuchin

U.S. Secretary of the Treasury

New

Goldman Sachs veteran Steven Mnuchin had a relatively easy confirmation process compared to some of President Donald Trump’s cabinet nominees. Now, as head of the Treasury Department, he is (along with the chair of the Federal Reserve) the most influential economic policymaker in the United States—and it is safe to assume that many of those policies could have considerable impact on the commercial real estate finance market.

Mnuchin followed in his father’s footsteps and started at Goldman soon after graduating from Yale University in 1985. He quickly climbed the ranks at the investment banking giant and held significant sway over Goldman’s mortgage operations, serving as head of the mortgage securities department in the 1990s.

After leaving the firm in 2002, Mnuchin dabbled in the private equity sector and, in 2004, made his mark as a Hollywood film producer when he co-founded film production company RatPac-Dune Entertainment with Brett Ratner and James Packer. He later served as an executive producer on blockbusters like American Sniper in 2014 and Mad Max: Fury Road in 2015. (In late March, Senate Democrat Ron Wyden called for an ethics violation investigation into Mnuchin regarding comments he made in an interview apparently promoting The Lego Batman Movie, which was financed in part by RatPac-Dune.)

He also got back in the residential mortgage game for a while, leading an investment group that acquired, in 2009, the failed California-based residential mortgage lender IndyMac, in the wake of the subprime mortgage crisis. Mnuchin helped nurse the company back to health, renaming it OneWest Bank and selling it to CIT Group for $3.4 billion in 2015.

While he’s no stranger to the real estate financing market, the real question is how Mnuchin’s policies as secretary of the Treasury will impact the market moving forward.

Already, he’s called for Congress to pass “comprehensive” tax reform with the goal of stimulating the economy. That could lead to more investor confidence in the commercial real estate sector and, hence, to more borrowing and further growth. Mnuchin is reportedly central in the Trump administration’s drafting of its tax reform proposal and has said he hopes to pass legislation by the August congressional recess.

Then there’s the question of Trump’s promised investment in infrastructure spending—the sort of stimulus that could lead to higher long-term interest rates and inflation—and a possible rollback of Dodd-Frank regulations viewed as burdensome on the financial services sector.

Whatever the next four years bring, Mnuchin will play a significant role in dictating U.S. economic policy, and that will almost certainly affect the state of commercial real estate financing in the foreseeable future.—Rey Mashayekhi

6. Ralph Herzka and Aaron Birnbaum

Chairman and CEO; Executive Vice President at Meridian Capital Group

Last Year’s Rank: 4

In the spring of 2016, RXR Realty and real estate investor David Werner made a bold purchase: the 42-story 1285 Avenue of the Americas for a whopping $1.65 billion. It’s no real surprise that, when RXR began shopping around for a loan, it turned to Meridian.

The $1.2 billion deal that Meridian’s Rael Gervis and Drew Anderman brokered for RXR (along with Adam Spies and Douglas Harmon, who were at Eastdil Secured at the time) from AIG and Morgan Stanley would stand out as a distinct moment of glory in a pretty lucrative year.

“It was a frenetic year of fast-paced finance,” Ralph Herzka told Commercial Observer.

According to Herzka, the firm did about $35 billion in finance deals in 2016—which was equal with what it did in 2015. However, last year Meridian also managed to generate another $2 billion in deals through its investment sales arm, which launched in 2015. (No, it’s not the financing part of the operation, perhaps, but $2 billion in business is hardly chump change.)

Of course, 1285 Avenue of the Americas was just one (extremely impressive) deal; Meridian also arranged a $330 million construction loan for Spitzer Enterprise’s massive, 856-unit Williamsburg project at 416-420 Kent Avenue, from Starwood Capital Group. Meridian has had its hand in Florida and the Northeast but has also extended its reach out west to California.—Max Gross

7. George Klett

Chairman of the Commercial Real Estate Committee at Signature Bank

Last Year’s Rank: 8

Start spreadin’ the news...Signature’s originations hit the $6 billion mark last year, mirroring 2015’s number. “We’re one of the most active lenders in New York City, and I think Signature’s reputation is that we understand the market and we can deliver,” George Klett said.

And deliver, it does. In 2016, the bank was busy lending on numerous Big Apple deals, including a $100 million acquisition loan for Dennis Wong’s 23-story apartment building buy at 377 East 33rd Street in Kips Bay and a $104 million loan for Bonjour Capital’s purchase of the 38-story Hamilton at 1735 York Avenue on the Upper East Side.

“What we focus on is multitenanted, income-producing properties in the New York City area,” Klett said. “We like multifamily, neighborhood retail properties, office buildings—but not Class A—some industrial and manufacturing buildings, all within 45 miles of New York City. We know the market very well, and we know all the players. We keep it close to home.”

When it comes to financial regulation, Klett is hoping the president follows through on his intentions. “The regulators are putting a tremendous amount of pressure on banks and forcing us to pull back a bit, which is presenting some difficulties,” he said. “[President Donald] Trump has said he is going to roll back regulation, but it takes a while. I’m hoping it happens, and the sooner the better, but to be realistic about it I think it’s going to take some time.”

In the meantime, it’s safe to say that Signature Bank is doing just fine. “We have a $22 billion portfolio with no losses and no problem loans. I’ve been [at the bank] for nine-and-a-half years, and during that time, we haven’t lost one dollar in real estate,” Klett said.

Doesn’t get much better than that.—C.C.

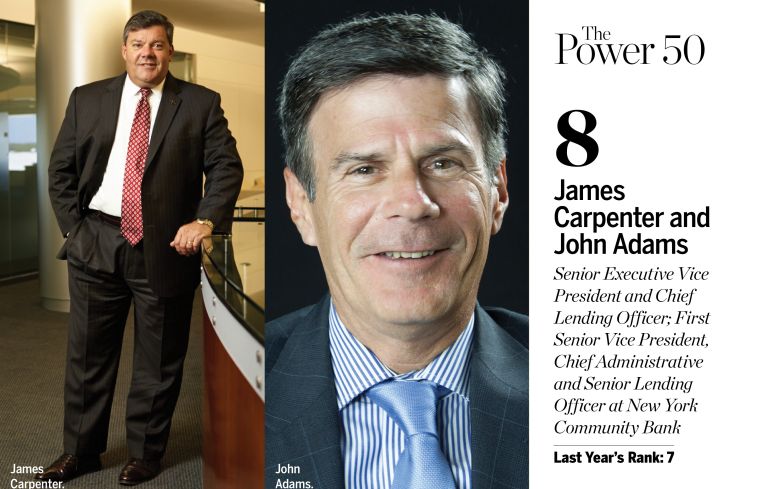

8. James Carpenter and John Adams

Senior Executive Vice President and Chief Lending Officer; First Senior Vice President, Chief Administrative and Senior Lending Officer at New York Community Bank

Last Year’s Rank: 7

When it comes to the bread-and-butter loans that keep New York’s multifamily and commercial real estate industry going, few names are more important than New York Community Bank.

But from its perch as the city’s most active lender in 2015, NYCB saw its loan origination shrink considerably in 2016.

According to figures from Actovia, NYCB executed 1,161 total deals in 2015, compared with 610 in 2016, a drop of about 47 percent. Moreover, the aggregated dollar amount of deals dropped to $3.72 billion from $6.48 billion, a decrease of more than 42 percent. (NYCB could not confirm these figures by press time.)

In December, regulators nixed NYCB’s potential merger with Astoria Financial because the combined institution would have more than $50 billion in assets, making it a “systemically important financial institution,” as has been widely reported.

Still, 2016 wasn’t too shabby a year by any means, and the bank was busy doing deals. Late last year, NYCB provided David Bistricer’s Clipper Equity with a $104 million loan to purchase The Brewster at 21 West 86th Street; the bank lent $148.6 million through 19 loans for a 21-property multifamily portfolio in the Bronx for The Morgan Group; and Banbridge Companies and China Orient Asset Management turned to NYCB for a $128 million mortgage to purchase the 656-unit Devonshire Hills complex in Suffolk County.—M.G.

9. Brian Baker

Global Head of Commercial Mortgages at J.P. Morgan Securities

Last Year’s Rank: 10

“We’re a unique business in that we are global,” said Brian Baker, whose team originated $16 billion in loans in 2016, up $2 billion from the year prior. “We’re basically in the business of either lending to banking clients or trading with investor clients. This is what keeps me interested in doing what I’m doing. We have clients on both sides of our business.”

One of Baker’s more exciting projects last year was providing a $765.5 million loan to the Witkoff Group for the Marriott Edition Hotel at 20 Times Square.

“We’re very excited to be involved with that,” Baker said. “The transition of Times Square has been happening for many years now, and [this project] takes it to the next phase.”

Baker and his team also lent $446.4 million to Michael Rosenfeld’s Woodridge Capital for the renovation of the Century Plaza Hotel in Los Angeles and $320 million to Related Group and Oxford Properties Group for 50 Hudson Yards.

These major deals were just the tip of the iceberg for Baker and his team’s productive year.

“We were also involved in some very large financing for Hilton Hotels & Resorts for some of their Hawaiian and San Francisco hotels,” he said. “We put them into a number of securitized transactions over the last few months.”

Baker emphasized that the variety of clients they service is a marked advantage for the firm—and one that hopes to make 2017 as strong as its predecessor.

“We are pretty broad in terms of our product offerings,” Baker said. “The power of the franchise is the ability to leverage the scale of J.P. Morgan and the client franchise. We will do smaller loans all the way up to billion-dollar loans. While we’re institutional in nature, there are plenty of good clients that need $5 million, $10 million, $15 million and $20 million loans as well. We try our best to balance those needs against the resources we have available.”—Larry Getlen

10. Warren de Haan, Boyd Fellows, Chris Tokarski and Stew Ward

Managing Directors at ACORE Capital

Last Year’s Rank: 39

The name may still be new, but the team is not.

In 2016—its first full year of business—ACORE was the second largest lender of transitional debt in the country, Boyd Fellows said.

And the numbers certainly add up. The private lender, which was launched by Warren de Haan, Fellows, Chris Tokarski and Stew Ward, provided $5 billion in commercial real estate debt loans across the United States, putting it second to Blackstone Group when it came to bridge lending.

Despite the volume, ACORE was extremely selective, and for every 20 deals that come across its desks, the firm may only lend on one. The company completed 70 transactions last year, making its average deal size just in excess of $70 million.

In September 2016, ACORE teamed up with Vanbarton Group and provided a $105 million debt package for Shorewood Real Estate Group’s mixed-use development at 17 John Street in the Financial District. In March of last year, the company made a $105 million construction loan against AECOM Capital and Ensemble Real Estate Investment’s 11-story hotel at 100 Independence Drive in Silicon Valley.

“In 2015 we were introducing ourselves to the market and getting our brand established,” Fellows said. “By the time 2016 began, our brand had become very widely known in the real estate community, so we executed on [deals] like we always do.”

If 2016 was only the start for ACORE, 2017 may have even more in store.—D.B.

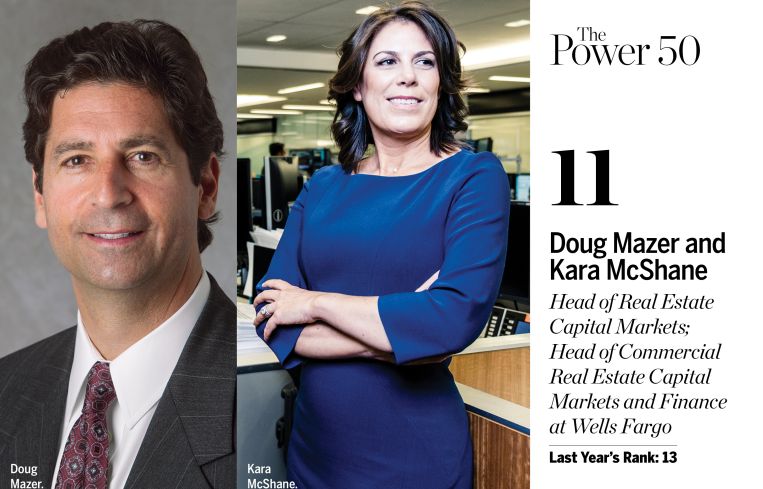

11. Doug Mazer and Kara McShane

Head of Real Estate Capital Markets; Head of Commercial Real Estate Capital Markets and Finance at Wells Fargo

Last Year’s Rank: 13

While many commercial mortgage-backed securities shops were dreading the implementation of risk retention, Wells Fargo got ahead of the curve, with Doug Mazer and Kara McShane at the forefront.

The San Francisco-banking giant, along with Bank of America Merrill Lynch and Morgan Stanley, actually led the first risk-retention structured deal, WFCM 2016-BNK1, in August 2016, well in advance of the rule’s Dec. 24, 2016, compliance date. Given the reception of the deal in the market, Wells Fargo issued a second BNK deal in 2016 and has issued two more, BNK3 and BNK4, so far this year.

Beyond structuring the first CMBS regulatory-compliant deal, McShane’s teams outdid themselves in terms of revenue growth. The commercial mortgage loan finance business experienced 22 percent year-over-year growth, and the CMBS team closed 80 securitizations totaling $57.3 billion. Of those 80, Wells Fargo led or co-led 45, totaling $30.9 billion, making the bank the No. 2 U.S. and global CMBS bookrunner. McShane’s team was also the top Freddie Mac CMBS bookrunner for the third year in a row, the top CRE CLO bookrunner (a title it has held since 2013), and the No. 2 global real estate bonds bookrunner and multifamily single-family rental bookrunner.

Mazer’s team was not short of accolades either. His real estate capital markets team was the top CMBS lender by loan count for the fifth year in a row and lent $10 billion in nonrecourse loans, of which $4 billion were securitized and $6 billion were held on Wells Fargo’s balance sheet. Some of his team’s most notable deals included a $900 million loan on Brookfield Property Partners’ 225 Liberty Street, a $625 million loan on Related Companies and Vornado Realty Trust’s 85 10th Avenue and a $550 million loan for the Shops at Crystals in Las Vegas.—D.B.

12. Paul Vanderslice, Joseph Dyckman and David Bouton

Co-Heads of U.S. CMBS at Citigroup

Last Year’s Rank: 19

Citigroup completed 28 CMBS deals in 2016 comprising a whopping $11 billion in overall volume—a $2 billion increase from its 2015 total. The group purposely targeted all four aspects of the market (conduit, single-asset/single-borrower, agency and collateralized loan obligations) and increased its volume in each bucket.

“We did two to three deals per month, one right after the other, and in some cases we had overlapping deals in the market. It was a planned, well-executed strategy from the beginning of the year. We targeted all four areas and just delivered on it,” Paul Vanderslice said.

Not only was Citi’s overall volume up 15 percent (in a market that was down 25 percent); its market share increased from 8 percent to 12 percent, and the bank ranked No. 4 in overall loan contributions to CMBS.

As if that wasn’t impressive enough, Citi boldly went where no man or woman has gone before and rolled out the first L-shaped risk retention-compliant deal—the $1.3 billion CD 2017-CD3 transaction—in January of this year. “When everyone was doing the practice deals back in December 2016, everyone was thinking ‘vertical, vertical, vertical,’ and we didn’t buy it,” Vanderslice said. “So we did the first L deal, which is far more complicated.”

As for the lure of the “L”? “It made the B-piece, which KKR bought in that deal, non-free to trade,” Vanderslice said. “A vertical deal locks the lenders in for 5 percent all the way down, but the B piece is free to trade, so they can buy it on Monday and sell it on Tuesday. With the L shape, all the relevant parties to the deal are locked in, and I think the L is a superior structure to the vertical structure for that reason.”

Looking ahead to the remainder of this year, “I think the market will be flat to up 15 percent. We want to continue to be more active in 2017 than we were in 2016,” Vanderslice said.—C.C.

13. James Flaum

Global Head of Commercial Real Estate Lending at Morgan Stanley

Last Year’s Rank: 18

For James Flaum’s team at Morgan Stanley, 2016 was characterized by some very large deals for its institutional client base.

Morgan Stanley paired up with AIG in May to provide $1.2 billion for RXR Realty and real estate investor David Werner’s purchase of 1285 Avenue of the Americas, which was one of the largest deals of the year. (And just last month, Flaum’s team topped that by putting together a $1.4 billion financing package to refinance 5 Times Square for the same borrowers.)

The mega-lender also provided two large refinancings for Vornado Realty Trust, including a $700 million loan on 770 Broadway in Manhattan and a $675 mortgage against Merchandise Mart in Chicago.

Jeff Sutton’s Wharton Properties also scored two refis from Morgan Stanley: a $272 million debt package for 529 Broadway in Soho and more recently a $125 million mortgage for the Whole Foods site at 100 West 125th Street in Harlem.

In total, Morgan Stanley’s real estate team completed roughly $14 billion in loans last year, roughly 40 percent of which was securitized, down from $16 billion in 2015.—D.B.

14. Jeff DiModica and Dennis Schuh

President; Chief Originations Officer at Starwood Property Trust

Last Year’s Rank: 17

While Dennis Schuh is new to Starwood Property Trust, he’s no first-timer when it comes to the business.

In May 2016, he left his longtime post at J.P. Morgan Chase to oversee Starwood’s large loan lending business. Jeff DiModica said that the company has seen a tremendous spike in deals, in part due to Schuh’s presence on the team.

“Having Dennis has been transformational,” he said. “There is not a better liked person that I’ve ever worked with, both internally and externally. After 19 years [at J.P. Morgan Chase], his Rolodex is a phonebook.”

In 2016, Starwood completed $6.4 billion in commercial real estate debt deals, up from $5.8 billion in 2015. One of its largest was a $330 million loan for the development of Eliot Spitzer’s residential building at 416-420 Kent Avenue in Williamsburg, and a $195 million financing across a first mortgage and mezzanine loan to refinance an office tower at 1180 Peachtree in Atlanta.

Of Starwood’s total CRE volume, more than half was on its balance-sheet lending book, while the remainder was split between the conduit business, commercial mortgage-backed securities and property investment.

“We are the most diversified of our peers,” DiModica said. “Most people have one cylinder of investment, while we have a multicylinder investment approach. I think the bond market was very happy to have an opportunity to put money in a company that wasn’t subject to any one sector.”

In addition to getting deals done and raising a significant amount of equity, Starwood ended the year with “more than $1.5 billion in liquidity,” which will give the company a “tremendous amount of gunpowder to look at a wider spectrum of deals,” DiModica said. Now, Starwood is deciding where to put that capital, and DiModica anticipates that “2017 will be the biggest production year by far.”—D.B.

15. Roy March

CEO at Eastdil Secured

Last Year’s Rank: 5

Early in the year, Eastdil Secured’s investment sales brokers negotiated one of the biggest acquisitions of 2016—CalPERS and CommonWealth’s $1.9 billion purchase of 787 Seventh Avenue from AXA Financial—and the finance team brokered the respective $1 billion acquisition financing.

Then, Eastdil suffered a big blow last October when top investment sales deal makers Douglas Harmon and Adam Spies left the company for Cushman & Wakefield.

Following the departure of Harmon and Spies, Roy March became a more frequent presence in the New York City office, as Commercial Observer reported in late December.

“He has been in New York every single week since these guys left,” David Lazarus, a senior managing director in New York, told CO at the time. “Given what happened he’s been much more focused on New York.”

Perhaps that focus paid off.

Toward the end of the year, Related Companies and Vornado Realty Trust secured $625 million to refinance 85 10th Avenue, according to Grant Frankel, a managing director at Eastdil, the exclusive adviser in the deal.

Eastdil—a wholly owned subsidiary of Wells Fargo—also brokered Savanna’s $257.5 million purchase of The Falchi Building in Long Island City, Queens, from Jamestown. And, the finance arm arranged Savanna’s $200 million acquisition loan for the property, which has an address of 31-00 47th Avenue, from Blackstone Group, Savanna announced on Dec. 22, 2016.

But still, the company’s originations decreased in the U.S. last year to $41.1 billion, with deals averaging $207 million, from $52.4 billion in 2015, when deals averaged $236 million, Frankel said.—L.E.S.

16. Robert Merck and Gary Otten

Head of Real Estate and Agricultural Finance; Head of Real Estate Debt Strategies at MetLife

Last Year’s Rank: 11

Talk to a lot of the firms on this list about how they did last year, and almost everyone gives you the qualified answer, “Not as good as 2015, but nobody did as well as 2015.”

MetLife is one of the debt originators that doesn’t have to make excuses: It had an unambiguously better year in 2016 than it did in 2015.

The commercial real estate wing of the insurance industry titan originated a record $15 billion in loans, up roughly 5 percent from its previous record in 2015 of $14.3 billion.

Granted, it was not as dramatic a jump as the company made from 2014, where origination increased 18 percent, but it’s hard to keep breaking records.

“[Last year] represented the fourth consecutive year of record commercial mortgage loan production for MetLife’s platform,” Gary Otten said. “I am hopeful that 2017 will continue our team’s trend of high-quality commercial mortgage originations, consistent with prior-year results.”

Among the highlights of 2016, MetLife threw $275 million at the Cherry Creek Shopping Center, a mega-mall in Denver, Colo., as the lead lender in the $550 million mortgage financing with PGIM Real Estate Finance, according to Commercial Real Estate Direct; it provided a $415 million floating-rate warehouse facility secured by a portfolio of 12 commercial mortgages nationwide, and finally, its big kahuna of 2016 was a $563 million first mortgage on a portfolio of Class A industrial properties in California, according to a release from MetLife.

But, of course, those were the biggies. MetLife continued expanding globally, inking deals worldwide, including $533 million in loans in Australia, more than $289 million in Japan and other deals in the U.K., Chile, Mexico and South Korea.—M.G. and D.B.

17. David Durning and Marcia Diaz

President and CEO; Global Head of Originations at PGIM Real Estate Finance

Last Year’s Rank: 26

Last year was a busy one for life companies and PGIM was no exception. The company provided more than $13.9 billion in financing nationwide, $13.2 billion of which was driven by multifamily, industrial and office property transactions.

“I think that 2015 and 2016 were fairly similar,” Marcia Diaz said. “Both were very strong years and very close in originations. In terms of real estate fundamentals and activity they were also similar—we felt like everything was humming. So far, if we annualize our production, we are on track for a similar production year in 2017.”

PGIM has a variety of loan offerings—from mezzanine and preferred equity to agency products from Fannie Mae and Freddie Mac—and began offering financing on “core-plus” assets, or more transitional commercial real estate transactions with a value-add component this year. “Core-plus is a natural extension of our core lending strategy,” Diaz said. “We see demand for this debt product and wanted to be able to provide an option for our borrower clients.”

Standout transactions from 2016 include a $271 million, 10-year fixed-rate portfolio loan for 32 well-leased industrial properties in Mexico (Guadalajara, Monterrey, Mexico City and Tijuana), totaling 7.5 million square feet. “We have invested in Mexico before, but this was a new borrower for us, and we were very excited to do that deal,” Diaz said.—C.C.

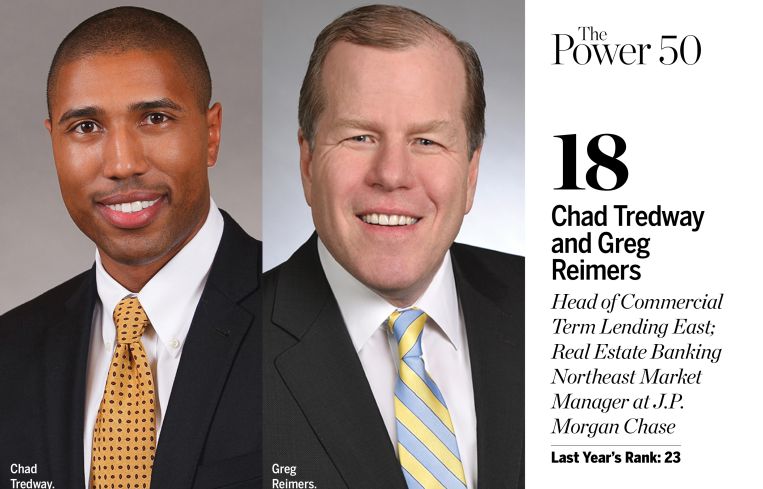

18. Chad Tredway and Greg Reimers

Head of Commercial Term Lending East; Real Estate Banking Northeast Market Manager at J.P. Morgan Chase

Last Year’s Rank: 23

Being a New York-based bank, J.P. Morgan Chase had yet another big year of lending in the Big Apple. The bank lent just over $6 billion in debt across the five boroughs last year, according to data from Actovia, up from $4.2 billion from the year prior.

Chad Tredway attributes J.P. Morgan’s success to its “client obsession” and “certainty of execution.”

“We remained consistent in our ability to lend to clients when regulatory headwinds hit almost all of our competitors,” he said.

His team focused on providing debt on housing across the city, and some of their deals included a $70 million loan on seven Manhattan apartment buildings, a $55.8 million financing for six multifamily properties across Queens and Brooklyn and a $24.5 million mortgage for 445 East 77th Street on the Upper East Side, city records indicate.

“Since 2013 we have been working to be a stable source of capital because we want people to live in New York City and because the supply and demand characteristics are in our favor,” Tredway said. “We focus on rent-regulated housing for two reasons: No. 1, we believe it’s great for the community. We’re a New York-based bank, and therefore we believe it’s our responsibility to lend on housing that’s affordable in New York City. No. 2, we believe that rent-regulated housing provides a very safe place to lend. The cash flow and volatility on it is lower than free-market assets.”

Greg Reimers’ team was also active and participated in some of the city’s most iconic deals of the year. The bank provided part of the $1.5 billion construction loan for SL Green Realty Corp.’s One Vanderbilt, and it also teamed up with M&T Bank and U.S. Bank on the $250 million loan for the development of Rudin Management and Boston Properties’ Dock 72 in the Brooklyn Navy Yard.

Looking forward, rising interest rates could be a game-changer for borrowers, especially depending on how far and how fast they rise, Reimers said.

“Any responsible real estate investor who is looking at a new loan or new acquisition has to look at how much that investment is going to perform in a higher interest-rate environment,” he said. “It affects how much a buyer can pay, and it impacts a lender’s coverage on a loan and their ability to get repaid at maturity.”—D.B.

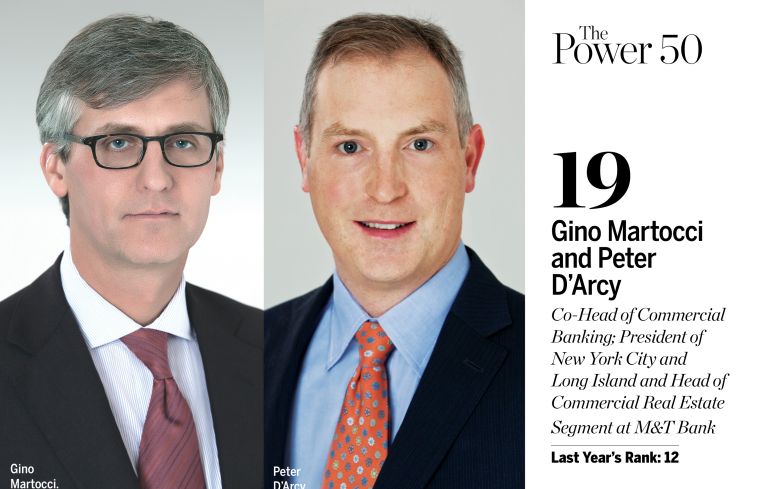

19. Gino Martocci and Peter D’Arcy

Co-Head of Commercial Banking; President of New York City and Long Island and Head of Commercial Real Estate Segment at M&T Bank

Last Year’s Rank: 12

“We pride ourselves on being the bank we’d want if we were one of the successful entrepreneurs we’re dealing with,” Peter D’Arcy said. Given last year’s success, it’s easy to see why.

Gino Martocci runs the company’s commercial banking activities (including the off balance sheet subsidiary M&T Realty Capital Corporation, which did $3.6 billion worth of business in 2016), while D’Arcy leads M&T’s commercial real estate business. In total, M&T financed over $13 billion worth of business in 2016, up from $10 billion the year prior.

Last year, M&T funded two sizable deals on behalf of the Durst Organization: a $92 million loan for the real estate owner’s purchase of 1800 Park Avenue and a $167 million mortgage for a development site at 29-37 41st Avenue in Long Island City, Queens. M&T also originated a $135 million mortgage for Two Trees Management’s 20 Jay Street and $62 million for a purchase in Newport, N.J., by the LeFrak family.

Despite the size of the deals, Martocci views M&T on more intimate terms.

“We talk about ourselves as a community bank,” he said. “Our mission is to serve the communities we’re in and the clients we carefully select to do business with through cycles. We’re not in it when things are good and out when things are bad.”

e and be really good banking partners for them. That’s what gets me personally excited about doing what we do.”—L.G.

20. Steve Kenny and Brad Dubeck

East Region Real Estate Executive; Commercial Real Estate Banking Executive for New York and New Jersey at Bank of America Merrill Lynch

Last Year’s Rank: 6

In 2016, Bank of America continued to grow its business overall, but its New York and New Jersey team saw a dip in originations—to roughly $2 billion from $4.3 billion the year prior.

“There were fewer large-scale construction loans last year, and there was less deal flow in 2016 than 2015 in terms of our clients,” Brad Dubeck said. “We have a very selective client base, and last year a lot of them considered themselves sellers.”

“As a business, we focused on serving our investors on quality real estate projects through the country,” Steve Kenny said, noting that Bank of America’s lending activity was diversified in 2016 with roughly 50 percent of activity in the term loan space, 25 percent in construction and the remaining 25 percent consisting of corporate lines and other types of credit facilities.

One of Bank of America’s largest deals was a $1 billion portfolio loan backed by more than 80 retail properties, Kenny said, declining to provide further details.

While potential changes to the financial markets’ regulatory framework are the topic du jour, Dubeck said deregulation would likely not have much of an impact on the banking system.

“[Banks] have spent so much time adopting new processes and regulations—many of which, I think, are frankly good for operating the business—that I don’t think there would be much change in how banks operate even if deregulation does happen,” he said.—D.B.

21. David Schonbraun

Co-Chief Investment Officer at SL Green Realty Corp.

Last Year’s Rank: 15

New York City’s largest office landlord had an active 2016 on the commercial real estate finance front, having received a $1.5 billion all-bank construction loan to finance the development of its One Vanderbilt office tower in Midtown. That said, SL Green continued to be a major lending player as well with its focus on subordinate and transitional debt.

David Schonbraun, who leads the real estate investment trust’s structured finance operations, pegged the firm’s originations at close to $2.2 billion in commercial debt in 2016—up from $1.8 billion in 2015.

He described SL Green as “the leader in New York”—the only market in which it is active as a lender—on bridge and mezzanine financing. “I think we provide more of this product in New York than anyone,” he said.

Notable deals included teaming up with Apollo Global Management to provide a $160 million mezzanine loan to JDS Development Group and Largo Investments for their American Copper Buildings rental towers at 626 First Avenue and a $200 million junior mezzanine loan to RXR Realty and David Werner to refinance their 5 Times Square office building.

“In this market, we’re trying to [look for] very good sponsors with very good product,” Schonbraun said, noting that SL Green’s lending operations have focused on the multifamily, office and retail sectors while mostly staying away from hotels and for-sale condominiums.—R.M.

22. David Lehman

Global Head of Real Estate Finance at Goldman Sachs

Last Year’s Rank: 16

David Lehman continues to pull the strings when it comes to the investment banking giant’s real estate finance operations, of which he assumed control in 2014. Goldman Sachs remains a major player in both commercial property financing and commercial mortgage-backed securities, backing deals globally while also retaining a high profile in New York.

Goldman acted as bookrunner on 21 CMBS deals totaling $7.79 billion—10.3 percent of the total market share—in 2016, according to Commercial Mortgage Alert. That dollar volume was down 6.4 percent from 2015, when it did 17 deals totaling $8.32 billion, albeit having a lower market share of 8.2 percent.

The bank’s contribution to CMBS deals, however, grew in 2016 to $6.79 billion from $6.26 billion the previous year—an 8.5 percent increase.

Notable recent deals include a $400 million refinancing of Vornado Realty Trust’s 350 Park Avenue office tower and a $450 million CMBS loan for SL Green Realty Corp.’s 485 Lexington Avenue office building. Goldman also teamed up with Wells Fargo to provide a $150 million securitized mortgage for BLDG Management and Crown Acquisitions’ 1 West 34th Street.

Goldman Sachs also underwrote $1.06 billion in bonds issued by the Metropolitan Transportation Authority and backed by the Hudson Yards mega-development on Manhattan’s Far West Side—the first time the MTA issued real estate-backed bonds in its history.—R.M.

23. Jeff Fastov

Senior Managing Director at Square Mile Capital Management

Last Year’s Rank: 30

It’s hip to be Square when your origination volume doubles for the second year in a row. In 2016, Square Mile Capital Management originated a cool $3.3 billion across its three lending strategies—leaving its $1.6 billion 2015 total in the dust.

In what was undoubtedly the year of the nonbank lender, Square Mile had an especially active 2016. “Because we do senior, mezzanine and common equity, we literally invest up and down the capital stack,” said Jeff Fastov, who heads up Square Mile’s commercial real estate lending business. “We’re starting to see a lot more repeat business and feeling the real benefit of being able to offer so many different capital solutions.”

Notable transactions include a $40 million mezzanine loan for the refinancing of the Hyatt Regency in New Orleans, a $45 million mezzanine loan for Minskoff Equities’ 1166 Avenue of the Americas and, most recently, a $145 million construction loan for The Bohannon Companies’ Class A office building in Menlo Park, Calif.

“The banks became even more conservative on development lending [last year],” Fastov said. “The Menlo Park deal is an example of what we hope to do more of. There was a pretty fundamental and pronounced change in the market for construction lending, and that created a big opportunity for us.”

Borrowers that work with Square Mile know that the team will go all out to provide the perfect deal, Fastov said. “We don’t leave the room until we find [a solution for our client].”—C.C.

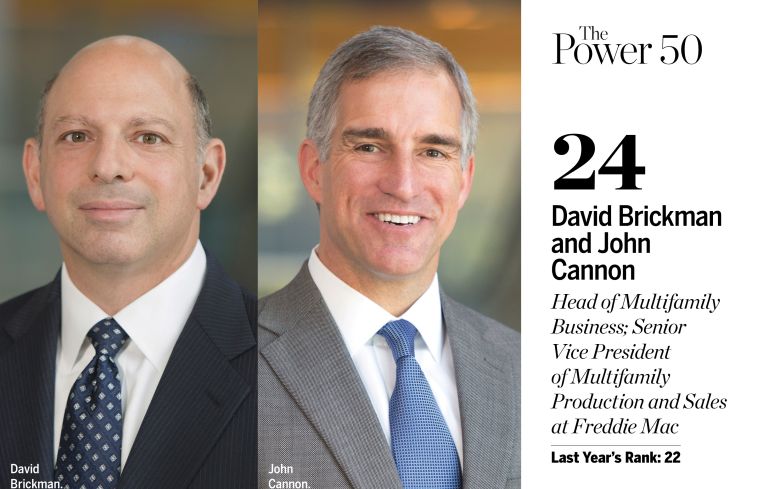

24. David Brickman and John Cannon

Head of Multifamily Business; Senior Vice President of Multifamily Production and Sales at Freddie Mac

Last Year’s Rank: 22

Freddie Mac is the top dog when it comes to multifamily lending in the United States. The government-sponsored entity reported $56.8 billion in loan purchasing volume in 2016, up from $47.3 billion a year prior. But that’s not all: The agency issued a record-high $51 billion in securities last year, making it the largest issuer of structured securities in the commercial mortgage-backed securities market.

And Freddie Mac did all of this without a sizable (a.k.a. over $1 billion) transaction last year. If the lender could categorize 2016, it would call it a year of success in “terms of social impact.” While the largest deal the lender completed in 2016 was a $238 million financing for Fairstead Capital’s $315 million acquisition of the 1,790-unit Savoy Apartments in Harlem in July, it was primarily smaller transactions that drove business.

“We love going after the large deals in Manhattan as well, but we were able to put up the numbers that we put up while not having any mega-deals,” David Brickman said.

Freddie Mac provided about $4.5 billion in loans across the United States through its small balance loan program, which offers loans between $1 million and $6 million to smaller projects. In just the five boroughs alone, it issued 200 such loans for $500 million in debt.

Freddie Mac also financed more than $6.3 billion for the construction or redevelopment of rent-restricted housing for low- and moderate-income families, and it issued $5.2 billion in loans on rental housing where landlords made “green” upgrades. In addition, Freddie Mac financed more than $1 billion through its moderate rehabilitation program, which allowed the renovation of about 50 moderate-income communities across the country, and it provided $3.2 billion in its senior housing business.

“To get to $57 billion last year without a mega-deal was a statement—it was a lot of singles, doubles and triples,” John Cannon said.—Liam La Guerre

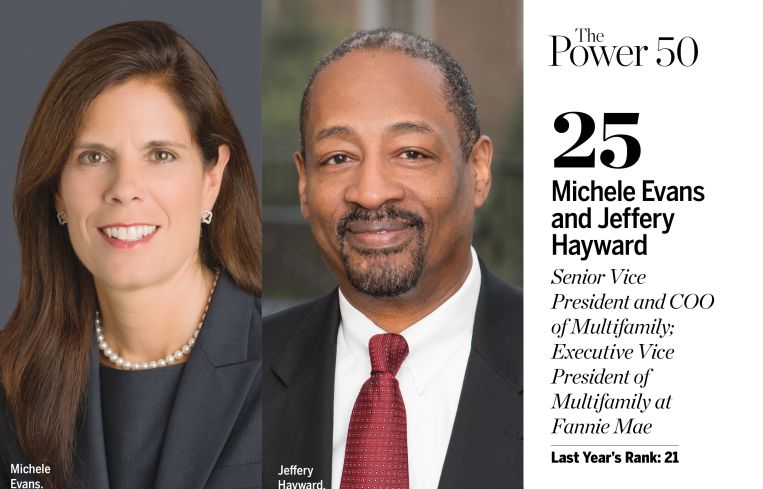

25. Michele Evans and Jeffery Hayward

Senior Vice President and COO of Multifamily; Executive Vice President of Multifamily at Fannie Mae

Last Year’s Rank: 21

Fannie Mae Multifamily, which relies on its roughly 30-year-old Delegated Underwriting and Servicing program to finance rental housing, had its busiest year in 2016. Last year, the arm provided financing for $55.3 billion worth of multifamily loans, according to Jeffery Hayward. “The number has continuously gone up probably since conservatorship,” Michele Evans noted, referring to September 2008, when the Federal Housing Finance Agency gained broad authority over Fannie Mae and Freddie Mac.

Fannie’s biggest deal last year was the closing of a $2.7 billion mortgage to fund Blackstone Group and Ivanhoe Cambridge’s purchase of Stuyvesant Town-Peter Cooper Village on the East Side of Manhattan. (While the sale closed in December 2015, Fannie Mae purchased the debt from Wells Fargo in January 2016.)

Evans and Jeffery Hayward both highlighted the company’s green initiatives, through which Fannie incentivizes borrowers making environmentally friendly improvements by offering lower pricing.

Of its 2016 deals, $3.6 billion were green loans, a number that has increased each year since Fannie introduced green lending products three years ago, Evans said. A lot of that, the pair said, came as a result of the company’s efforts to educate buyers about green financing. “The big jump was really a function of the programs that we established but also the attractive financing and the attractive pricing,” Evans said. “I also think it had a lot to do with buyers learning about the nuances with [going green].”

When it came to manufactured housing community transactions, Fannie came out ahead last year, with $3 billion worth of business, versus the typical $1 billion a year, Evans noted. The spike was in large part due to a $1 billion financing to YES! Communities last August, which was backed by 120 communities that will provide workforce housing for more than 29,000 families in 13 states. That was the biggest MHC deal Fannie has ever done, Hayward noted.—L.E.S.

26. Aaron Appel, Keith Kurland, Jonathan Schwartz and Dustin Stolly

Managing Directors at JLL Capital Markets

Last Year’s Rank: 25

Between Aaron Appel, Keith Kurland, Jonathan Schwartz and Dustin Stolly, JLL's real estate investment banking team negotiated $12.6 billion in debt deals last year, up from $9.4 billion the year prior—numbers that stand out in a year where many lenders experienced less deal flow volume.

Kurland secured a $370 million financing from Deutsche Bank and SL Green Realty Corp. on behalf of Kushner Companies, for the old New York Times Building at 229 West 43rd Street. Appel and Schwartz negotiated a $102 million Mesa West loan for Taconic Investment Partners, TH Real Estate and Squire Investments' 817 Broadway. And despite being based in New York City, the broker powerhouse was active across the country. Stolly arranged a $300 million construction loan from Cornerstone Real Estate Advisers for Steve Witkoff's Edition-branded hotel in West Hollywood, Calif.

When it comes to 2017, Stolly said there are positive signs in both the long-term fixed-rate and transitional debt markets. "[They're stronger and more competitive than I’ve seen in several years," he said. "There's significant stability, which is a good sign, particularly in the CMBS market—and there's a ton of competition. If you’re a borrower, you’re going to have tremendous opportunity to take advantage of that. There’s an abundance of capital for all asset classes and all types."—D.B.

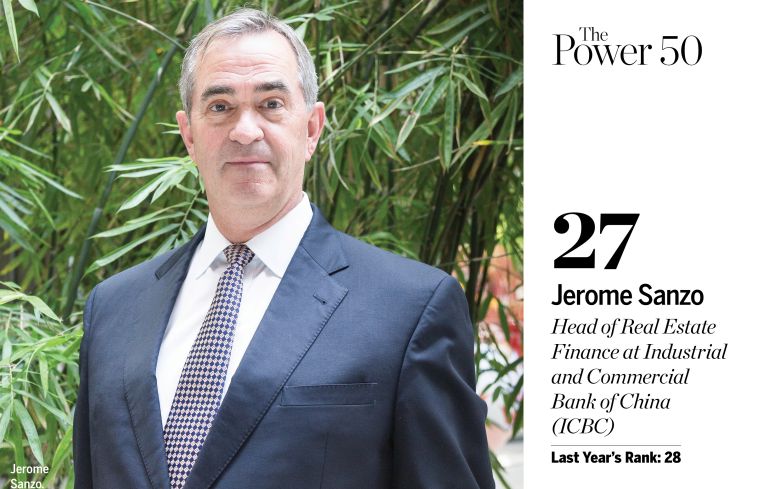

27. Jerome Sanzo

Head of Real Estate Finance at Industrial and Commercial Bank of China (ICBC)

Last Year’s Rank: 28

When Commercial Observer sat down with Jerome Sanzo last summer, he had just learned how to say, “xin qing hao,” which means “the mood is very good.” That sentiment carried on throughout the year, as ICBC originated another $2.5 billion in 2016, roughly the same as the year prior.

The Chinese bank focused its energies on gateway markets, like New York City and Los Angeles. In January 2016, ICBC provided a $211.6 million loan to Kuafu Properties and Shanghai Construction Group for the acquisition of the top 13 floors of 1 MiMa Tower. In September, it teamed up with Deutsche Bank and Natixis Real Estate Capital on a $500 million senior loan for Extell Development Company’s One Manhattan Square. The following month, ICBC led a $115 million mortgage for Brookfield Property Partners’ Silver Spring Metro Plaza office complex in Silver Spring, Md.

Looking forward, Sanzo thinks the “story this year will be how much foreign investment in U.S. real estate will continue, grow and taper,” he said. “It’s no surprise and no secret that the Chinese government is trying to curtail some [of the outbound investment]. It’s more difficult to move money out.”—D.B.

28. Robert Verrone and Christopher Herron

Principal; Managing Director at Iron Hound Management Company

Last Year’s Rank: 29

Wachovia alumni Robert Verrone and Christopher Herron continued to move and shake on multiple fronts through their restructuring advisory platform and debt and equity business.

In total, Iron Hound was involved in roughly $3.8 billion in debt transactions in 2016, Herron said—up from roughly $3 billion in 2015. He attributed the increase to “an overall ramping up of our platform,” with the firm continuing to tap into relationships with existing clients and making inroads with new ones.

Notable deals included advising on the $272 million refinancing of retail magnate Jeff Sutton’s new development at 529 Broadway in Soho, a $217 million workout of Chetrit Group, Edward J. Minskoff Equities and the Moinian Group’s 500-512 Seventh Avenue office building in Midtown and a $194 million financing package for Chetrit’s condominium conversion of 49 Chambers Street in the Financial District.

But Iron Hound still maintains a national presence: Herron noted the firm remains “bullish on the major markets in gateway cities, across all asset classes.” He said he expects the firm’s restructuring advisory business to “stay very busy” in the face of upcoming maturations involving legacy commercial mortgage-backed securities originations from 2006 to 2008 “still left to come on the table.”—R.M.

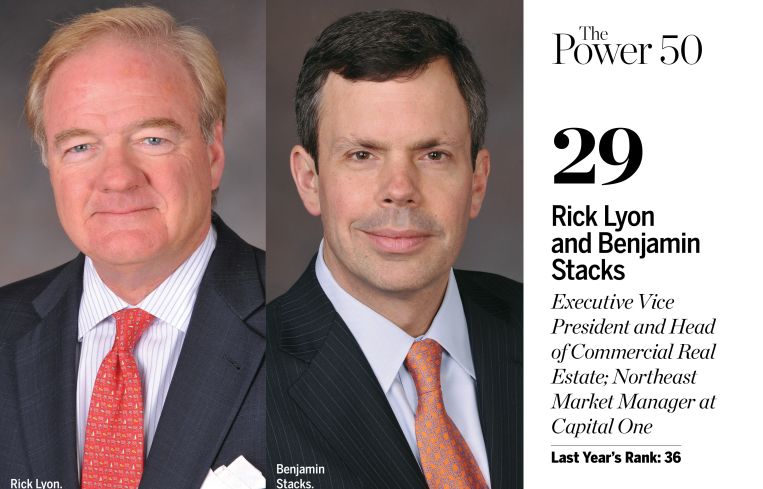

29. Rick Lyon and Benjamin Stacks

Executive Vice President and Head of Commercial Real Estate; Northeast Market Manager at Capital One

Last Year’s Rank: 36

Capital One’s portfolio of loans grew to $26.5 billion in 2016, up by nearly $1 billion the year prior.

Similar to growing its book, the bank’s current strategy revolves around growing its presence, Benjamin Stacks said. In addition to its operations in New York, New Jersey, Pennsylvania, Louisiana and Texas, Capital One opened offices in Boston and San Francisco recently—and Los Angeles is next on the list.

While Capital One’s focus on growth was national, it was an active lender in the outer boroughs last year with signature deals in Brooklyn, Queens and the Bronx. In April 2016, Capital One provided a $110 million floating-rate, interest-only loan to Taconic Investment Partners and Clarion Partners to refinance their 1,416-unit, 118-building Eastchester Heights Apartments in the Bronx.

Then in December, Capital One issued an $80 million construction loan to Starwood Capital Group and Toll Brothers for the 194-key 1 Hotel Brooklyn Bridge in Dumbo. The project, which opened this February, includes 20,000 square feet of meeting space, a 24-hour-fitness center, a spa, and a rooftop bar and a pool.

“We are cautiously optimistic about current market conditions and remain committed to providing our customers with access to capital, excellent service and competitive rates,” Stacks said.—L.L.G.

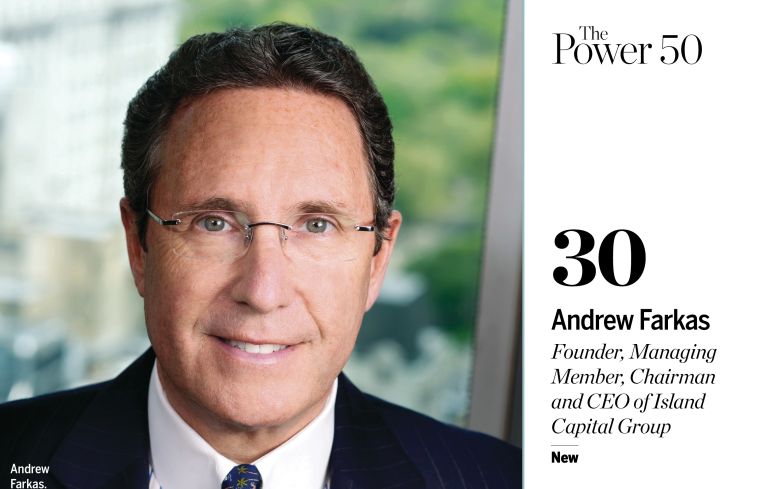

30. Andrew Farkas

Founder, Managing Member, Chairman and CEO of Island Capital Group

New

The king of a veritable real estate empire wasn’t on the Power 50 list last year? What the Farkas! Andrew Farkas, that is. After switching him over to the Power 100 last year, we thought it’d make more sense for the founder and chief executive officer of Island Capital Group (and its subsidiaries C-III Capital Partners, NAI Global and EVO) to have a spot on this list.

C-III Capital Partners is one of the largest CMBS investors and special servicers in the U.S. Its special servicing arm oversees $60 billion in commercial loans—likely boosted last year by the wave of CMBS maturity defaults and loan modification requests, and its primary servicer handles a further $4 billion. C-III and its subsidiaries manage more than $12.3 billion in assets. In 2016, C-III also acquired Resource America, an asset management company specializing in real estate and credit investments. Resource America manages a publicly traded commercial mortgage real estate investment trust, Resource Capital Corp., as well as four nontraded public REITs and two other investment companies.

“This is a transformative acquisition for C-III,” Farkas said in a September 2016 press release. “With our expanded platform, we are now able to provide commercial real estate debt and equity solutions to both institutions and retail investors. Today, we are well positioned for further growth and to better serve the needs of our clients as well as those of the evolving commercial real estate industry.”

Lastly, the C-III platform is now one of the top 30 multifamily property managers in the nation, with over 43,000 units owned or managed. Within New York City alone, C-III invests in a portfolio of more than 2,000 multifamily units in 15 buildings.—C.C.

31. Dan Thomas and Richard Smith

Vice Chairman and Chief Lending Officer and President of Real Estate Specialties Group; Executive Vice President and Northeast Manager of Real Estate Specialties Group at Bank of the Ozarks

New

The Little Rock, Ark.-based bank has made huge strides in recent years, transforming itself from a regional player into one of the more active lenders in the New York City commercial real estate market.

Bank of the Ozarks’ real estate specialties group, led by Dan Thomas, originated $8.24 billion in debt in 2016—up considerably from $5.63 billion the previous year. Thomas said the increase was due to “both a larger number of loans and a larger average loan size.”

While an increasing number of lenders have deemed the residential condominium sector too risky to engage with, Bank of the Ozarks has stepped in to fill the void. Some of the bank’s most notable deals include a $108 million loan for XIN Development’s new 72-unit condo building at 615 10th Avenue in Hell’s Kitchen; a reported $135 million in financing for JDS Development Group and the Chetrit Group’s supertall residential development at 9 DeKalb Avenue in Downtown Brooklyn; and a reported $187 million loan for Nathan Berman’s latest office-to-residential conversion at 20 Broad Street.

While Thomas acknowledged that the bank has been active in financing condo projects, he noted that Bank of the Ozarks has “primarily focused on the moderately priced segment of the market” while only lending to “a limited number of ‘luxury’ condo developments.”

“We have been very selective with respect to the location, strength and experience of sponsorship, current and anticipated future supply in the submarket and presales contracts,” Thomas said. “In all cases, we have kept our leverage ratio low.”—R.M.

32. Mark Talgo

Senior Managing Director and Head of New York Life Real Estate Investors

Last Year’s Rank: 35

In 2015, New York Life Real Estate Investors had a record year with $10 billion in new deals across its lending, equity and real estate securities businesses. And in 2016, the life company fell just shy of that number with $9 billion in its three divisions. But Mark Talgo touted that the company grew to $50 billion in total assets under management, up from more than $46 billion in 2015.

One of the lending platform’s major highlights from last year came in June, when it provided $228.1 million in financing to ECI Group for a 10-property multifamily portfolio across Georgia and Florida.

Later in 2016, New York Life Real Estate Investors originated $225 million in debt on behalf of Macerich and Institutional Mall Investors for The Village at Corte Madera, a 460,000-square-foot regional mall in Corte Madera, Calif. And in November, it issued a $90 million, 15-year loan to TF Cornerstone for two Washington, D.C., office buildings at 1156 15th Street NW and 1620 Eye Street NW.

Talgo is projecting New York Life’s business will remain consistent in 2017. “We expect to [invest] $9 billion and maybe closer to $10 billion,” he said. “It’s still competitive out there. There is no other way to look at it. Even though there are some areas that look stressed, [real estate] fundamentals are in still good shape.”—L.L.G.

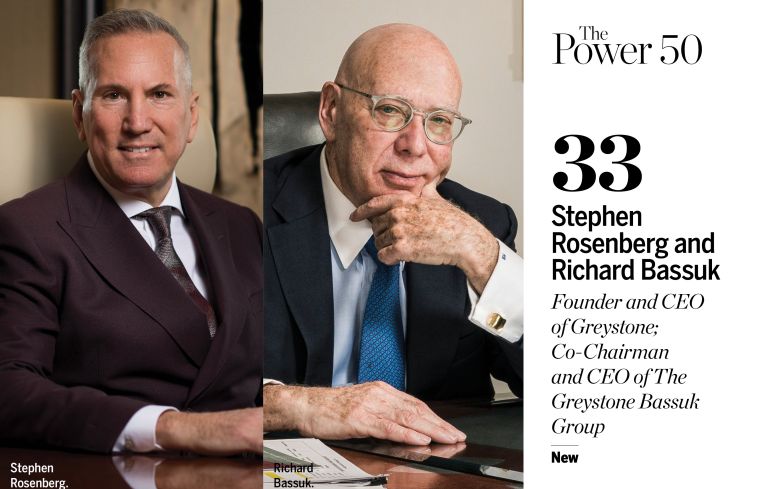

33. Stephen Rosenberg and Richard Bassuk

Founder and CEO of Greystone; Co-Chairman and CEO of The Greystone Bassuk Group

New

Stephen Rosenberg’s Greystone racked up $7.1 billion in agency, commercial mortgage-backed securities, bridge and proprietary loan originations in 2016, a 34 percent increase over its $5.3 billion 2015 number. A top Fannie Mae and Freddie Mac lender, the company was the most active Fannie Mae small loan originator in 2016 and the No. 2 Freddie Mac lender for small balance loans. As if that wasn’t impressive enough, the firm also grew its loan servicing portfolio to a whopping $21 billion.

With a national reach, some of the notable deals keeping Rosenberg’s team busy included a $106 million Fannie Mae financing for the acquisition of a six-property portfolio in Texas, a $103 million affordable housing preservation recapitalization in Florida and a $221 million Freddie Mac credit facility for an 1,800-unit affordable housing property in California.

Greystone’s advisory business, The Greystone Bassuk Group, has been busy too. Last February it completed the $586 million refinancing of a portfolio of 34 multifamily properties located in New York, Florida, Nebraska, Nevada, Arizona and Colorado on behalf of Maxx Properties.

The firm has also been busy building out its EB-5 practice. “It was something that took patience,” Richard Bassuk said. “As we were doing it, we thought, ‘It’s going slowly,’ but then it started accelerating. At the end of the day when we look back, it will be something that sits well with our overall corporate strategy, and I feel very proud of it.”

As with anything else, “Nothing worth doing is ever easy, and that’s what my wife always tells me,” Bassuk said. “Greystone has had the success it has had by being very careful and by being very client-centric. It’s another form of consumerism, and if you don’t do a good job, you’re going to have that hit you over the back of the head.”—C.C.

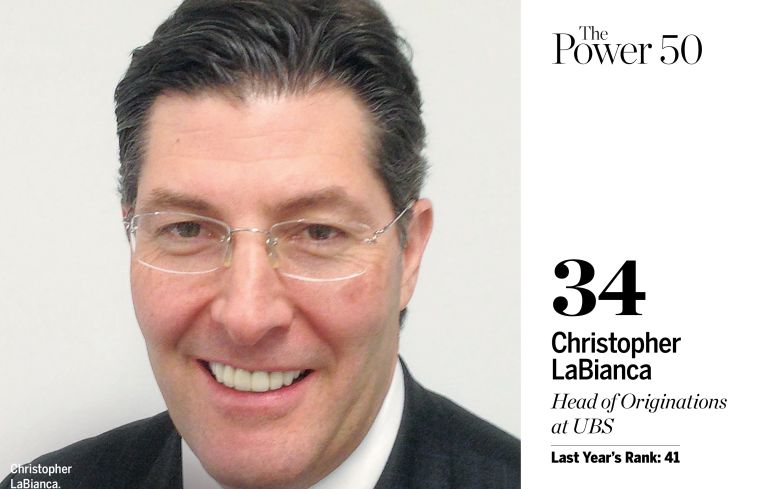

34. Christopher LaBianca

Head of Originations at UBS

Last Year’s Rank: 41

UBS’ lending business remained steady year-over-year, holding to $3 billion in volume in 2016. Of that, roughly $2.5 billion was securitized in the commercial mortgage-backed securities market.

Christopher LaBianca said he expects volume to increase in 2017, as the firm rolls out new balance-sheet lending programs.

“Last year was interesting for us because, especially on the CMBS side, the first quarter was so brutal,” he said. “Two-thirds of the entire production for the year got done in the second half.”

And indeed, some of UBS’ most iconic deals closed in the latter half of 2016. In August, the firm co-originated a $272 million debt package with Morgan Stanley for Jeff Sutton’s 529 Broadway Nike store in Soho, and in November, UBS teamed up with Citibank on a $215 million refinancing of Metropole Realty Advisors’ 681 Fifth Avenue.

As for 2017, LaBianca said the market should be busy for the first two quarters, as loans from 2007 are coming due. “It’ll be interesting to see what the second half of the year looks like because we expect less rollovers and expect interest rates to start moving up,” he noted.

Interest rates aren’t the only relevant factor for UBS’ business, though. The firm is watching spreads, which have been at “extremely tight levels” throughout the capital stack, LaBianca explained. “It’s hard to believe that they could stay there for the entire year,” he said. “You would expect that they probably start to widen out as product becomes a little more scarce as there is less opportunity for refinancings [in the latter half of 2017].”—D.B.

35. Michael Lehrman and Anthony Orso

Co-CEOs and Co-Founders of CCRE

Last Year’s Rank: 14

CCRE saw a down year on the CMBS side, according to figures from the Commercial Mortgage Alert, which reported that after contributing $4.1 billion to CMBS deals in 2015, that figure dropped 23 percent for the firm in 2016 to $3.15 billion, or 4.7 percent of the market share. From that figure, $96 million was in single-asset, single-borrower deals.

One 2016 deal for the company, according to Commercial Property Executive, was the sale of a $112 million fully performing, adjustable-rate loan portfolio of commercial and multifamily assets in four states, to “a mix of private equity groups and regional banks.”

The company did not respond to requests for an interview for this piece.—L.G.

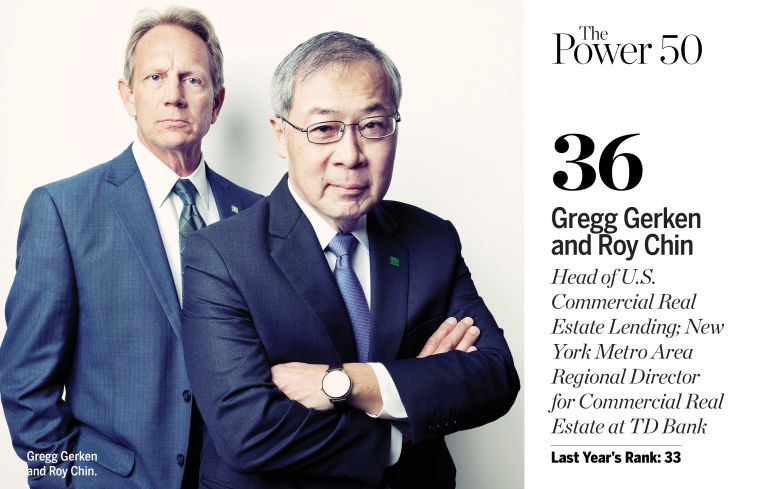

36. Gregg Gerken and Roy Chin

Head of U.S. Commercial Real Estate Lending; New York Metro Area Regional Director for Commercial Real Estate at TD Bank

Last Year’s Rank: 33

TD Bank slightly increased its loan production volume in 2016 to $5.8 billion from $5.3 billion in 2015, and similar to the previous years, its deal flow was driven by its institutional clients doing big deals across New York City.

Perhaps the most notable deal TD was involved in was the $1.5 billion financing of SL Green Realty Corp.’s One Vanderbilt across from Grand Central Terminal. The Toronto-based lender was one of five banks involved in the mega-construction loan and held a $170 million piece of the deal on its books. Additionally, TD preleased 200,000 square feet in the 58-story tower.

TD also provided the Related Companies with $116 million in debt, $58 million of which was used for the development of a 160-unit, mixed-income apartment building in the Hudson Square neighborhood of Manhattan.

As far as 2017 goes, Gregg Gerken predicts that lending activity could cool down. “As the economy continues to improve, future [interest rate increases] have become more likely,” he said, and “one would expect potential rent inflation and an increase in cap rates.”—D.B.

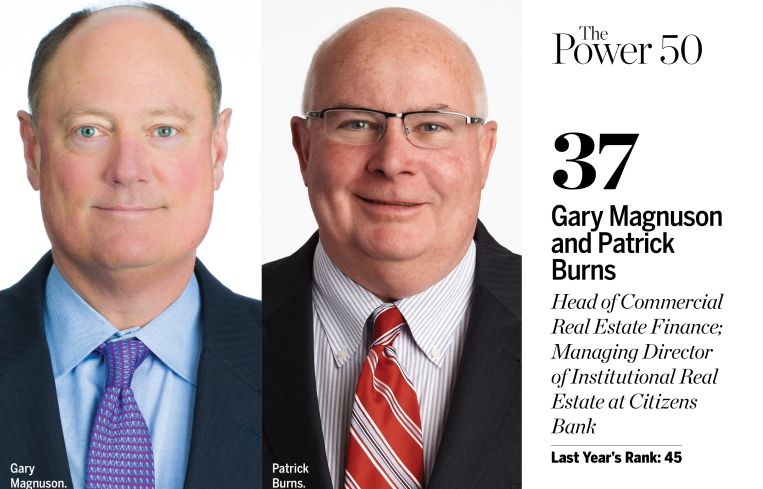

37. Gary Magnuson and Patrick Burns

Head of Commercial Real Estate Finance; Managing Director of Institutional Real Estate at Citizens Bank

Last Year’s Rank: 45

Citizens Bank saw its portfolio grow by 15 percent last year with its outstanding real estate debt reaching $9.8 billion at the end of 2016, compared with $8.5 billion at the end of 2015. “We were able to grow our business in many different ways,” Gary Magnuson said. “We were able to syndicate more deals and lead more deals.”

The bank enacted a strategy a few years ago that focused on proving its capabilities to better sponsors in better markets. “I think we’ve done that,” he said. “The thing that our clients want is certainty of execution, and we’ve been able to provide them with that. As a result we’ve done a fair amount of repeat business with some of the biggest and best real estate sponsors in the country.”

While Citizens’ primary markets are Boston, New York City, Washington, D.C. and Chicago, the Rhode Island-based bank has also been busy providing construction loans in gateway cities across the country. It provided a $107.3 million construction loan to developer Questar Properties for 414 Light Street in Baltimore—a 44-story, 394-unit luxury apartment tower—and a $87.4 million construction loan to Mill Creek Residential for the construction of a 21-story residential tower in Atlanta. Other notable transactions included a $117.3 million loan to a joint venture between DivcoWest and the Rockpoint Group for the acquisition of a 17-story office tower in the heart of downtown San Jose, Calif.

“Last year was a little diverse,” Patrick Burns said. “We were busy with multifamily construction lending in the first half of the year, but as we got into the second half of the year, we saw more opportunities on the office side and in repositioning of properties that institutional buyers were looking to add value to. We also saw a ramp up in the life science space—it’s been a great segment for us.”—C.C.

38. Simon Ziff, Patrick Hanlon and Russell Schildkraut

President; Principal; Principal of Ackman-Ziff

Last Year’s Rank: 37

Ackman-Ziff held steady in 2016, matching its $5 billion in transactions from the year before. While deal volume remained flat, the firm’s revenue has significantly increased due to investment sales and equity activity, Simon Ziff said.

“We think we’re unique in that we are entrepreneurial and aggressive like some of the smaller New York-based firms but still check the boxes for the larger, national institutional clients that represent more than 60 percent of our firm’s business today,” Ziff said.

In a year when construction loans were the quintessential needle in a haystack, Ackman-Ziff managed to secure a $228 million development loan from PNC for RXR Realty’s restoration of Pier 57.

The firm is in growth mode, and its partners made a key decision to expand Ackman-Ziff to 50 professionals last year with new outposts across the country. The advisory firm also built out joint venture equity and investment sales practices. “We achieved our objectives in being both a powerful New York-centric and national capital advisory group,” Ziff said.

With last year’s objectives achieved, 2017 is already off to a roaring start. The firm already has $1 billion in transactions under its belt for the first two months of 2017.

“What’s driving growth is our focus on getting better and the team we have here,” Ziff said. “We have great people whose individual and collective businesses are ramping up nationally. It’s really always about the people.”—C.C.

39. Larry Kravetz

Head of CMBS Finance at Barclays Capital

Last Year’s Rank: 27

While Barclays’ overall lending volume decreased to $3.5 billion from $7.1 billion due to market conditions, the bank remained busy on the bookrunning front. In addition to nine conduit securitizations, Barclays led or co-led seven standalone securitizations in 2016.

“Our objective is to be one of the more meaningful players in the commercial mortgage-backed securities space for both large loan standalone deals and [our] bread-and-butter conduit business,” Larry Kravetz said.

On the conduit side, Barclays led a $100 million financing of the Hyatt Regency in Jersey City, N.J., a $95 million loan for 215 Park Avenue South, and a $130 million fixed-rate loan for a portion of 1166 Avenue of the Americas in Manhattan.

Of that last deal, for a building with three separate condo components, Barclays provided the borrower, Edward J. Minskoff Equities, with the loan it was looking for, then “securitized it into A-note, B-note and mezzanine debt,” Kravetz said.

“When you have a building that has multiple office condominium components, it gets pretty complicated,” Kravetz said. “It’s a good example of our ability to work through those complications.”

As for noteworthy standalone deals, Kravetz referred to the company’s $700 million refinancing of the 1.3-million-square-foot Easton Town Center in Columbus, Ohio, which he referred to as one of the top-performing retail centers in the country.

And while 2016 was a tough year for CMBS lenders—the year started slow and ended with the implementation of the long-awaited risk retention regulation—Kravetz sees better times ahead not only for Barclays but also for the industry as a whole.

“[People ask], How does this look compared to 2007 and that era?” Kravetz said. “The significant difference is that the industry has maintained really strong discipline. So while there’s good liquidity for real estate borrowers, it remains disciplined. I don’t see anything close to a real estate bubble or going off the cliff from the lending side, which has kept things from getting out of hand on the buy side as well.”—L.G.

40. Jeff Friedman and Mark Zytko

Co-Founders and Principals of Mesa West Capital

New

Last year, Mesa West reaped the benefits of having expanded its physical footprint. The Los Angeles-based private lender saw its originations increase to $2.8 billion in 2016, up from $2.1 billion the year prior.

That ramp up in deals is in part due to the Mesa West’s recently opened Chicago office, Jeff Friedman said. Roughly 80 percent of the firm’s overall business was split along the coasts, between its locations in Los Angeles and New York City, while the remaining activity came from Chicago, Denver and Texas.

“2016 was a good year across all of our product [offerings],” Mark Zytko said. “It’s just a continuation of growth, and we were able to react quickly and provide long-term loans that have custom elements.”

What differentiates the debt fund from a large bank, insurance company or CMBS shop, said Friedman, is that with those lenders, borrowers are “forced to accept the structure that is provided by a large institution,” where Mesa West provides customers with more flexibility. “It’s more about trying to make our loan fit the transaction than having the transaction fit our loan,” he said.

Friedman pointed to a $280 million acquisition loan the firm provided to Brightstone Capital Partners and Artisan Realty Advisor’s purchase of the Lantana Media Campus in Santa Monica, Calif. The borrowers were buying the property in an off-the-market transaction, so the financing needed to be closed quickly. Growth is coming from more than just debt deals though: This January, the company closed its fourth fund with a total of $900 million in capital, and in its core-lending fund, Mesa West increased its commitments to $1.2 billion.

“We’re excited about market opportunity,” Friedman said. “We’ve been fortunate to attract the capital we’ve been able to attract and also build our relationships with borrowers and intermediaries. We’re excited to continue to grow out platform going forward.”—D.B.

41. Steven Kohn, Gideon Gil, Alex Hernandez and Dave Karson

President of Equity, Debt & Structured Finance; Senior Managing Director; Senior Managing Director; Executive Managing Director at Cushman & Wakefield

Last Year’s Rank: 42

It’s a Game of Kohns at C&W’s 1290 Avenue of the Americas office, where Steven Kohn and his team of 80 are busy arranging deals on the properties that surround them, including the $850 million financing of 1301 Avenue of the Americas—right across the street.

“1301 [Avenue of the Americas] was our largest loan in 2016, and we closed that with three life insurance companies [MetLife, AXA Financial and New York Life Insurance Company]. Its size and the complexity of having three lenders involved made it the most interesting transaction for me,” Kohn said.

While the overall origination volume dipped slightly to $7.9 billion in 2016 from $8.5 billion in 2015, the team executed some of New York City’s most buzzed-about transactions. Another jewel in C&W’s crown was the combined $315 million refinancing of 10 Times Square and 1410 Broadway on behalf of L.H. Charney Associates.

“I think 2016 was pretty comparable to 2015. The first quarter of the year was a little challenging on the capital markets side, so that got the year off to a slow start, but then we had a great finish,” Kohn said, adding that the deluge of 10-year debt rolling and subsequent need for refinancing bumped up the debt side of the business.

While Kohn, Alex Hernandez, Gideon Gil and Dave Karson lead the charge, Managing Directors John Alascio, Mark Ehlinger and Chris Moyer play critical roles in the team’s successes.

“We’re also working closely with the investment sales team that came over [Douglas Harmon and Adam Spies, who joined C&W from Eastdil Secured in October], and that’s been terrific. The combined capital markets team here has really grown,” Kohn said.—C.C.

42. Greg Murphy

Head of Real Estate Finance Americas at Natixis Real Estate Capital

Last Year's Rank: 31

With $3.2 billion in loan origination in 2016—flat year-over-year—Greg Murphy and his team at Natixis pride themselves on handling complex loan transactions in a manner unlike other firms.

“We have a broad, integrated platform that's fairly unique," Murphy said. “We have a fixed rate that we do for commercial mortgage-backed securities and floating rate that we do for balance sheet on the same platform offered by the same banking teams to the same clients. We're able to offer solutions and certainty in a way our competitors can't."

Of the bank's more prominent deals last year was a $229 million, five-year, fixed-rate loan for RFR Holding and Tristar Capital's purchase of Urban Union, a 12-story, 296,000-square-foot Class A office building in Seattle that will house offices for Amazon.

“We were able to break that financing down into three pieces," Murphy said. “We kept the senior [debt], which we're going to securitize, and then we sold two subordinated tranches in order to optimize that transaction and make it more efficient for the borrower."

Natixis completed a similar $233 million deal, also to Tristar, for the purchase of a three-building office complex in Sunnyvale, Calif., that will be used exclusively by Apple. The bank also provided $208 million to Hana Asset Management for its purchase of a 761,824-square-foot headquarters facility for pharmaceutical firm Novo Nordisk in Princeton, N.J.

Murphy acknowledges the industry's recent bumps, but with business brisk, he said that for lenders that are “making sure [they're] cautious and doing [their] homework…there are reasons to feel optimistic" about the year to come.—L.G.

43. Matt Galligan

President of CIT Real Estate Finance

Last Year’s Rank: 34

CIT originated $2.25 billion worth of loans in 2016, primarily for the “repositioning of office buildings as well as Class B multifamily transactions,” according to Matt Galligan. The bank was busy financing workforce housing in Southern California.

“This is inexpensive housing relatively close to where people work,” Galligan said. “Our clients are buying 30- to 40-year-old garden apartments and putting $7,500 [in upgrades] per unit. They improve them, then they rent them at reasonable rates. We’re doing a lot of work in that market.”